Argentina is on the brink

By: Colby Smith

When Mauricio Macri was elected Argentina's president in 2015, he was hailed as a pro-market, pro-reform leader willing to make the difficult policy decisions that would eventually re-right the country's struggling, inflation-wracked economy.

One extended currency crisis and the largest IMF programme in history later, and his administration's approach to muddling through market volatility while keeping constituents happy is failing ahead of the all-important presidential election in October.

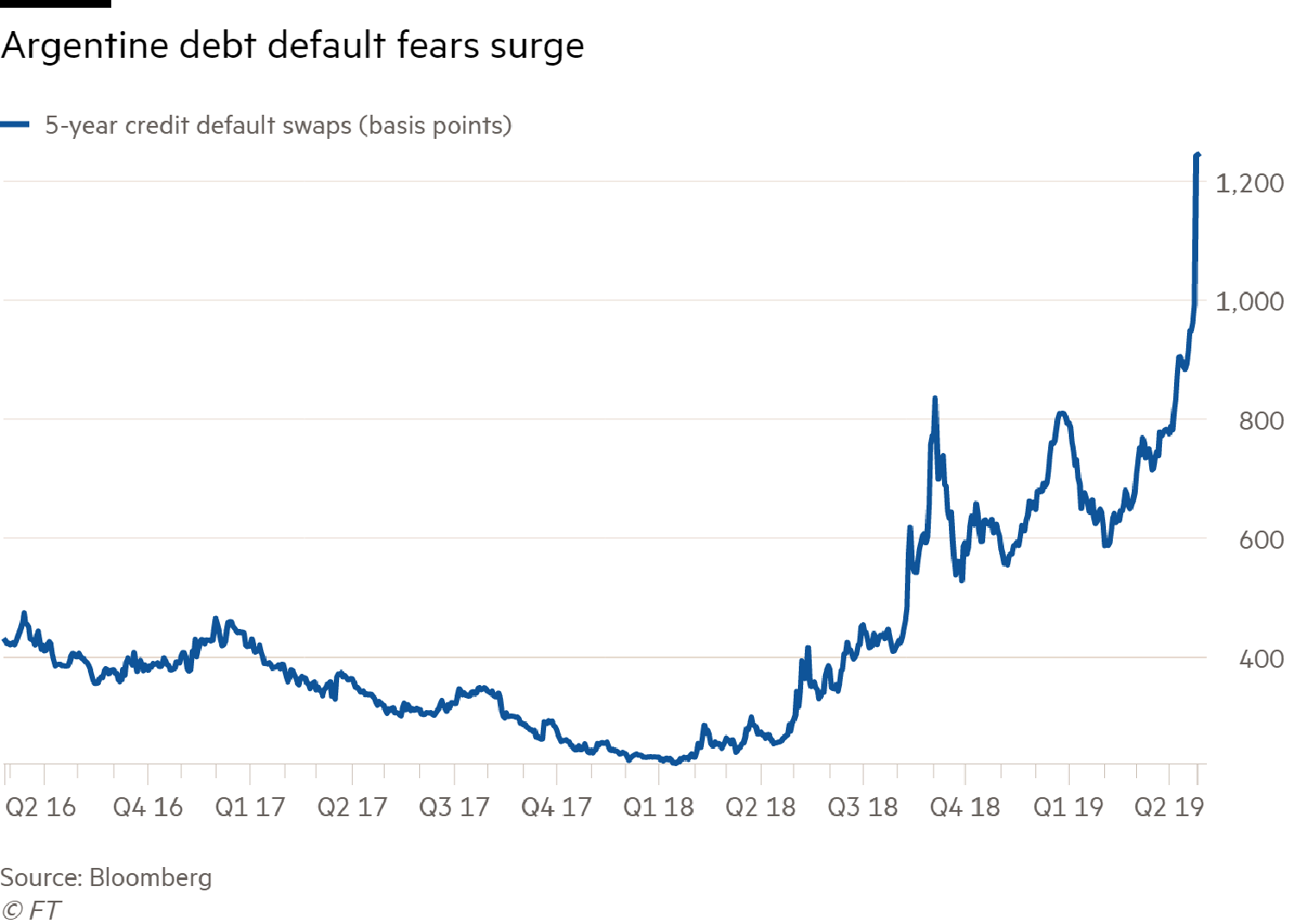

On Wednesday, the cost of insuring against an Argentine debt default surged to its highest level since Macri took office three-and-half years ago, cementing the country's title as the world's second-riskiest sovereign borrower behind Venezuela:

Argentine bond spreads over Treasuries soared nearly 90 basis points, and the yield on a bond due in just two years rocketed to roughly 18 per cent. The much-derided century bond fell to a record low, and the peso tumbled almost 4 per cent against the dollar.

The sharp moves come as Macri's re-election prospects look decidedly dimmer, and government officials scramble to contain both record-breaking inflation and an increasingly volatile currency with little success.

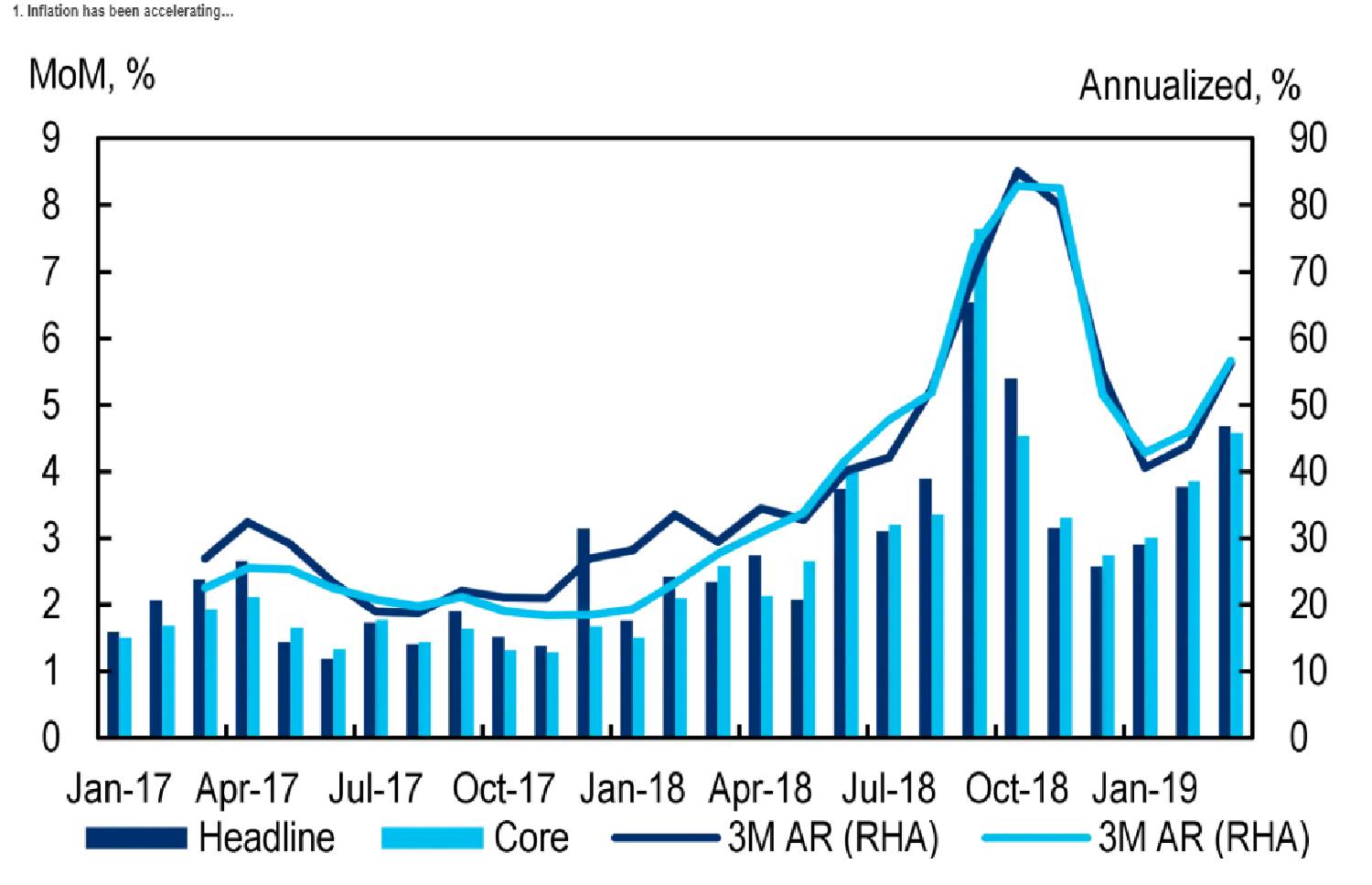

Once again, the most recent reading of inflation surprised to the upside. In March, consumer prices rose 4.7 per cent month-over-month. On an annualised basis, headline inflation now sits near 55 per cent, as this chart from Citi's Fernando Jorge Diaz shows:

To redress this, Macri's administration has leaned on unorthodox economic policies in a “desperate” attempt, as one investor puts it, to clamp down on the runaway inflation that has undermined the country's recovery ever since last year's currency crisis. The most recent comes in the form of price controls. While this may help to anchor inflation expectations in the short-run, it sends a worrying signal to investors with painful memories of the former administration's penchant for economic unconventionality.

Here's what Ashmore Group's Jan Dehn has to say about Macri's recent decision to freeze prices for up to 60 products:

Consistent with its longstanding tradition of mismanaging its economy, the Argentine government last week abandoned its most recent attempt at macroeconomic orthodoxy in favour of the kind of heterodox policy measures, which have been to blame for Argentina’s long record of dismal economic performance.

The problem with such “myopic” economic policies, according to Dehn, is that they may alleviate Macri's increasingly dire political problems in the immediate term, but do very little to redress inflation — one of the underlying sources of his unpopularity among voters.

Government officials have also struggled to keep the currency on an even keel. About a week ago, the central bank unveiled changes to its currency band, which is a range for the peso's dollar exchange rate between which it will not intervene. While the previous band incorporated a 1.75 per cent depreciation in the peso by year-end, the central bank plans to leave the band unchanged at 39.8-51.4 pesos per dollar until 2020. After yesterday's slide, one dollar fetches 43.9 pesos.

Again, this new plan may help to contain an inflationary spiral in the coming months but, according to Ed Glossop at Capital Economics, it may handicap the country later on:

The new measures raise the risk that the peso does not fall far enough to offset the erosion of competitiveness resulting from high domestic inflation and wage growth. The previous band was designed such that the real exchange rate would hold steady or weaken modestly by year-end.

In order for the peso to remain competitive, Glossop reckons the nominal exchange rate will need to weaken to the upper-bound of the currency band. If it instead strengthens to the lower-part of the band, it may become overvalued versus the dollar, necessitating a sizeable, and potentially destabilising, adjustment at a later date.

Not all of the government's policies have failed. With an ultra-tight monetary stance, the central bank has effectively engineered a massive rebalancing of the country's trade balance — a key issue for investors not too long ago. In March, Argentina recorded an impressive $1.18bn trade surplus, driven by a 33.7 per cent year-over-year decline in imports. Just last year, the country was sporting a gaping $554m trade deficit.

The problem is that a trade surplus doesn't win elections, a point made by pollster Alejandro Catterberg of Poliarquia Consultores at an event hosted by JPMorgan in Washington DC this month:

The problem is that many of those fundamentals are basically Chinese for the regular people on the street. They don't understand what a fiscal deficit means, they don't know what a current account is . . . The economic variables that influence their electoral decisions are how much peso volatility there is, how much inflation there is, poverty and consumption. In these four categories, people believe that things nowadays are worse than when Macri started.

And until he can find a way to make progress on these issues, the situation is only going to get worse from here.

0 comments:

Publicar un comentario