Banks are still the weak links in the economic chain

©James Ferguson

©James Ferguson

Why have the prices of bank shares fallen so sharply? A part of the answer is that stock markets have declined. Banks, however, remain the weak link in the chain, fragile themselves and able to generate fragility around them.

The decline of European stocks was a little bigger than that of US ones but the underperformance of the European banking sector was similar. Relative to the overall US market, the index of shares in US banks fell 9.1 per cent, while that of European banks fell 11 per cent relative to European markets — and so only a bit more.

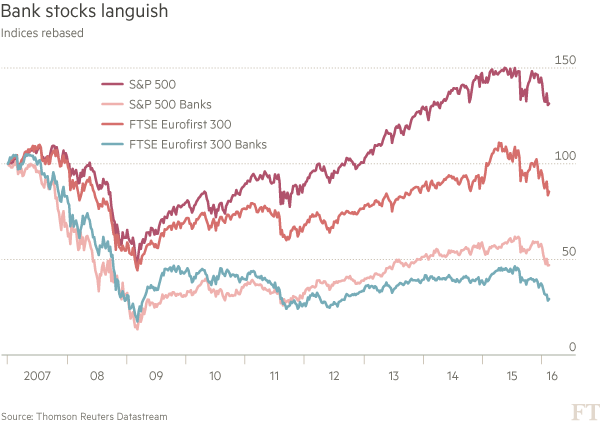

The dire performance of European banks becomes more evident if one takes a longer view.

Bank stocks have failed to recover the huge losses they suffered in the wake of the financial crisis of 2007-09. On February 15 2015, the S&P 500 was 23 per cent higher than on July 2 2007 but the US banking sector was still 51 per cent below where it had been then; the FTSE Eurofirst was 21 per cent below its 2007 level, reflecting the botched European recovery, but its banking sector was down by 71 per cent. In the European case a decline of 40 per cent in the value of bank stocks would return them to the 2009 nadir.

So what might explain what is going on? The short answer is always: who knows? Mr Market is subject to huge mood swings. Yet a vital consideration, particularly in the US market, is that Robert Shiller’s cyclically adjusted price-earnings ratio is at levels substantially exceeded only in the stock market bubbles that peaked in 1929 and 2000. Investors might simply have realised that the downside risks to stocks outweigh the upside possibilities.

One might be anxious about a slowdown in the American economy, partly driven by the strong dollar, weakening corporate profits and a misguided commitment to tightening by the US Federal Reserve.

One might be concerned over the need for sovereign wealth funds to liquidate assets to fund fiscally stressed governments, particularly of the oil exporters. One might worry about a big slowdown in China and the ineffectiveness of its government’s policies. One might fear another crisis in the eurozone. One might be worried about geopolitical risks, including the threat of war between Russia and Nato, disintegration of the EU and the chance that the next US president will be a hardline populist.

One possible response is that it is the euphoria over China that is over. A better response, however, would be that the high-income economies have not yet recovered from the financial crisis and subsequent eurozone crisis, as ultra-low interest rates show.

This array of worries, and particularly the ongoing deflationary pressure, throws a sharp light on the plight of the banks. Banks are highly leveraged plays on economies. If economies are sick, banks are likely to be sicker. Worse, the sicker the banks, the sicker will be economies.

Worries about banks are shown now not only in the price of their stocks, but also dramatically so in the prices of contingent convertible bonds, or cocos. These bonds are hybrids: debt in good times but convertible into equity when common equity becomes too small relative to banks’ balance sheets.

The collapse in the prices of cocos of a number of banks can be seen either as proof that they work or as the possible beginning of a death spiral, in which the signal of stress dries up the funding of fragile banks more broadly.

Why should banks be so fragile after all the vaunted re-regulation? One answer is that they remain highly leveraged. If one ignores the vanishing trick of risk-weighting, the true leverage of many large banks remains at more than 20 to one. Another answer is that banks are exposed to almost everything.

Poor market conditions undermine their returns from broking and wealth management. The threat of deflation increases the likelihood of negative interest rates on reserves. The effect of that on the banks is uncertain but also worrying.

At least as important is the flattening of the yield curve as returns on longer-term bonds collapse. A flat yield curve is bad for the profitability of banks, whose business is to borrow short and lend long. Commodity-price falls also raise worries about solvency of borrowers. A bigger issue is the new rules on resolution of banks in difficulty. These threaten creditors with forced conversions into equity. For shareholders, that would mean dilution. For creditors, it would mean unexpected losses.

The world economy is not necessarily heading for a crisis, it is probably just heading for a slowdown — but risks abound. Moreover, such risks are bound to affect banks, particularly those of bank-dependent Europe. The weakened banks will then damage economies.

Policymakers must remain aware of these downside risks and do what they can to avoid adding to them. One thing remains clear: banks are still the weak links in the global economic chain.

People worry about the health of these huge, highly leveraged, extremely complex and opaque behemoths. They are undoubtedly right to do so.

0 comments:

Publicar un comentario