O, O, O, It's Magic

by: Brad Thomas

- All triple-net REITs grow earnings by utilizing spread investing.

- The higher the multiple, the lower the costs of capital, and that translates into BIGGER MARGINS.

- The low cost of capital (high equity multiple) is the most important competitive advantage in the net lease industry.

This article is one in a sequence of articles that I refer to as “If I Had To Own Just One REIT” series. As you may recall, I recently wrote on the Healthcare REIT sector and I selected Ventas, Inc. (VTR) as my top pick. I summed up my BUY recommendation as follows:

VTR is my favorite Healthcare REIT and one of the best managed REITs overall. While I don't consider the shares anywhere near bargain-pricing levels, I consider the stock soundly valued and worthy of an entry position. For a deep value investor, I would wait on a pullback, but I have no problem recommending shares at the current price point.

I also wrote on the Shopping Center REIT sector and I explained that “after surveying the list of vetted retail REITs and considering which of the companies are worthy of ownership, I find Retail Opportunity Investments Corp. (ROIC) one of the best REITs to own.”

Given the more recent news and powerfully disruptive force in the retail sector – Amazon (AMZN), it’s critical that investors focus on QUALITY. As I explained in a recent Forbes article,

The best quality real estate with the highest sales productivity should thrive as successful retailers want to drive sales and inventory turnover..., Amazon is recognizing that to build a successful mousetrap, the blueprint must include REAL ESTATE.

In other words, it’s now more critical than ever to own Retail REITs that have the highest quality assets. There is no reason to be cute, hoping to capture outsized returns by investing a REIT like Spirit Realty (SRC) that leases to Shopko and formerly invested in a struggling grocer, Hagen. I summarized my thoughts in a recent article,

The cream always rises to the top, and today REIT investors have an opportunity to pick up shares in a stalwart REIT that has a superior low cost of capital advantage. It’s critical to always examine the underlying revenue generators of a REIT and remember that “quality is not free.

Now it’s time to continue the “If I Had To Own Just One REIT” series and today I’m writing on the Net Lease REIT sector. I’m sure you already know the company but in case you don’t here’s a clue…. O, O, O, It’s Magic.

The Basic Net Lease REIT Overview

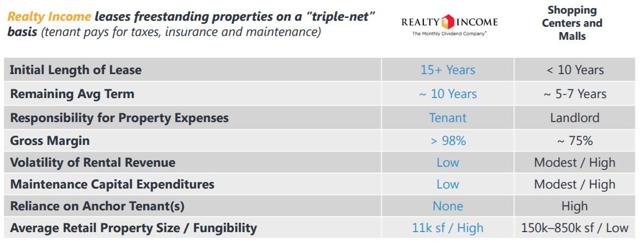

Before I start on the discussion of Realty Income (O), let’s begin with a general overview of the Net Lease REIT sector. Net Lease REITs are different from Shopping Center REITs because their lease structure and growth drivers support a predictable revenue stream relative to other forms of retail real estate. This snapshot below compares Realty Income (and Net Lease REITs) with Shopping Center/Mall REITs:

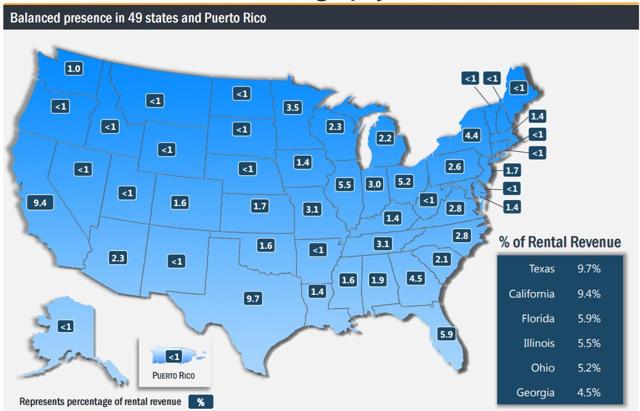

One of the most important differentiators for Net Lease REITs is that they drive growth through acquisitions. When is the last time you saw a Mall REIT acquire a Mall? Net Lease REITs like Realty Income have a large pool to fish in – the sector is highly fragmented and there are opportunities to invest in practically every state in the U.S. (Realty Income owns properties in 49 states).

Here is a snapshot comparing Realty Income’s market capitalization with the Net Lease REIT peers:

Over the years, Realty Income has evolved into a massive Net Lease REIT with 4,980 properties located in 49 states and Puerto Rico. As you can see below, the company has a highly diversified portfolio spanning 49 states (not in HI):

It’s hard to fathom how much Realty Income has grown over the years, from one Taco Bell site to over 4,900 properties. The company now has incredible scale, well diversified by tenant, industry, geography, and to a certain extent, property type.

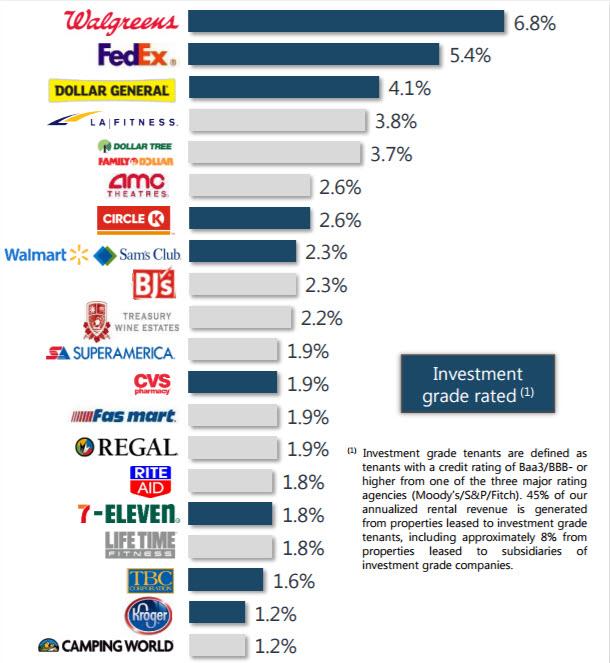

No tenant represents more than 6.8% of revenue as Realty Income has 250 commercial tenants, 45% are investment-grade rated (including 9 of the top 20 tenants):

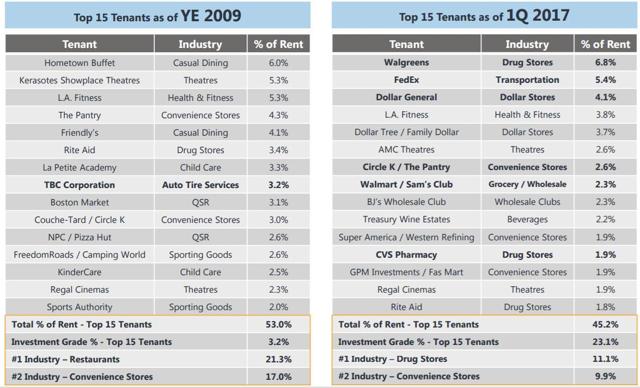

As you can see, Whole Foods is not on the list of Top 20 tenants. During the first quarter, Realty Income added Kroger (NYSE:KR) to its top 20 tenants, representing 1.2% of annualized rental revenue. But more importantly, the top 15 tenants represent higher quality credit, less cyclical industries and greater diversification vs. 2009:

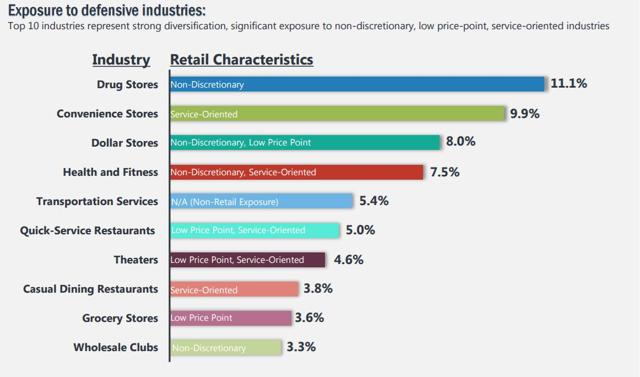

No industry represents more than 11.1% of rent and the company has considerable exposure to defensive industries: Top 10 industries represent strong diversification, significant exposure to non-discretionary, low price point, service-oriented industries:

Realty Income’s roots are in retail with growing exposure to mission-critical industrial properties:

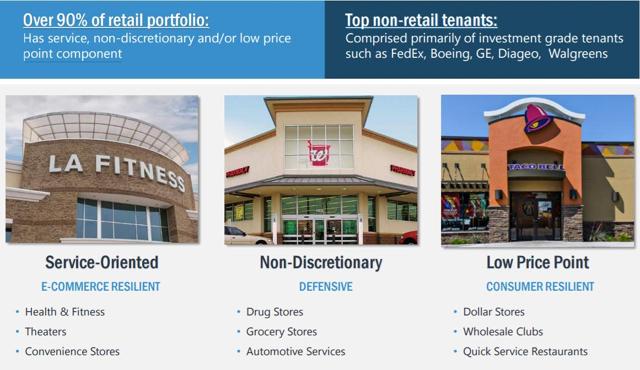

Realty Income’s management team is highly experienced at sourcing deals and when the company invests in retail it seeks strong unit-level cash flow coverage (specific to each industry). The company seeks tenants with service, non-discretionary and/or low price point components to their business with favorable sales and demographic trends.

Keep in mind, there have been 13 retail bankruptcies in 2017 and 12 of them were related to apparel, electronics, and general merchandise. Realty Income has little exposure to these categories: 5 apparel BKs and O has 1.8% of ABR in apparel, 3 sporting goods BKs and O has 1.3% of ABR in sporting goods, and O has .30% exposure in electronics, 1.7% in general merchandise, and just .65% exposure in shoes (i.e. Payless BK).

Also, Realty Income has 3.67% exposure (based on ABR) to the grocery sector. The company has Wal-Mart and Kroger as Top 10 tenants. As I said earlier, it’s critical to invest in quality retail and that means avoid REITs that have exposure to weaker chains like Shopko (i.e. SRC) and Bi-Lo (i.e. WHLR).

What about Rite Aid (RAD)?

Of all of Realty Income’s tenants, Rite Aid is, in my opinion, the biggest watch list candidate. There is doubt regarding the Walgreen merger and RAD is highly leveraged (rated B by S&P). Realty Income has 69 RAD stores but I don’t consider this dire news given the fact that Realty Income has cherry-picked the real estate and the pharmacy sector is growing.

Who knows, maybe the RAD leases become Amazon leases… I’ll save that article for another day…

Realty Income remains comfortable with the momentum in the drugstore industry and continues to view the exposure favorably given the industry’s attractive demographic tailwinds, non-discretionary nature and continued growth from in-store pharmacy pickup.

Additionally, Walgreens and CVS (the top two drugstore tenants) have generated 15 consecutive quarters of positive same-store pharmacy sales growth.

Most importantly, over 90% of Realty Income’s retail portfolio has service, non-discretionary and/or low price point components. The Non-Retail-focused investments are Fortune 1000, primarily investment-grade rated companies.

The Magic Starts Right Here

All triple-net REITs grow earnings by utilizing spread investing; this simple formula is described as follows:

Cap Rate - Cost of Capital = Spread

By using this example, assume a triple-net REIT acquires standalone buildings at a 7% cap rate, and then, after subtracting the cost of capital (~5%), arrives at a spread (that's the profit margin) of ~2% (or 200 bps).

Over the years, I have been reading many articles on Seeking Alpha and other investing websites, and I'm amazed that most analysts miss the "most important thing" when it comes to net lease investing:

The Low Cost of Capital Advantage.

Let's consider the equity details related to spread investing.

To arrive at the earnings yield, one must divide the P/FFO ratio into 100. For example, a P/FFO of 21x divided by 100 is a 4.7% earnings yield. Since assuming Wall Street charges around 6.5% for equity, the earnings yield after issuance costs is .935 (100% - 6.5% = 93.5%).

So, the Nominal Cost of Equity is arrived at by dividing the 4.7% earnings yield by .935, or 5%.

With a 7% cap rate (on a purchase), the 5% NCE is equal to 2.0%. Thus, on a $100 million investment, there is $2 million in new profits for all shareholders. The same thing at 25x P/FFO equals a 4.27% NCE that translates into around $2.73 million (in profits) on a $100 million acquisition.

So, very simply, the higher the multiple, the lower the costs of capital, and that translates into BIGGER MARGINS.

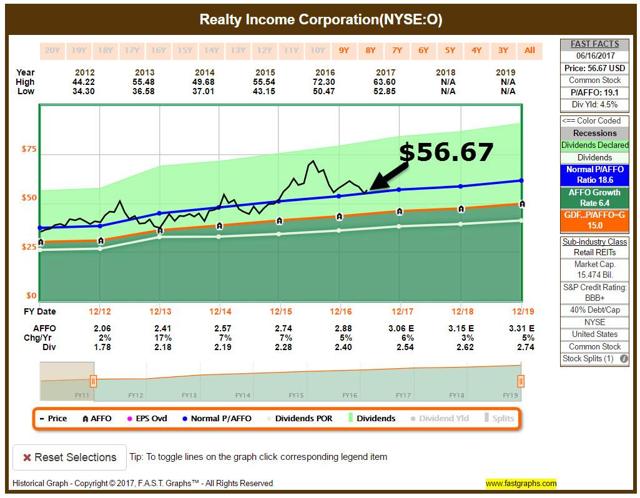

AFFO yield = Annualized 2017 estimated AFFO ($3.06) divided by $56.67 stock price = 5.39%

Estimated cost of 10-year debt = 3.60%

Nominal Cost of Free Cash Flow = 0%

66% equity = 5.39% * (0.66) = 3.56%

34% debt = 3.60% * (.33) = 1.22%

WACC = 3.56% +1.22% = 4.78%

(In reality, it's actually lower than that, because O uses free cash flow instead of equity. Cash has a 0% nominal cost.)

Realty Income’s investment spreads relative to its weighted average cost of capital remained healthy in the first quarter, averaging 170 bps, which were well above the historical averages. Realty Income defined investment spreads as initial cash yield less the nominal first year weighted average cost of capital.

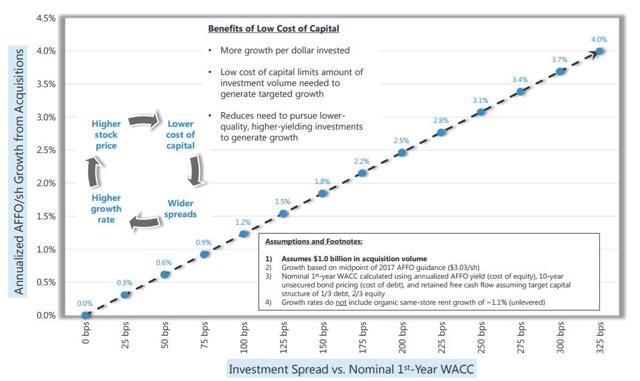

As illustrated below, the low cost of capital (high equity multiple) is the most important competitive advantage in the net lease industry:

Low cost of capital allows Realty Income to acquire the highest quality assets and leases in the net lease industry:

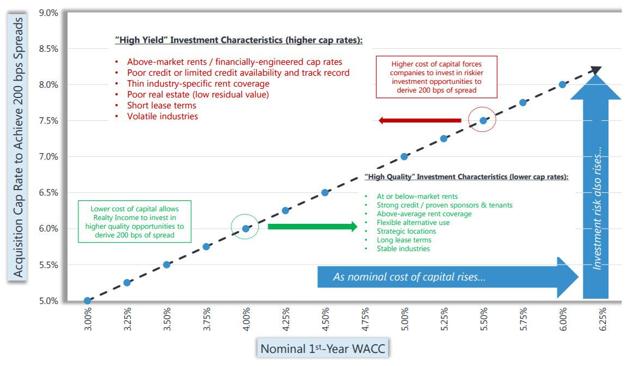

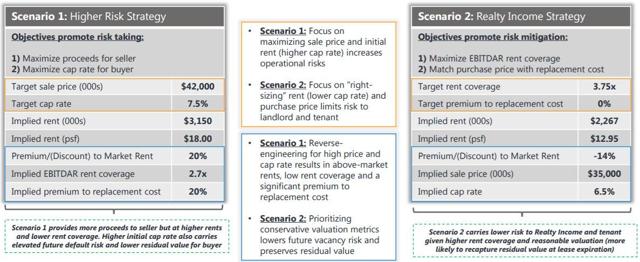

Realty Income avoids lease structures with above-market rents, which can often inflate initial cap rates:

Assuming identical real estate portfolio, consider two different lease structure scenarios...

Realty Income’s cost of capital advantage drives ability to source, fund, close on accretive M&A deals, like the ARCT transaction that closed in 2013:

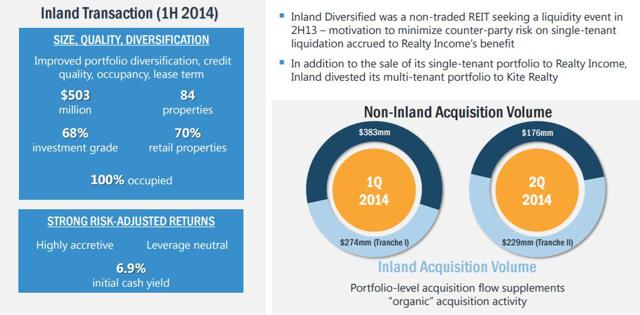

Large, diversified portfolio offers capacity to absorb co-mingled portfolio opportunities, like the Inland portfolio that closed in 2014:

Realty Income’s property diversification, cost of capital, and willingness to acquire $250mm+ transactions with diverse property types provides unique growth opportunities in addition to traditional single-asset or retail sale-leaseback pipeline.

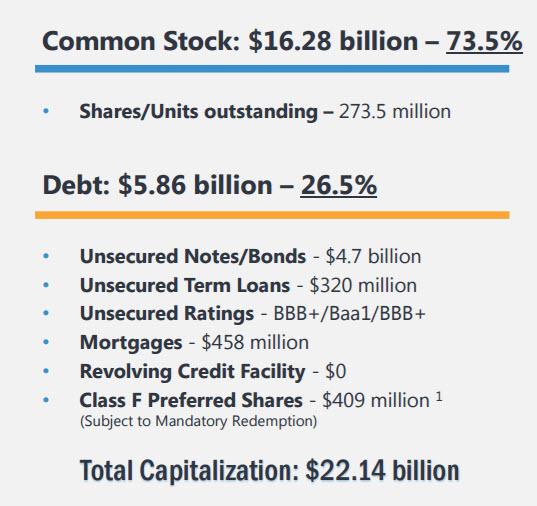

The Fortress Balance Sheet

In the first quarter, Realty Income issued approximately $800 million in common equity at an average price to investors of approximately $62 per share (trading at $53.76 now).

Realty Income has the highest credit rating in the net lease sector, the company issued $700 million in fixed rate unsecured debt with a weighted average term of 18.3 years and a yield of 4.1%.

The company’s credit spreads remain among the lowest in the REIT industry and leverage continues to decline with net debt to total market cap of approximately 26% and debt to EBITDA of approximately 5.5x. Realty Income currently has approximately $1.5 billion available on its $2 billion line of credit. This provides ample liquidity and flexibility as the company continues to grow.

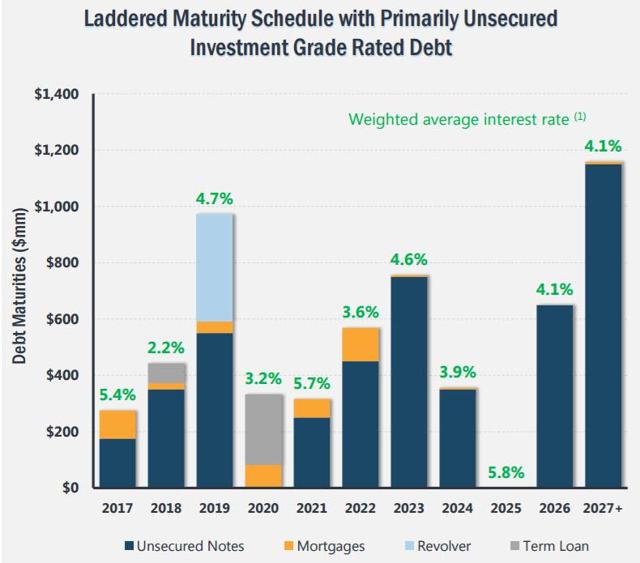

The company is rated BBB+ by all three major rating agencies (Moody's, S&P, and Fitch), and is likely to become an A- rated REIT soon. Key metrics include: 93% fixed-rate debt, weighted average rate of 4.15% on debt, staggered maturities (8.1 year on average), and ample liquidity ($1.68 available on revolver (L+90bps) with $120 million (annually) of free cash flow.

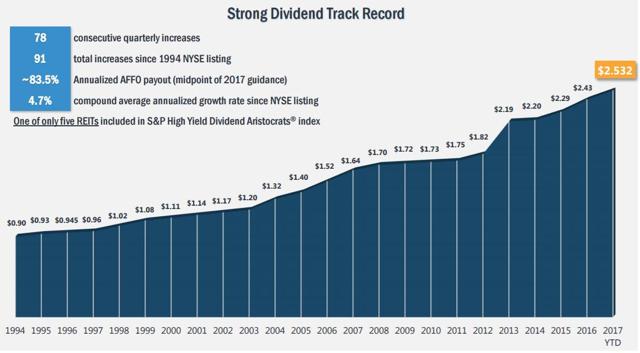

O, O, O, It’s Magic

What company would copyright the name, “the monthly dividend company” if they did not intend to generate reliable monthly dividends?

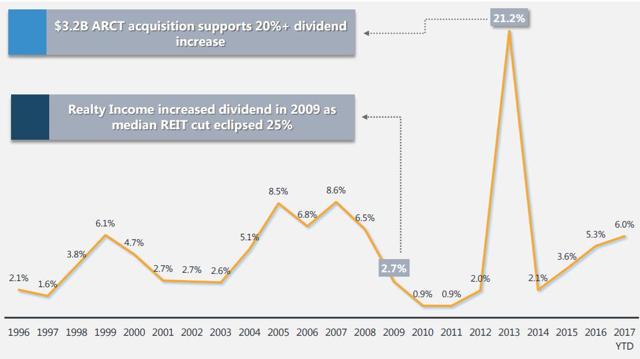

As you can see, Realty Income has had Zero dividend cuts in 22 years as a public company:

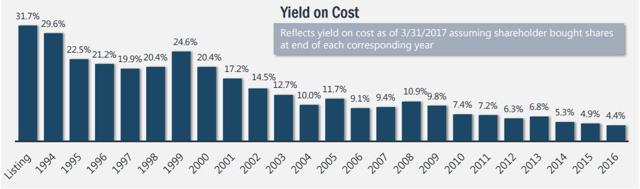

The “Magic” of Rising Dividends: Yield on Cost, Dividend Payback long term, yield-oriented investors have been rewarded with consistent income. There are potential benefits to investing long term in a company that regularly increases its dividend. The longer you hold your shares, the higher the yield you will receive on your original investment, assuming dividends increase over time. Additionally, the compounding of reinvested dividends could generate increased investment returns over time.

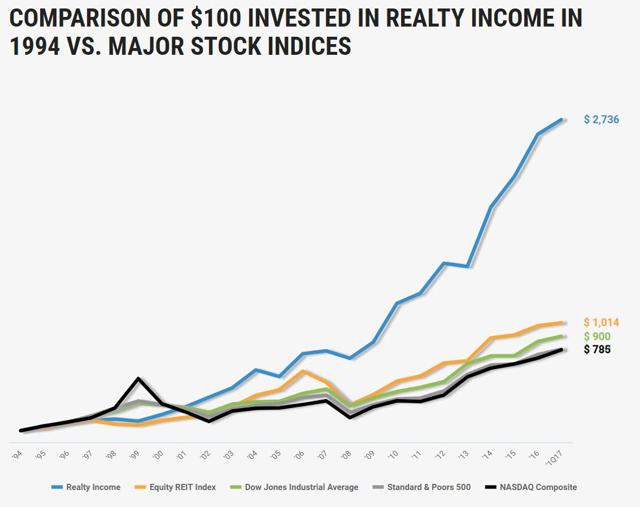

Investors who have elected to reinvest their dividends have enjoyed the following returns over time (as of 3/31/2017):

Buy, Sell, or Hold?

Keep in mind, Realty Income’s share price (of $72.00) is down considerably over the last 11 months.

The dividend yield has compressed by 230 bps, representing a cushion for investors (Note: I had a “Trim” on shares at $72.00).

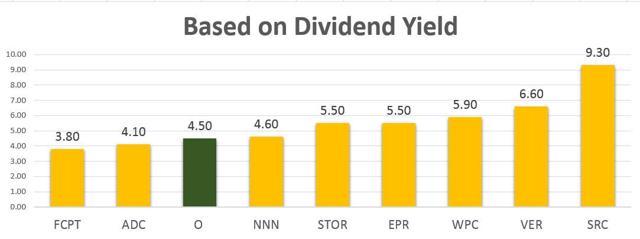

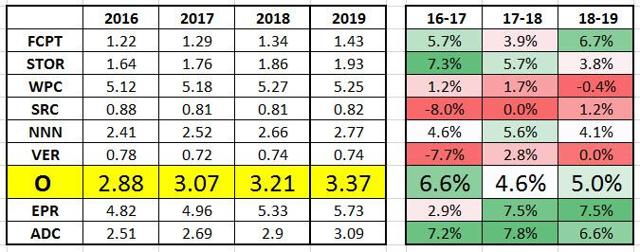

Let’s examine Realty Income’s dividend yield, compared with the peers:

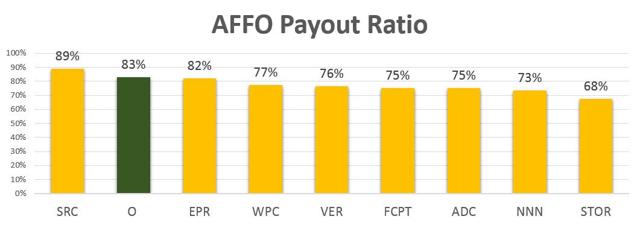

Now let’s examine the AFFO Payout Ratio:

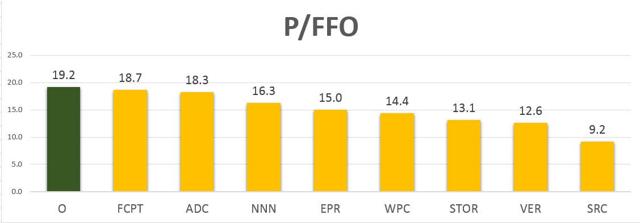

Realty Income's Payout Ratio is higher than most peers, but the company does not have considerable office exposure and the quality of the income stream justifies the low 80% ratio. Now let’s examine the P/FFO multiple:

As you see, Realty Income trades at the highest P/FFO multiple in the Net Lease REIT sector, but that does not mean shares are expensive. I would argue that shares are now “soundly” valued and that the premium valuation (relative to the peers) is warranted based on management’s skillful strategy for managing risk. Obviously, I would encourage investors to buy Realty Income if the price drops, but I consider fundamentals sound and I’m maintaining my BUY recommendation.

Although the Amazon/Whole Foods deal was a surprise last week, it should be no surprise that Realty Income has been able to successfully manage risk for more than two decades. The fact that Amazon is betting on brick and mortar serves to validate the argument that real estate is an essential asset class for delivering goods and Realty Income remains in an enviable position to be the dominant Net Lease consolidator.

In conclusion, if I had to buy just one Net Lease REIT, it would be Realty Income... O, O, O, it's magic!

AFFO per Share Forecaster (powered by FAST Graphs):

Author's note: Join me at the DIY Investor Summit where I share detailed tips on my core investment strategies, top advice for DIY investors, and specific ways I'm positioning for the second half of 2017.

Brad Thomas is a Wall Street writer, and that means he is not always right with his predictions or recommendations. That also applies to his grammar. Please excuse any typos, and be assured that he will do his best to correct any errors, if they are overlooked.

Finally, this article is free, and the sole purpose for writing it is to assist with research, while also providing a forum for second-level thinking. If you have not followed him, please take five seconds and click his name above (top of the page).

Sources: FAST Graph and O Investor Presentation.

0 comments:

Publicar un comentario