Open

Letter to the President, Part Five

By John Mauldin |

When

the next president of the United States walks into the Oval Office on Saturday,

January 22, after the heady experience of Inauguration Day followed by numerous

balls, he or she will be confronted with significant economic challenges. This

is the fifth and I hope final installment in a series of letters I’ve written

to the next president on those challenges. The first three letters in the

series dealt mostly with the realities of the economic landscape beyond the the

United States. The situations that most of our significant trade partners face

dictate that the next US president will have much less room to operate than the

candidates have suggested that they’d like to have.

Europe

will be struggling not to fall apart. The budgets of most European countries

are going to be even more constrained than the US budget will be. China will be

lucky to escape a hard landing within the next four years. The same can be said

for many other countries that are dependent on global trade in an era when

trade is actually slowing.

My

basic thesis is this: Without significant changes in tax and incentive

structures, the US will almost assuredly enter a recession within the next few

years. Then, if we lose tax revenues only to the extent we did in the last

couple of recessions, we’ll be saddled with a deficit of over $1.3 trillion,

and the deficit won’t fall below $1 trillion as far out as the eye can see,

according to the nonpartisan Congressional Budget Office (CBO).

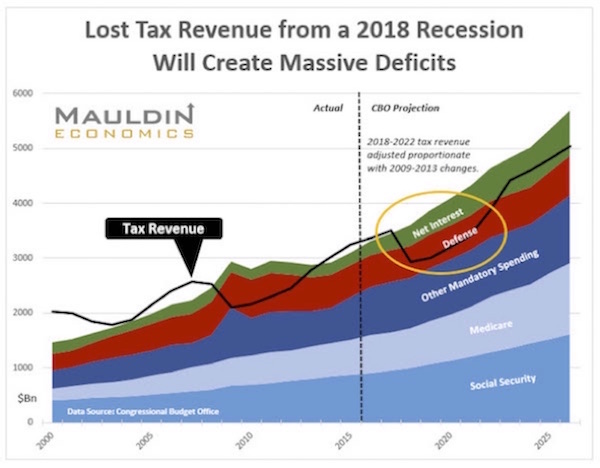

It

appears to me that the CBO projection understates the real issue; in fact, the

CBO may be viewing things through rose-colored glasses. They don’t project a

recession for the next 10 years. The above chart depicts my estimate of what

would happen if we were to encounter recession two years from now. But it

doesn’t include the constant revisions upward to the cost of Medicare and

Medicaid and other entitlements. Just this week we learned that one portion of

Medicaid is going to cost well over $1 trillion more over the next 10 years

than was projected in the current budget. So add another $100 billion dollars

of deficit a year. Such revelations are constantly coming at us. My estimate

also doesn’t take into account how fragile the lower-income echelons of the US

economy are today. They will probably require even more income and healthcare

support, meaning larger deficits for the US and extremely constrained state and

local budgets.

Unless

something is done to counter these trends – and I do not mean tinkering around

the margins – this is going to be the reality that you as president will face

in the next four years. There are those who have warned for many years of a

debt crisis.

They have looked like stopped clocks. But like any stopped clock,

they are getting ready to be right this once. Paul Krugman and others who

pooh-pooh the concept that debt is a problem may soon get to see what it’s like

to deal with a true economic crisis. Of course, they will want more

quantitative easing by the Fed and federal debt issuance to relieve the

suffering; but we know now that QE does little for Main Street.

Instead, it

simply helps the rich maintain their asset prices, and deficit spending digs us

deeper into a fiscal abyss. We could of course monetize the US debt, but that

course would bring its own major negative repercussions.

My aim

with this series is to present you, as the potential new president, with a series

of options that I think will not only help us avoid the next crisis but set us

up for a decade or more of true prosperity and put us back on the path of 3% to

4% annual growth for the next 10 years. And one of the few things that Krugman

and I can agree on is that the only way to get out of this crisis is to grow

our way out.

While

this series has been more popular than I expected it to be – and even US

senators are tweeting about it – there have been those who question how

realistic it is to think that my proposal might win acceptance. And sadly, I

think they have a point. Enacting radical proposals along the lines I am

suggesting will not be politically easy. So next week – in case we don’t pull

our act together in time to avert a crisis – I’m going to outline what we can

do if we fall into recession again. I’ll also propose how we can end the

dysfunctionality in Washington DC. While I’m not advocating an actual

revolution, my proposal is quite revolutionary, and it already has a

significant movement supporting it. And, who knows, maybe in the midst of a

crisis we’ll make good on what Winston Churchill used to say about us: “You can

always count on the Americans to do the right thing – after they have tried

everything else.”

But

before we get into the heart of the letter, let me give you an update on my

Strategic Investment Conference, which will be held in Dallas this coming May

24–27.

We have been able to work out some additional space and accommodations

with the Hyatt hotel here in Dallas where the event is being held, so we have

told all those who were on the waiting list that they can now enroll. We also

have a small number of additional spaces available. Since we don’t want to find

ourselves with more attendees than we can handle, we are going to continue to

employ a waiting list.

First-come, first-served.

If you

want to attend, I suggest you go to the Strategic Investment Conference website (click

on the link) and register to have your name put on the waiting list. I can

almost guarantee that the new seats now available will disappear, as there

aren’t not that many; so don’t procrastinate. Those who wait until the last

month to register are going to be disappointed.

I

won’t even tease you with the fabulous new speakers that we are adding every

week. The lineup just keeps getting better and better.

By the

way, I was looking through the list of attendees. There are almost 100 people

from outside the US already registered. I see a lot of familiar names, and we

could easily put together a fascinating conference just from the attendees. We

are evaluating two different computer apps that will, among other things,

significantly enhance attendee networking.

One of

the comments I have heard over the years is that people would like to be able

to network more effectively with other attendees, but they do not always know

whom they want to meet. Whichever app we choose, it is going to allow you to

find and grow a network of people who share your interests. This is one time

you really want to be in the room if at all possible. Now to our letter.

Let’s

summarize where we are. Last

week I showed you where to find $2 trillion for infrastructure development

by repurposing the Federal Reserve’s balance sheet.

What I didn’t mention was

that, while the whole trillion obviously cannot be put to work the first year

(given the nature of infrastructure timelines), it is not unreasonable to

expect that $400 billion in annual expenditures could be reached within three

years. There are 122 million people working in the US today, in an economy of

roughly $20 trillion. We could easily expect that our $400 billion a year to

translate into more than two million jobs and perhaps even more, as

infrastructure development is generally more labor-intensive than many other

activities are. And these jobs would generally be higher paying than most

service jobs, so this initiative could deliver a serious stim ulus for the

economy, helping us steer clear of recession.

And if

you do the authorizing legislation correctly, it could be the gift that keeps

on giving. As these bonds are paid back to the Federal Reserve, the Fed could

use the money coming in to fund even more infrastructure construction. Your

presidential legacy might well include leaving the country’s infrastructure in

its best shape in 100 years and continuing to improve. Not a bad day at the

Oval Office.

Then I

showed you how restructuring the corporate income tax – about which there is

already quite a lot of bipartisan agreement – would offer a radical boost to US

business, especially export businesses, and generate modestly more revenue by

eliminating all deductions. Of course, a lot of K Street lobbyists would have

to look for new jobs; but they are reasonably well educated, and I’m sure they

could find something to do that would actually be more constructive .

But we

come to a real sticking point as we begin to figure out how to navigate the

budget.

Taxing foreign-earned revenue and growing the economy will only

modestly increase the revenue stream from taxes in the short term. To offset

the trillion-dollar deficits that the economy will be racking up in just a few

years, you’ll need more than modest revenue growth.

There

are really only three ways to deal with the deficit. You can increase taxes,

cut spending, or borrow money. You will notice that there is at least one party

in Congress generally opposed to two out of those three. It’s an existential

dilemma for Republicans to allow taxes to increase or for Democrats to cut spending,

especially on entitlement programs. Yes, Republicans would be willing to cut

some entitlements, and Democrats would be willing to cut some defense spending,

but both parties are just tinkering around the edges and won’t get you to where

you need to be.

One

stubborn problem is that US voters want a lot of healthcare but don’t want to

pay for it. Yet maintaining the healthcare services and entitlement programs

that we have today will require more money. There’s just no way around it.

In

order to get the revenue you need, you are going to have to convince both

parties to compromise on issues that both have sworn never to compromise on.

And proposing traditional compromises in the current political environment is

simply not going to work. You can try until you’re blue in the face, but

nothing will happen, and we’ll lurch toward a truly fundamental economic crisis

that all the infrastructure spending in the world won’t fix.

So

let’s step entirely outside the box and figure out how to give both parties

something they want so badly that to get it they’ll be willing to

compromise on what the other party wants. And we have to do this in such a way

that the bulk of the American people see a significant improvement in their

lives and in their paychecks.

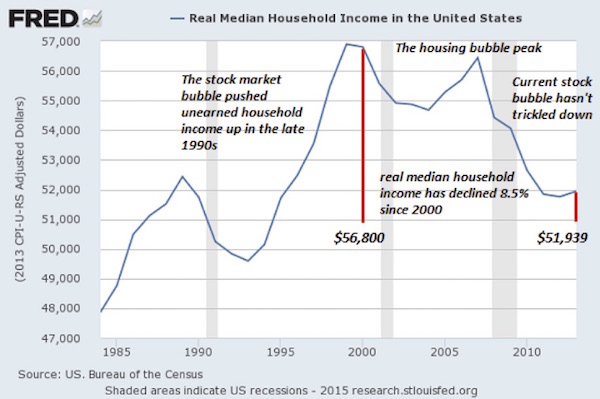

To

craft a solution, let’s look first at what has happened to the average American

worker. There is a reason that large numbers of voters in both parties are

frustrated. The charts that follow tell better than 1000 words could why that

frustration is warranted. For all the crowing about how quantitative easing has

helped, it has mostly helped Wall Street and the top 20% of earners. Median

income in the United States is down 8.5% since 2000.

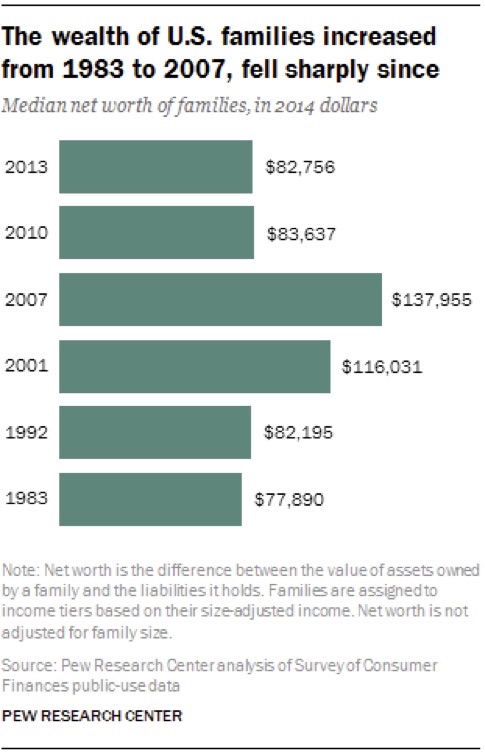

The

median net worth of US families has fallen sharply since 2007 and is roughly

back to where it was 24 years ago:

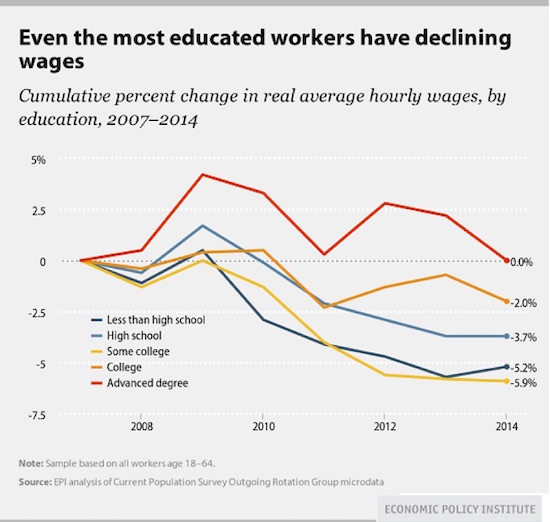

And

that economic malaise is affecting all education groups. Even those with advanced

degrees have seen their incomes stagnate since 2007:

And

while incomes have stagnated, the real cost of goods and services has increased

much more than the purported inflation rate suggests. The cost of housing,

utilities, and local taxes has certainly increased beyond inflation levels. And

don’t even get me started on how much has gone up, crushing families who can

least afford it.

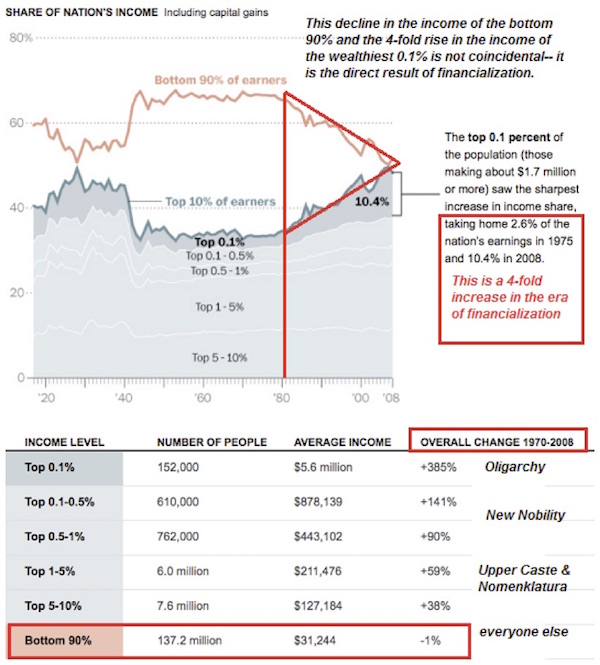

This

next chart paints our economic situation in even starker terms. The bottom 90%

of Americans have seen their overall income drop. Low interest rates and

quantitative easing have dramatically helped the top 10%, and we could break

out the numbers to show that it’s actually the top 25% that have benefited, though

the further down the income chain you go, the less the Fed’s tinkering has

helped. The financialization of America is directly responsible for this turn

of events, and rather than helping GDP growth as it was intended to do, it has

thwarted growth.

You

need to do something, something radical, to shake up the system, to make sure

those at the bottom get an increase in income all the while making sure that

you don’t push the economy, which is already stalling, into a dive. Economics

and politics as usual simply will not cut it.

Giving Everybody Some of What They Want…

But Not Everything They

Want

Here

is the basic political reality you’re dealing with. Republicans want

supply-side tax cuts and flat taxes, spending cuts, and a balanced budget, or

some combination of all of them. Democrats want more spending for healthcare

and other consumer-related items, an agenda that means higher taxes; and many,

if not most, would at least give a nod to balancing the budget. Everyone is for

“the little guy.”

So

let’s start with the easy part. You’re going to want the Republicans to go

along with an increase in the total tax revenue. If you forget for a moment

where you want to extract that revenue from (by taxing the rich, for instance)

and just say that your goal is to get more tax revenue, then you will have a

lot more flexibility. And the reality is that you could significantly raise

taxes on the rich (and by “the rich” I mean the top 20% in income) and still

get nothing close to the amount you need. The sad reality is that you would

have to raise taxes not only on the rich but on the middle class in order to

make a difference. And I’m going to assume that raising taxes on the

beleaguered and shrinking middle class is a nonstarter for pretty much

everyone.

So to

get what you want, give the Republicans a tax cut that will get every one of

their little supply-side hearts absolutely quivering in anticipation. Give them

so much of what they want that it becomes almost impossible for them to say no.

That means you can’t be halfhearted; you’re going to have to go the whole hog.

Offer

a 20% flat tax on income over $100,000. Period. No deductions for anything.

Dividends, interest income, municipal income tax revenues, all are taxed at 20%

above the total $100,000 income level. Every

sacred cow goes. No mortgage deductions, no charitable contribution deductions,

no child tax credit, no nothing.

Every penny over $100,000 is taxed at 20%.

Now, you can make an argument that income from say $50,000–$100,000 should be

taxed at 10%, but that’s not going to give you enough money to do what you need

to do in order to be able to get the support of the Democrats. There is, on the

other hand, a case to be made that people making over $50,000 should contribute

something to the overall general welfare of the economy.

That

still gives everyone up and down the ladder a major tax cut. There is not a

supply sider in America who is not going to like that tax structure. Your

income tax filing is done on a 3”x5” card. If you made between $50,000 and

$100,000, you pay 10%. If you made more than that, you pay $10,000 plus 20% of

everything you made above $100,000. This is going to be surprisingly popular

with millennials: survey after survey shows that one of their big fears is

dealing with the IRS. In a world where 40% of America is now getting some form

of non-salaried income, dealing with the IRS is becoming more complicated.

Millennials are increasingly part of the gig economy, and a flat tax will make

their lives easier. You are going to be surprised at the level of support this

tax proposal will get from young people.

Now,

this tax structure is, of course, going to make people who want to soak the

rich unhappy, as they don’t see how the little guy benefits. So here is where

we have to get really creative. And this is why you are giving the Republicans

something that’s going to be very difficult for them to walk away from: you’re

going to combine their tax cut with two additional items.

To the

Democrats, offer to abolish the Social Security tax on both sides of the

equation, both business and personal. That means an individual making $30,000 a

year gets an approximately $2000 pay raise immediately. Every working man and

woman gets a pay increase in the form of no deductions for Social Security

taxes from their wages.

So

where do you get the money? You’re certainly not going to get the support of

senior citizens or anyone else for that matter if you start messing around with

the ability to pay Social Security benefits. So that means we have to find

another revenue source.

And

for that revenue source you need to turn to the tax that is the most efficient

in economic terms: a consumption tax. But not one that looks like a sales tax.

Rather, it should be a version of what almost every other country in the world

uses, and that is a value-added tax, or VAT. I would modify it to look more

like a business transfer tax (BTT).

Basically,

with a BTT, a company pays tax on the revenue it receives net of what it pays

for the services and products it is selling. Netflix pays on the revenue it

receives after deducting the money it sends to television and movie producers

for the rights to show their products. This is all transparent to the end user.

You

can tinker around the margins to make this tax more politically acceptable. You

can exempt groceries, but then you’re going to have to charge a higher rate on

everything else. You can exempt nonprofits, but I wouldn’t: they pay Social

Security tax on their employees now. But that may be the price of getting the

deal done.

A BTT

in the low teens (12-14%) will get you all the revenue that you need. You look

the Republicans square in the eye and say I want to get 2% of GDP more tax

revenue in the form of the BTT in return for the income flat tax on

individuals. By the way, the BTT is legally deductible by US corporations under

WTO rules when they ship products overseas – which is what every other country

does to us, and why they have a tax advantage over us when shipping products to

us. The BTT is going to be a huge boon to US producers. Talk about a cheap way

to boost the economy – this is it.

Now,

Republicans are going to push back and say, yeah, sure, you want to start this

BTT at a low rate today, but the day will come when you want to raise that

rate, just as every European and other country around the world has done. And

you’re going to want to raise those income tax rates again. Why should we give

an inch when you may take a mile in 10 years?

And

your counter to that is to offer to sign a constitutional amendment that will

require a balanced budget and a supermajority of 60% to raise taxes. In theory,

everyone is for a balanced budget (well, almost everyone), and the political

reality is that it takes 60% of the Senate to approve any major new tax revenue

source anyway.

You’re not giving up a lot. Enough Democrats will be willing to

go along, because they’re going to get the extra revenue they need for the

programs they desperately want, and they get a major boost to lower-income

America in the form of no Social Security taxes.

Now,

the hard part for Republicans is that they have to get 38 states to approve

that constitutional amendment. But they’ll just need to fight it out in about

five states (getting 33 more or less red states to approve it shouldn’t be too

hard) in order to get what they really want: certainty about the future of

taxes and the budget deficit in America. You also need to get everybody to hold

hands and sign a pledge to not raise taxes under any circumstances for 10

years. Now, we all know that inside the room a pledge like that is only worth

so much, but it’s at least a start.

Oh,

and for a sweetener, offer to sign a bill to sunset every government regulation

over the next 10 years. Do it in an orderly fashion. Maybe even something like

eliminating 20% of government regulations across the board during your first

term and not letting the absolute number of new regulations increase after

that? If you want a new regulation, get rid of an old one. Force the various

bureaucracies to clean out their attics and stop hoarding regulations that are

way out of date.

And

since I’m from the financial services industry, maybe include one little item

to help the gig economy and the upcoming generation. Make retirement plans

portable from one job to the next so that a young person has an actual

opportunity to build a tax-deferred nest egg.

Taken

together, my proposals amount to a major shift in the tax and incentive

structure of the United States. You won’t be able to implement them all

overnight. I would start with the infrastructure project and the reduction of

corporate taxes, because the former starts to stimulate the economy, the latter

is more or less revenue-neutral, and both boost employment. If part of the

compromise on the reduction of corporate taxes is some kind of lower-tax-rate

amnesty on the $2 trillion sitting outside the United States, that provision

could result in a nice one- or two-year revenue boost. If that tax rate was the

10% I proposed above, there would be $200 billion coming in, which would sure

put a dent in the deficit during the following 12 months.

But

lowering income taxes, introducing a VAT, and reducing the Social Security

burden on businesses and individuals are measures that should probably be

phased in over four years. It would take at least a year just for the various

agencies involved to change their revenue models and infrastructure.

Set a

time limit for balancing the budget. The Clinton/Gingrich budgets did not

balance the budget the first year. It took time. Figure out how much actual

infrastructure can be worked on to boost the economy in the first year, and

then begin to project how those projects will affect growth and how long it

will actually take to balance the budget. My back-of-the-napkin guess is that

4–5 years is reasonable. There is nothing like 5% nominal growth to speed the

process, and holding spending to the level of inflation will bring the budget

under control over time. It will work almost like magic. All you have to do is

make sure that the total budget doesn’t rise faster than inflation. The economy

can then take care of the rest.

The

general objection to the introduction of a VAT in the US is the political

impossibility of getting it done. It is only politically impossible if everyone

doesn’t get something they want. What I have proposed is so politically

delicious to all sides that it becomes possible.

Further,

the lead article in this weekend’s Wall

Street Journal opinion section is a full-throated endorsement of a

VAT, quoting various conservative sources. There are numerous conservative

economists who think a consumption-oriented tax is the smartest and most

economically efficient way to produce government revenue.

Everyone

agrees there are flaws in Obamacare. Depending on who the next president is,

those flaws can be fixed and their budget implications can change. But the

structure I propose above gives both sides more flexibility in getting the

changes they want. Streamlining the healthcare system and giving states more

flexibility will certainly help control costs. There have to be caps on how

much those costs can rise. The American taxpayer is not a bottomless well.

For

those under a certain age, the Social Security rules have to be changed. There

needs to be a change in the law so that the age of retirement is automatically

adjusted upward if the mortality tables show that lifespans are continuing to

increase. (You would be exempt if you were within 15 years of retirement.) This

would eliminate a political hot potato. When Roosevelt first proposed Social

Security, the average person lived only to age 58, and benefits didn’t start

until retirees were 65. Now the average person is living into his or her 80s,

and the average lifespan of those with above-average income is in the high 80s.

(Yes, there are differences in life expectancy depending on income.) Social

Security needs to be means tested.

There

are scores of other ways that savings can be found. There are over 100 agencies

with their own very expensive bureaucracies that do some type of job training.

If this were the private sector, the markets would be screaming for

consolidation.

You

have an enormously difficult task in front of you. If you do nothing but

tinker, you will have a recession on your hands in the early years of your

administration. Just yesterday, real interest rates went negative on the US

10-year bond for the first time. The yield curve is in serious danger of

becoming inverted in real terms. Your economist advisors will confirm that the

research shows the only true predictor of a US recession is a negative yield

curve.

The

research shows that if the yield curve stays inverted for 90 days, a recession

is likely to show up in 12 to 15 months. That means you are not going to have

much time after you’re inaugurated to enact a major stimulus program and

restructure the incentive structure of the US economy. If you wait until we are

already in recession to win cooperation from Congress and get legislation

passed , the negotiations will be more difficult by an order of magnitude. You

need to hit the ground running.

Therefore,

in addition to campaigning after you’re nominated at the convention, you had

better be planning to govern. The economy is not going to wait around for you

to get adjusted to your new position. But what better way to campaign than to

show the voters you are already thinking about how best to serve them?

There

are scores of other major and minor economic topics we could discuss, but these

won’t matter much if we fall back into recession. Unemployment will climb back

to double-digit levels; incomes will suffer; tax revenues will plummet; tempers

will flare and finger-pointing will increase; and you will cornered into being

merely reactive instead of proactive. Foreign policy will take a backseat if we

hit a recession, and your foreign policy choices will be far more constrained.

The first three things you need to be thinking about when you walk into the

Oval Office are the economy, the economy, and the economy. In that order. If we

go into recession on your watch, nothing else you do is going to matter all

that much in terms of the success of your presidency. You can solve the Middle

East crisis, bring peace in our time, and curb global warming. But you will

still be judged by what the economy does.

I’ve

laid out a rough plan that can certainly be adapted and changed. But if you go

with the gist of what I’ve suggested, here are the positives:

- You’re

going to add two to three million jobs during your first term as

president. Most of those jobs will be higher-paying ones, so median income

is going to rise. And because the economy will be booming, employers are

going to have to increase wages in order to attract new workers and keep

current workers. There is nothing like fatter paychecks to improve the

mood of the middle class.

- If

you add jobs and get the economy growing back at 2% to 3%, the Federal

Reserve can begin to normalize interest rates, and savers will stop being

punished. Retirees will be able to make more on their investments and be

more capable of affording a reasonable lifestyle in their retirement

years. Pension plans and insurance companies will have a better chance of

meeting their performance requirements and actually fulfilling their

obligations. I know the issue of retirement plans is not high on your

list, but there is going to be a crisis that you will have to deal with if

we go into recession. So many government pensions are drastically

underwater.

- You

will fix healthcare and entitlement programs in a bipartisan manner that

actually solves their problems rather than kicking these cans – real

toe-breakers now – down the road. You will put the country on a path to a

balanced budget.

- You

will end your first term in office as the most influential president in

terms of economic impact since Franklin Roosevelt.

- The

economy will be booming, and your reelection in 2020 will see you win

nearly as many votes as Ronald Reagan did in 1984.

These

are pretty much your choices: Herbert Hoover or Ronald Reagan?

I wish

you the best of luck, I truly do. We really are all in this together.

With

warm regards,

John

Mauldin

I know

a lot of my readers and friends think I must have gone stark raving mad. I

detoured off the deep end and kept going. I missed that turn in Albuquerque.

Whatever.

I

personally find some of the things that I have suggested to be philosophically

offensive. I can’t imagine there is anyone reading this who thinks every one of

these ideas is actually a good idea. Seriously, if I haven’t offended your

political sensibilities, you are either very flexible or I’m not trying hard

enough.

But

that is the point. We have a deeply divided country. Nearly fifty percent of

Democrats seem to be voting for a full-throated socialist. Sanders is not

socialism lite. He would take us to European socialism and keep right on going,

and there’s a significant contingent of Americans who seem to be with him.

Meanwhile, over 50% of Republicans are saying that what we need is somebody who

is way outside the “establishment,” who will shake things up and do things differently.

Forget on-the-job experience; people no longer trust the current leadership to

get the job done.

Unless

something really odd happens at the conventions, we are going to end up with a

race where the only thing the majority of Americans agree upon is that they

don’t like their choices. The unfavorable ratings of all the candidates in the

final running are extraordinarily high.

I am

seriously, deeply worried that we are going to have a recession in the next few

years. The negative impacts this time around will be every bit as drastic as

they were in 2007–08. Pensions and retirement funds will be devastated.

Unemployment will go through the roof. Monetary policy will be impotent. The

government will be all but nonfunctional, given the current players and system.

A recession this time around is actually going to feel far worse than the last

one did.

Now,

the republic will survive. We’ve actually faced far worse times and come

through them. You can go back and read about those periods – they weren’t fun.

So it’s not the end of the world, but for much of America it could end up

feeling every bit as bad as the Great Depression.

To

stave off such a serious outcome will require radical solutions; and given that

I don’t think any one party is going to have control of the process (which is

not exactly what we’d want anyway), we are going to have to choose between real

compromise and real trouble. What I have tried to do is to propose a program

that actually amounts to a workable compromise.

I

fully recognize that proposing to take another 1–2% of GDP out of the economy

and turn it into tax revenue is heresy among my more conservative friends. I

fully recognize that cutting income taxes to a 20% top rate feels like giving

the rich another get-out-of-jail-free card if you’re a liberal Democrat.

My

goal with this proposal is to create an environment in which the economy can

grow in the 3–4% range, and that rising tide really will raise all boats with

the structure I suggest. Do I think there is much chance of that growth being

achieved? That is the question we will deal with next week, when I will talk

about what we’ll need to do in case my admittedly rose-colored, optimistic

proposals never even make the desk of serious politicians, let alone the next

president.

I’m

looking at my calendar, and although I see a few one-day trips with little or

no time for anything other than meetings, my next real trip has me leaving in

the middle of the month for a short week in Abu Dhabi, then coming back for a

quick speaking gig in Raleigh, North Carolina, before I fly back to get ready

for my own investment conference here in Dallas. Which is good because the

book-writing deadline is looming in the background, along with so many

distractions and things that simply “must” be done. And it seems that most of

that stuff requires me to spend time in front of my computer. Then there are

the never-ending meetings and phone calls. I’m in the process of making

significant changes in my core investment business, and that project really

requires a great deal of personal involvement. Some things you just can’t

delegate.

If you

are still with me, you are overly patient; and so rather than conclude with a

few personal remarks, which is how I normally close the letter, I am simply

going to tell you to have a great week.

Your

concerned about his country analyst,

John Mauldin

0 comments:

Publicar un comentario