Hopes that the trade war is easing have buoyed the European auto sector in recent weeks, but another profit warning from Daimler is a reality check

By Stephen Wilmot

Trade-deal hopes have given investors a useful opportunity to bail out of European auto stocks. Daimler’s latest profit warning shows why they should seize it.

Europe’s auto sector has had a strong few weeks on the stock market as fears about a global trade war have eased.

Not only have the U.S. and China edged toward a deal, but the White House has also quietly backed away from its threat to slap a 25% tariff on imported cars, which would have been devastating for German brands popular among American consumers.

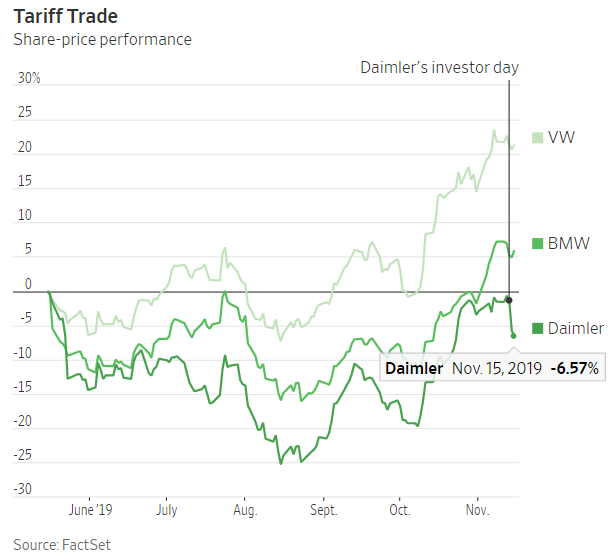

The Euro Stoxx Autos & Parts index is up almost 11% so far this quarter.

Tariffs aside, though, conditions are only getting tougher for Europe’s vehicle industry.

Daimler, which makes Mercedes-Benz DMLRY -0.89%▲ cars and Freightliner trucks, spelled out the problem in sobering investor days in London on Thursday and New York on Friday.

Investors had hoped that a brand new management team led by Chief Executive Ola Källenius,who took the top job from longtime boss Dieter Zetsche in May, would somehow reinvigorate the Daimler investment case after a string of profit warnings—possibly even by splitting the company up.

Instead, Mr. Källenius’s first big step has been to lay out the immense scale of the challenge.

Daimler stock fell 4.5% Thursday and was also down in early trading Friday.

This year has been “relatively difficult,” said Mr. Källenius, but next year will be even worse—and even after that the recovery appears highly risky.

The operating margin of the flagship Mercedes-Benz car division, which accounts for roughly half the company’s revenue, will fall to roughly 4% in 2020 from 5% this year.

Analysts had been expecting something close to 6%.

The company now says the margin only will recover to that level by 2022.

Even these downbeat forecasts seem dependent on punchy assumptions: No recession, sales growth approaching 3% and no tariffs.

If President Trump’s trade talks fall apart and China increases its tariffs on vehicle imports from the U.S. next month, as threatened, the Mercedes-Benz operating margin would barely exceed 3% next year.

Daimler exports sport-utility vehicles to China from its plant in Tuscaloosa, Ala.

There are two big reasons why margins are falling: the need to sell less profitable electric vehicles to meet new European emissions regulations that partially come into force next year and higher depreciation charges.

Daimler has been investing heavily in recent years, but the impact on its earnings has been masked because it has counted an increasing part of the bill as capital rather than current spending.

At some point it has to pay for that approach: Capital must be depreciated, while the proportion of capitalized costs can’t rise indefinitely.

Daimler needs to offset these pressures.

The main lever available is squeezing suppliers to cut material costs, but the company is also reducing staff numbers, particularly in the car division.

In total it said staff costs would be reduced by €1.4 billion ($1.54 billion), which will irk Germany’s powerful unions but equates to less than 1% of the company’s €167 billion in revenue last year.

Daimler is an extreme example, given its history of under-managing costs, but all car makers face the same formidable regulatory conditions in Europe and China.

For now, the U.S. is taking a longer road to electrification, easing the pressure on Detroit, but U.S. car makers are working toward the same ultimate destination.

Seeking refuge in scale, which gives car makers more leverage over suppliers, is one response—hence the merger plan under negotiation between Fiat Chryslerand Peugeot,and the platform-sharing deals between Volkswagenand Ford.

After the recent rush of trade optimism, the Euro Stoxx Autos & Parts index fetches roughly eight times expected earnings—close to an 18-month high. Now is a good time for investors to limit their exposure.

Whatever happens with Mr. Trump’s tariffs, next year’s emissions regulations will cause an almighty pileup.

0 comments:

Publicar un comentario