If Firms Leave China, Will US Tariffs Follow?

By: Phillip Orchard

Stroll down the electronics aisles of any big box store in America, and you’re bound to see an array of products from companies that are moving manufacturing from China to Southeast Asia.

Much of the components in Apple’s AirPods, Google’s next Pixel phone, and Nintendo’s Switch, for example, are now made largely in Vietnam.

Sony has moved operations to Thailand, while Samsung is shifting notebook and smartphone production to Taiwan and Malaysia.

This is, to a large extent, the result of the U.S.-China trade war, which has sent firms scrambling to adjust their supply chains to minimize the effects of existing or scheduled U.S. tariffs.

But firms in China haven’t exactly been stampeding for the exits. Among other sources of hesitation is major uncertainty about where the White House’s trade war might expand to next.

After all, China has never been the sole focus of the United States; Washington kicked off the trade war in spring 2018 with metals tariffs applied almost globally, and it’s been gradually ramping up pressure on dozens of other countries.

Over the past few months, U.S. President Donald Trump has claimed that both the European Union and Vietnam are worse trade abusers than China.

On Oct. 25, the U.S. revoked special trade privileges affecting some $4 billion in exports from Thailand – a move similar to ones it also made this year against India and Turkey (and threatened against Indonesia and Kazakhstan).

Bottom line: Few low-cost manufacturing hubs are safe from U.S. pressure altogether. But trade pressure is hardly the same thing as a trade war, and Southeast Asia will largely be spared.

A Partial Exodus From China

Relatively few firms are abandoning China as a manufacturing base altogether.

Most companies that make things in China do so in part to ensure their ability to sell their products to Chinese consumers, who make up the world’s second-largest consumer market.

The fact that other major consumer markets – Japan, South Korea and Europe, in particular – have politely declined to follow the United States’ lead with tariffs on Chinese exports of their own further diminishes the need for firms to pull up stakes.

Moreover, though Chinese exports to the United States are finally starting to show sharp declines, U.S. consumers continue to eat a large portion of the costs of U.S. tariffs on China.

The reality is that moving operations is expensive, disruptive and time-consuming, so many firms are reluctant to do so – especially since at least some of the U.S. tariffs are likely to be lifted if and when Washington and Beijing eventually reach a trade deal.

Of course, the trade war has made abundantly clear the risks of being too reliant on any one place, along with the fact that many frictionless supply chain models have been optimized to the point of becoming excessively fragile and vulnerable to disruption.

And for firms in high-tech and advanced manufacturing sectors with national security implications, U.S. restrictions on China-made imports are quite likely to remain in place for the long haul.

As a result, we’re seeing an increasing trend of firms considering moving just enough operations out of China to be able to put the uncertainty of the trade war behind them and get on with business.

But even among those for whom relocating is worth the time and expense, there’s still the issue of finding a suitable alternative to China. There are two main problems with Southeast Asia and other low-cost hubs.

First, no single alternative hub boasts China’s combination of advantages.

Despite its rising labor costs and loss of some low-skill manufacturing to frontier markets, China remains uniquely attractive as a well-oiled export machine for goods further up the value chain.

Its infrastructure, near-bottomless pool of well-trained workers, and the abundance of financial incentives available from local governments keen to prevent large-scale job losses have helped offset the rising costs of production.

India, for example, has the bottomless low-cost labor pool, but not the infrastructure, streamlined regulatory schemes or tech sector experience needed to lure away firms en masse – and it’s too far from East Asia’s most important tech clusters to fit seamlessly into the industry’s tightly integrated supply chains, anyway.

Malaysia and, to a lesser extent, Thailand rate highly on infrastructure and tech sector expertise, but not on labor pool depth, and both are a bit too far from other regional hubs to be considered ideal.

Vietnam has the ideal location, the low labor costs and open access to consumers in its fellow Trans-Pacific Partnership members, but its weak infrastructure became quickly oversaturated after the trade war exodus began.

Infrastructure can of course be built, and regulatory and incentive schemes can be adjusted to meet exporters’ needs.

But these are long-term projects.

And there’s little that can be done to offset these countries’ geographic or demographic disadvantages.

Trade Pressure on Southeast Asia, Not a Trade War

The second main problem is the concern that U.S. tariffs might just follow exporters from China to the next low-cost export hub.

The U.S. tariffs on China are indeed starting to hurt Chinese exports.

U.S. imports from China have fallen 12.5 percent so far this year, compared to 2018.

But this has done little to benefit employment in U.S. manufacturing outside of a small number of industries.

On the whole, U.S. exports of goods have declined around 3 percent year on year since the beginning of 2019, and U.S. manufacturing activity has contracted for two consecutive months, according to the Institute for Supply Management. (Some of this is due to the global slowdown more than the trade war.)

Other low-cost manufacturers, meanwhile, have generally benefited from the trade diversion.

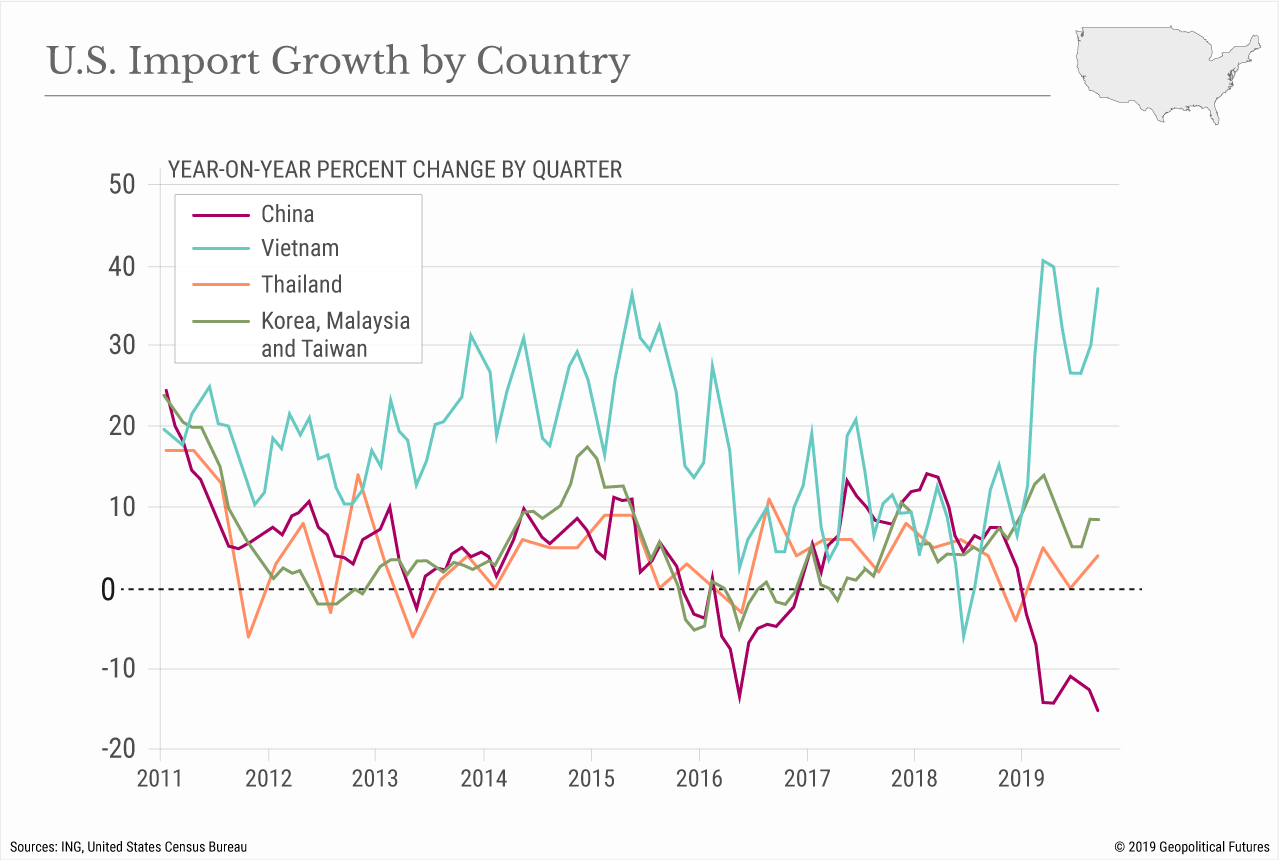

Vietnam, for example, has been the clear winner at this point, with its exports to the U.S. surging some 40 percent year on year.

(click to enlarge)

If the overriding goal of the Trump administration's tariffs is to revive the lost glory of labor-intensive U.S. manufacturing, then it stands to reason that eventually it would have to expand tariffs to other low-cost manufacturers running large trade surpluses with the United States as well. (The U.S. would probably also have to wage war on automation.)

To be sure, some in the Trump administration have certainly advocated for a much sharper turn toward autarky.

But that was always politically unrealistic. And if that were indeed the overriding goal, we probably wouldn’t be seeing the White House prepping the public for a deal with China that will almost certainly relax some tariffs.

And we wouldn’t have seen the Trump administration settle for largely cosmetic changes in its renegotiated trade deals with Mexico, South Korea and Japan.

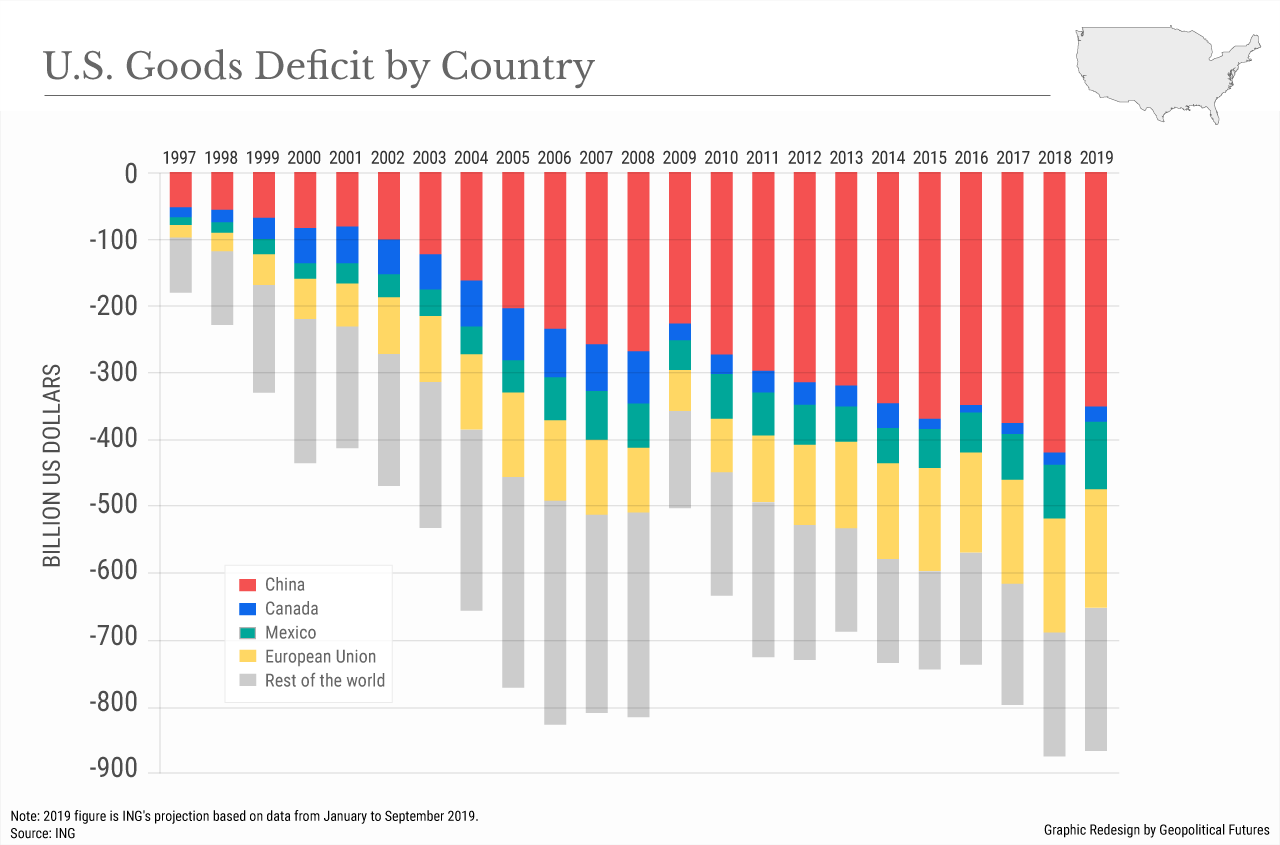

(click to enlarge)

Rather, the two main goals of the tariffs are to pressure China into immense structural reforms and to contain China's accumulation of power more broadly.

We’re doubtful of the ability of tariffs to really do much toward either goal and think that the United States will eventually move away from tariffs as its favorite tool for resetting its trade relationships.

But the belief that China must be pressured to change one way or another and/or that China poses an intolerable threat to U.S. strategic interests is widespread on both sides of the aisle in Washington – far more so than the base of support for tariffs aimed at reshoring low-cost manufacturing jobs.

And expanding the trade war in full force to Southeast Asia and low-cost hubs elsewhere would conflict with both of these larger goals.

This doesn’t mean countries like Thailand, Vietnam and India are immune to U.S. pressure altogether.

The U.S. has long sought to nudge exporters everywhere to comply with global trade rules on issues like currencies and subsidies, whether with stick or carrot.

To maximize its campaign against China, the United States also has strong incentives to crack down on Chinese transshipments through regional hubs.

Perhaps the biggest risk for tech sector firms is that the U.S. expands measures aimed at mitigating supposed Chinese technological threats to U.S. national security to high-tech manufacturing operations elsewhere in the region – particularly Taiwan, countries vulnerable to Chinese intelligence, or countries with governments considered too cozy with Beijing.

Otherwise, U.S. trade measures targeting regional states will be relatively light, aimed at addressing narrow issues that are largely resolvable in negotiations. (The U.S. move against Thailand, for example, affects just 15 percent of Thai exports to the U.S. and was driven ostensibly, at least, by correctable human rights issues in the seafood industry.)

Most important, none of these countries has the capacity to fundamentally threaten the United States’ core interests economically or strategically.

Quite the contrary, in fact.

To establish long-term incentives to persuade China that it’s in its best interest to play by established rules and to undermine its coercive power regionally if it doesn’t, the United States will have greater reason to work with the region, not against it.

0 comments:

Publicar un comentario