Average yields on auto loans are being supported largely by short-term factors that don’t look sustainable over a long-time horizon

By Telis Demos

Early this year, declining used-car prices supported rising yields on auto loans, but prices recently have surged; pre-owned vehicles at a Miami auto dealership. Photo: Alan Diaz/Associated Press

Auto lenders have enjoyed driving on an open road for a while. It is about to get more congested.

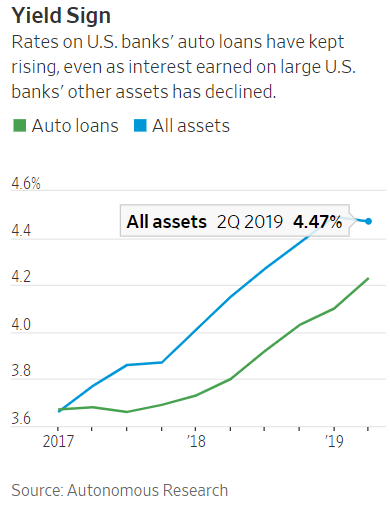

As would be expected amid falling rates, the average yield on the largest U.S. banks’ total asset portfolios declined sequentially for the first time in three years in the second quarter, by 0.02 percentage points, according to figures compiled by Autonomous Research. But average yields on loans to car buyers among the five biggest auto-lending banks actually rose sharply, by 0.13 points, Autonomous shows.

That could make sense if credit risks were surging in auto lending, something many have warned about for years. But at the moment, credit isn’t getting any worse. Delinquencies actually declined slightly in the second quarter, to 4.64%, according to the Federal Reserve. And charge-offs among the biggest auto-lending banks are at a three-year low, Autonomous figures show.

Instead, auto yields are being supported by some short-term factors that look much less sustainable over a longer time horizon.

For one, used car prices had been declining at the beginning of the year. This supported higher yields because a key component of auto lending risk is the expected recovery of a repossessed car in the secondary market. But prices have since surged, with the Manheim Used Vehicle Value index hitting a new all-time high in August. Trade spats only bolster the outlook: If imported cars are slapped with big duties, more people head into the used market, lifting prices.

There has also been less competition of late. Major institutions like JPMorgan Chaseand Wells Fargoboth pulled back from the space when auto delinquencies rose and used-car prices fell in 2016 and 2017.

But as Autonomous’sBrian Foranpoints out, it is very easy to scale up and down in auto lending. A lot of production originates from dealers and is acquired second-hand. Plus there are many nonbank players, making it hard to get a real-time sense of who is in or out. “This is an unusual market, and banks are just a piece of it,” Mr. Foran said.

This week, there were indeed signs of elevated yields drawing lenders back into the market. Wells Fargo on Monday said it was expanding production again. Capital One Chief Financial OfficerR. Scott Blackleysaid on Tuesday about auto loans: “I would say that we are seeing more competition.”

It has been tempting to follow the yield. Ally Financial ,whose primary lending business is auto lending, has been one of the top gainers among large U.S. banks this year, up 55%.

And it remains reasonably priced, trading at 8.3 times forward earnings. That is well below the 11.1 times average for constituents of the KBW Nasdaq Bank index, though only slightly below its own five-year average of 8.7 times, according to FactSet.

However, with a new influx of competition on the way, pure-play lenders like Ally have a more congested road ahead. Investors should leave them on the lot for now.

0 comments:

Publicar un comentario