By Tara Siegel Bernard and Karl Russell

Examine the typical American family’s monthly budget, line by line, and a larger story emerges about how the middle class has evolved.

What it means to be middle class hasn’t changed much — there’s a steady job, the ability to comfortably raise a family if you choose to, a home to call your own, an annual vacation. But what it takes to achieve all that has become more challenging.

The costs of housing, health care and education are consuming ever larger shares of household budgets, and have risen faster than incomes. Today’s middle-class families are working longer, managing new kinds of stress and shouldering greater financial risks than previous generations did. They’re also making different kinds of tradeoffs.

Most people believe that they belong somewhere in the middle class, but its boundaries and markers are subject to interpretation.

Based on income alone, about half of all adults in the United States fall in this category, according to a 2018 report from the Pew Research Center, a nonpartisan research group. It defined being middle class as having an annual household income from about two-thirds to double the national median, which translates to roughly $48,000 to $145,000 for a family of three (in 2018 dollars).

Four families, from Sheboygan, Wis., to San Francisco, gave us a glimpse at their monthly budgets. Their stories help illustrate how a middle-class existence has fundamentally shifted over a generation.

‘Such High Levels of Stress’

For Lauren and Trevor Koch of Sheboygan, making their finances work on one salary was a struggle. Mr. Koch, a chef earning $51,000, often worked 50 hours or more a week. Ms. Koch decided to give up her job as a restaurant server after the couple had the first of their two children. Given the high cost of child care, she felt her time was better spent at home.

Life got trickier when Mr. Koch lost his job as a chef at the end of February. Now he cares for the children in the morning, while Ms. Koch works part time at a shop that sells CBD, or cannabidiol, products. When she gets home at 1 p.m., he leaves for his job as a line cook, where he is paid hourly and works until 11 p.m. Neither of them receives paid time off or health insurance.

“We have such high levels of stress from juggling our schedules,” Ms. Koch said. Collectively, they earn slightly more than before, she said, but it’s unclear if their hours will dwindle during the winter months.

As family incomes have become more volatile, academic experts said, the trend has contributed to greater feelings of financial insecurity. For many people who experience a drop in income, whatever the reason, the declines tend to be greater than in the past, according to an analysis by Jacob Hacker, the director of Yale University’s Institution for Social and Policy Studies.

The share of Americans who experience income loss tends to rise and fall with the economy. But the share of Americans experiencing larger losses has increased.

“The gap between Richie Rich and Joe Citizen is a lot larger than it used to be,” Professor Hacker wrote in “The Great Risk Shift,” “but so too is the gap between Joe Citizen in a good year and Joe Citizen in a bad year.”

That’s just one indicator of the deeper structural problems reshaping the middle class, he said. Employers and government institutions keep shifting responsibility to workers, forcing them to navigate more threats to their financial well-being. Pensions have been largely replaced by 401(k) plans. Comprehensive health coverage has given way to high-deductible plans. Paid family leave is uncommon.

So families make tradeoffs. Even when Mr. Koch had a salaried job with benefits as a chef, he and his wife couldn’t afford to save for retirement. Their biggest expenses were rent, food and debt payments, and they were just scraping by. At $80 a month, their health care premiums seemed reasonable, until they needed a doctor: Both had deductibles of $3,000.

Such a fragile existence is threatened even further when major investments meant to cement a middle-class life — getting a college degree, buying a home — backfire. Mr. and Ms. Koch both have more than $70,000 in loan debt for college educations they never completed, meaning a good chunk of their money is effectively gone every month before they have spent anything at all.

If their finances were stronger, Ms. Koch said, they would seek help handling life’s stresses and complexities. “Therapy is probably the first thing we would add into our lives,” she said.

‘We Are in Survival Mode’

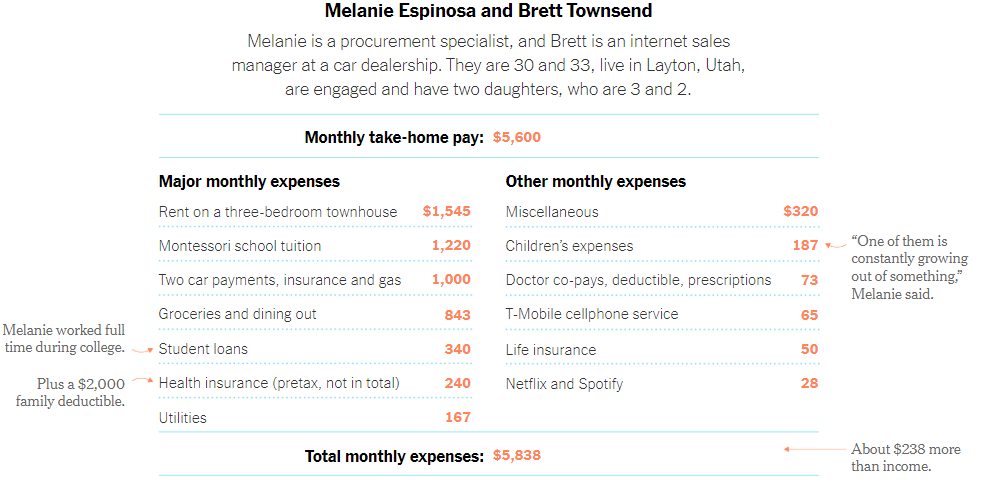

Melanie Espinosa, 30, and her fiancé, Brett Townsend, 33, of Layton, Utah, have mastered a morning routine: She is up at 6:45 getting ready for work. He rouses and dresses their two toddler daughters about 15 minutes later and gets them a snack. They buckle the girls into their carseats by 8 and head to preschool. They’ll have breakfast there.

Ms. Espinosa, a purchasing specialist at a transit technology company, and Mr. Townsend, an internet sales manager at a car dealership, together earn about $90,000 a year. And yet their income never seems to go as far as they need it to.

Ms. Espinosa said they would like to save for a down payment on a home and for the girls’ college educations. But that isn’t possible right now.

“We are in survival mode,” she said. “We can mostly break even.”

Even with two paychecks, middle-class status has become more elusive. The soaring costs of those three big-ticket items — housing, health care and college — have made it more difficult for some people to achieve certain milestones.

The struggle is not unique to the United States. In April, the Organization for Economic Cooperation and Development reported that pressures on the middle class around the world have increased since the 1980s. What sets middle-class Americans apart, the study found, is that they are struggling under several burdens — low income growth, rising costs, declining job security — while those in many other countries face just one or two.

Spending patterns have also shifted drastically over the past century. American households spend significantly more of their budgets on housing and less on items like food than they did in previous decades.

Housing accounted for 23 percent of the average household’s total expenditures in 1901, 27 percent in 1950, and nearly 33 percent in 2018, according to data from the United States Consumer Expenditure Survey. Those squarely in the middle of the income distribution spent slightly more, or 34.5 percent. (The data doesn’t account for homes today being larger and having more amenities.)

“Young families with kids are really getting slammed on all sides,” said Jenny Schuetz, a fellow at the Brookings Institution who studies housing policy. “They are more likely to have some student debt, and child care has gotten more expensive. So if you are trying to pay off student debt, pay for child care and rent, it will be tough to save for a down payment.”

Child care is a substantial expense for Ms. Espinosa and Mr. Townsend — and it just swelled. They were paying about $800 a month, a relative bargain because they relied on someone who watched children in her home. But they had to find a replacement quickly when their caregiver stopped working recently. Two spots at a Montessori school were available, but they’re now paying $1,200 for that — nearly as much as their rent.

The girls are thriving, Ms. Espinosa said, but the extra cost will probably push the prospect of owning a home further into the future.

The couple’s only debt is from Ms. Espinosa’s student loans, now just under $16,000, and car payments on their six- and 11-year-old Hondas.

Ms. Espinosa said she had always thought being middle class meant living a humble life, without having to constantly worry about which bills were coming up.

“We have a good income for where we are,” she added. “But for some reason every single month it seems like, ‘Oh, something came up or we didn’t make enough.’ It’s just a constant battle.”

‘If It Had Not Been for Women’

Until a few weeks ago, Amanda Rodriguez and David Allen together earned about $154,000 annually, which would place them on the upper-income tier in many American cities. But in San Francisco, where they live, it’s considered middle class, according to Pew’s calculations.

The couple welcomed a baby girl in May, meaning their income will have to stretch even further: They will likely spend roughly two-thirds of their take-home pay on child care and rent on their two-bedroom apartment. For now, they’re managing on less money.

Ms. Rodriguez, who has been on maternity leave, had planned to return to her job — managing a program that trained medical providers to help victims of violence — in mid-September. But little more than two weeks before her scheduled return, she learned she no longer had a position to return to — federal funding had been slashed, eliminating the program.

So her leave from the work force has effectively been extended — she plans to look for another job in public health in the coming months.

The shape of the American family is in a steady state of flux, but two-earner households are the norm now. In perhaps one of the biggest shifts of the past 50 years, married mothers entered the work force in ever-greater numbers in a wave that peaked in the 1990s before leveling off and retreating slightly. Women, in general, followed a similar pattern.

But for many families, the addition of women’s earnings has simply helped maintain their position or kept household income from dropping, according to an analysis by Heather Boushey, the president and chief executive officer of the nonprofit Washington Center for Equitable Growth.

From 1979 to 2018, middle-income families’ incomes rose 23.1 percent, adjusted for inflation, according to the study. Professional families’ incomes, by contrast, rose 68.3 percent. Over the same 39 years, the average American woman experienced a 21 percent increase in annual working hours, according to Ms. Boushey’s analysis.

Most of the earnings gains among families in the period Ms. Boushey studied can be traced directly to working women. They accounted for three-quarters of the rise in income among middle-class families in that time. Among professional families, women’s earnings were the most important factor, but men’s incomes rose, too.

“Many families would have seen their income drop precipitously over the past few decades if it had not been for women going to work,” Ms. Boushey said.

Low-income households: those in the bottom third of the income distribution, or earning less than $26,080 annually in 2018 dollars; Professional families have income in the top 20 percent, or roughly $71,913 or higher, with at least one member holding a college degree or higher. Everyone else is middle class.·Source: Heather Boushey, president and chief executive of the Washington Center for Equitable Growth.

And though it’s more common now than it once was in households led by two adults for both to be working, it can introduce new costs and stresses. Ms. Rodriguez wasn’t comfortable with leaving her infant in a big day care, so she and Mr. Allen will most likely pay a little more to share a nanny with another family.

That means they will be forced to set aside significantly less for retirement, eliminate trips to the chiropractor and cut back on weekend jaunts out of town. Saving for a down payment on a home isn’t a priority because they don’t have any aspirations of ever owning in high-cost San Francisco.

“We will rearrange things,” Ms. Rodriguez said. “It’s a very expensive city, and we are actively making a choice to be here.”

‘We Have Been Incredibly Lucky’

“Middle class to me means being able to work and afford the things we need and some of the things you want,” said Mr. Schluckebier, a 38-year-old academic adviser at a university, who recruits students and helps them navigate the curriculum. “And I’d say we are on the upper end of that.”

Families like the Schluckebiers — on the cusp of what could be considered upper middle class or above — have experienced greater income gains than those squarely in the middle. That has allowed their collective net worth to grow far more, even if they feel pinched by rising costs.

“A good proxy for points at which we can be pretty sure people are in a strong financial position is if their income is congealing into wealth,” said Richard Reeves, director of the Future of the Middle Class Initiative at the Brookings Institution and the author of “Dream Hoarders: How the American Upper Middle Class Is Leaving Everyone Else in the Dust.” “It is not what is coming in, but what is staying in.”

There is no magic formula for creating that congealing effect, but achieving it often involves several factors, including a bit of luck and a bit of help.

SHARE OF INCOME: Income after accounting for federal taxes; social insurance benefits like Social Security, Medicare, unemployment insurance; and mean-tested benefits like Medicaid and food stamps. SHARE OF WEALTH: Income groups are measured by usual income, which is designed to capture income without economic fluctuations. Does not count value of Social Security benefits or defined benefit plans; also excludes Forbes 400, so likely underestimates wealth held by top 1 percent.·Source: Brookings Institution (using data from the Congressional Budget Office and the Federal Reserve’s Survey of Consumer Finance)

A few factors helped shape the Schluckebiers’ circumstances. They made deliberate financial decisions that have worked out well: Both kept the cost of college down by working on campus as resident assistants. They also worked full time during graduate school — Mr. Schluckebier was a residence hall director, so they had free housing — and eventually saved $16,000 for a down payment on a house.

Once they were ready to buy, they didn’t reach for a more spacious house in the parts of town where two-car garages are the norm. They chose a modest, 1,500-square-foot ranch, then dedicated an extra $800 a month to paying off the principal on their mortgage while making healthy contributions to their retirement accounts. That may be easier to do in a relatively low-cost locale with healthy job opportunities like Iowa City than in a big city on one of the coasts.

Timing also helped. They were ready to buy a home in 2008, as prices were trending lower. They also have the good fortune of having what Mr. Schluckebier calls “spectacular” retirement and health benefits at work. His employer contributes 10 percent of his salary to his retirement account.

The couple’s student debt, now paid off, was manageable, in part because their parents contributed to their tuition payments.

But they worry about whether they will be able to contribute enough toward their own children’s college expenses, given what college might cost 10 years from now. More broadly, they are concerned about the state of the country, and how other Americans are faring.

“We have been incredibly lucky,” Mr. Schluckebier said, “which is why I don’t necessarily worry about us as much as I worry about the macro picture across the country.”

0 comments:

Publicar un comentario