Inflation Outlook Supports Gold's Long-Term Uptrend

by: Clif Droke

Summary

- Low inflation expectations are why gold's long-term prospects are bullish.

- Recent trade relation improvement is a short-term headwind, though.

- Persistent low inflation will eventually overcome gold's latest obstacle.

- Recent trade relation improvement is a short-term headwind, though.

- Persistent low inflation will eventually overcome gold's latest obstacle.

It’s a commonly held assumption that gold benefits primarily from inflation.

If that were entirely true, then there should be no reason for gold to be struggling against the prospects of increasing inflation now that trade relations between the U.S. and China are being patched up.

The idea that gold loves inflation is only partially true, however.

What gold responds to more than anything else is the fear of the unknown.

As I’ll explains here, strong evidence for a lack of inflation supports gold’s longer-term uptrend in the year to come.

On a short-term basis, however, gold faces a headwind from the recent improvement in the global trade Outlook.

Gold’s popularity is always greatest during periods of political or economic turmoil. That includes periods of runaway inflation, such as the U.S. experienced in the late 1970s.

But when the inflation rate is coming off extremely low levels and only gradually increases, this isn’t a reason for investors to fear the economic consequences.

To the contrary, a healthy dose of inflation following a period of low inflation (or deflation) would be quite beneficial for the economy and would also be a reason for investors to sell gold and rotate into assets that would benefit from an improved economic growth outlook.

Low inflation rates, by contrast, imply low levels of economic growth. When the economy fails to realize its long-term growth potential, investors get nervous and accordingly start looking around for safe places to hedge their investments.

Gold is naturally one of the first assets they turn to in their quest for safety.

Indeed, gold’s bull market since last year is at least partially predicated on the market’s worries over sub-par inflation rates.

There has been some speculation among financial commentators, however, that the U.S. and the developed world might finally be heading out of the prolonged period of low inflation in 2020.

Yet there are no signs to date that inflation is anywhere on the horizon.

This is one reason for believing that gold’s longer-term bull market is still intact, even if the yellow metal is struggling to re-establish its forward momentum in the immediate term.

Virtually all the latest major economic reports confirm the near-absence of inflation. Last week it was announced that U.S. consumer prices were unchanged for September as inflation was acknowledged to be in “retreat.”

According to the Labor Department, the flat consumer price index for September recorded its weakest reading since January.

Worries about slowing global growth and continued chaos over Britain’s planned exit of the European Union have contributed to the decline in business investment spending and lower commodity prices.

Not only do the economic numbers testify to the lack of threat posed by inflation, but consumer sentiment reflects continued fears that low inflation is still a problem.

The latest New York Fed survey, for instance, revealed that the inflation outlook for U.S. consumers was muted in September and fell to its lowest level on record over a 3-year timeframe since the bank began its monthly consumer expectations survey in 2013.

This should be regarded as good news for long-term holders of gold or gold-related assets.

On a short-term basis, however, investors aren’t overly worried that the inflation rate will continue to decline.

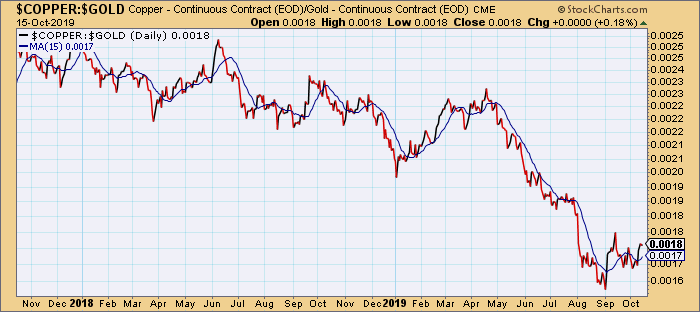

One way to measure the extent to which inflation prevails on a short-to-intermediate-term basis is to compare the gold and copper prices from a relative strength perspective.

Not only does the copper/gold ratio be used to show where long-term Treasury yields should ideally be (based on current inflation rates), but the gold/copper relationship is useful for gauging the safe-haven demand for gold as well.

When the price of copper is weak relative to gold for a period of several weeks-to-months, it implies that investors have serious concerns about the rate of global growth.

Historically, copper is weak versus gold, investors turn to gold and other safety-oriented assets (namely Treasuries) as an insurance policy against a slowing economy.

Shown here is a ratio comparison of the gold versus the copper price in the last two years.

This graph underscores the tendency for rallies in the gold/copper ratio to precede declines in the gold price.

The reason for this is that relative strength in copper suggests that investors’ confidence in the global outlook is temporarily on the rise after the latest improvements in U.S.-Sino trade relations.

When investors are feeling more assurance about the economic growth outlook, they tend to move away from safe havens like gold and turn to risk assets like equities.

This partly explains why the gold price has remained stuck in a trading range since peaking in September.

Source: StockCharts

Source: StockCharts

When the copper/gold ratio is trending lower, however, it implies investors are definitely concerned about slowing global growth.

This was the case in late 2018 and also during the May-August period this year.

The downward trend in the gold/copper ratio shown above illustrates these two periods of worry.

Based on the copper/gold relationship described here, it should come as no surprise that gold’s best performance this year so far was during this period when investors were deeply worried about the U.S.-China trade war and its potential impact on the global economy.

Lately, however, investors have received assurances from the governments of the U.S. and China that they are collectively working toward an agreement which would mitigate the impact of trade tariffs on both sides.

Currently, the copper/gold ratio is above its 15-day moving average and is also above its year-to-date low.

This reflects the short-term headwinds standing in the way of higher gold prices, namely increased investor confidence in the short-term outlook.

Indeed, the bounce in this ratio in September was enough to scare off new gold buyers and also encouraged traders to book some profits in existing long positions in the yellow metal.

But the copper/gold ratio hasn’t reversed its long-term downward trend and this implies that the inflation outlook is still muted. It further suggests that the long-pull bull market for gold which began last year is still very much intact.

On a short-term basis, however, as long as the gold/copper ratio remains above its 15-day moving average, gold’s immediate-term (1-4 week) trend will remain unsettled and new highs in the gold price will have to wait.

What’s more, if the copper price starts to rally on perceptions that China’s industrial outlook is strengthening then we may even see some downward pressure on the gold price.

Yet there are still plenty of geopolitical and global economic uncertainties to keep

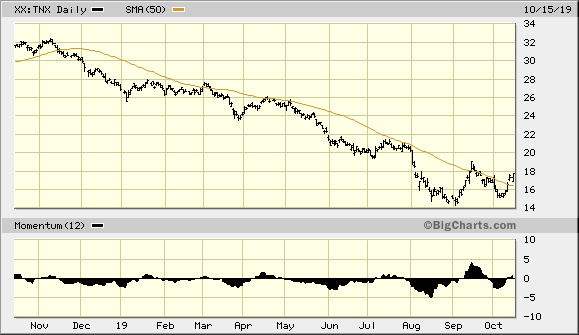

Meanwhile, the copper/gold ratio is current at 0.0018, which is telling us that the U.S. 10-Year Treasury Yield Index (TNX) should be at around 1.80%.

Currently, the 10-year yield is at just under 1.80%, almost exactly where it should ideally be according to the ratio.

The recent rally in TNX represents a an improvement from the last several months when yields were plummeting to unnaturally low levels, due largely to the panic over a global slowdown.

Those fears have been temporarily suspended thanks to the latest developments on the global trade front.

But by no means should investors assume that trade-related worries are a thing of the past.

Accordingly, long-term gold investors are justified in maintaining investment positions in the metal.

Source: BigCharts

Source: BigCharts

However, the higher low that was established in the copper/gold ratio since September is enough to warn investors to steer clear from initiating new long positions in gold for now.

Gold will likely continue to struggle against the efforts of the major industrial nations to lower or eliminate tariffs.

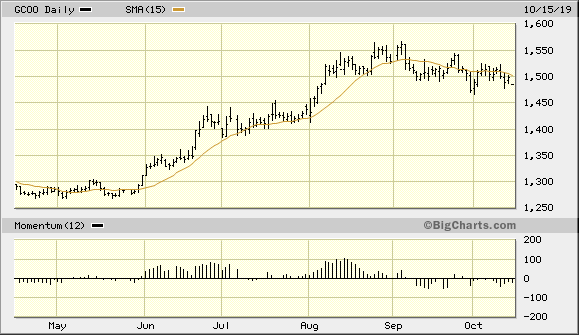

Moreover, until the gold price closes at least two days higher above its 15-day moving average (below), gold will remain vulnerable to any positive news developments on the trade front.

Source: BigCharts

Source: BigCharts

In conclusion, the bull market for gold which began last summer is still being supported by geopolitical concerns and global growth worries.

What's more, an outlook that points to continued low inflation in the coming years is supportive of bullion prices.

On a near-term basis, however, investors should exercise caution and wait until the next technical breakout signal is confirmed in the gold price before adding to existing long positions.

On a strategic note, I’m waiting for both the gold price and the gold mining stocks to confirm a breakout before initiating a new trading position in the VanEck Vectors Gold Miners ETF (GDX), my preferred trading vehicle for the gold mining stocks.

I’m currently in a cash position in my short-term trading portfolio.

0 comments:

Publicar un comentario