by: Victor Dergunov

Summary

- The S&P 500 is approaching new all-time highs, while the economic atmosphere is extremely murky right now.

- The S&P 500 is approaching new all-time highs, while the economic atmosphere is extremely murky right now.

- The Fed may not be as accommodative as many market participants perceive going forward.

- Many key forward-looking economic readings are worsening.

- There are numerous red flags that suggest a recession in the U.S. is approaching.

Fed or no Fed, deal or no deal, a recession in the U.S. may occur within the next 6-12 months.

Source: CNBC.com

Source: CNBC.comThe Recession Approaches: Fed or No Fed, Deal or No Deal

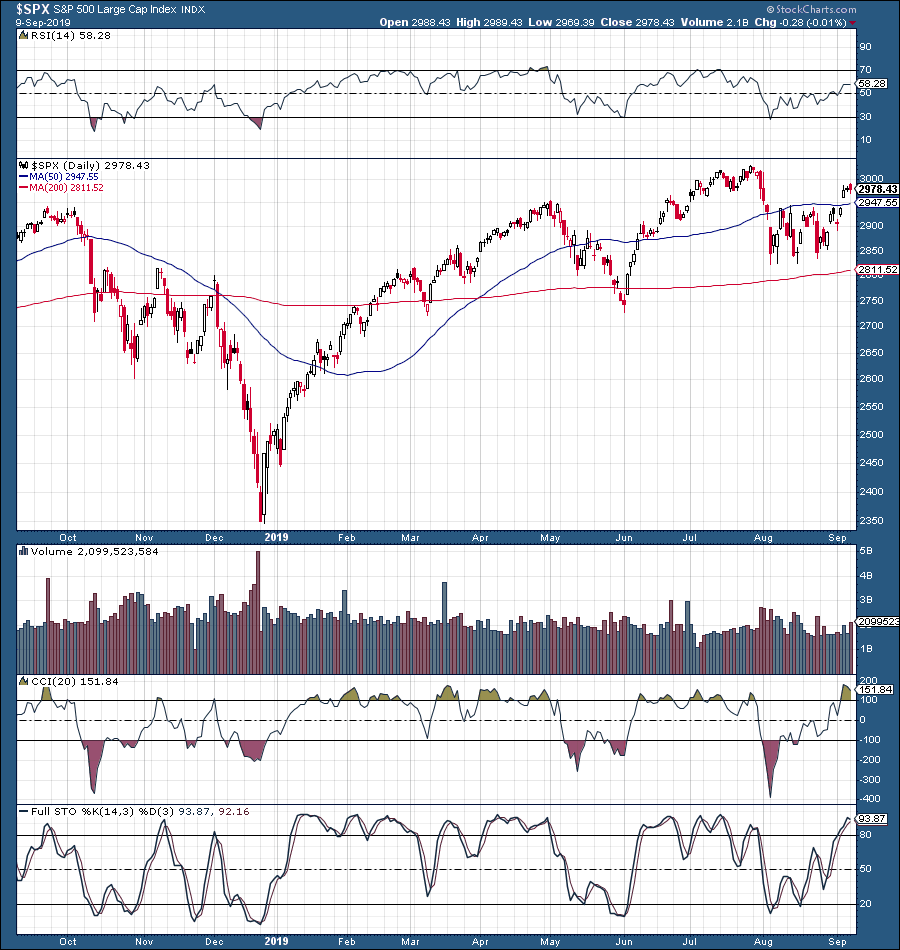

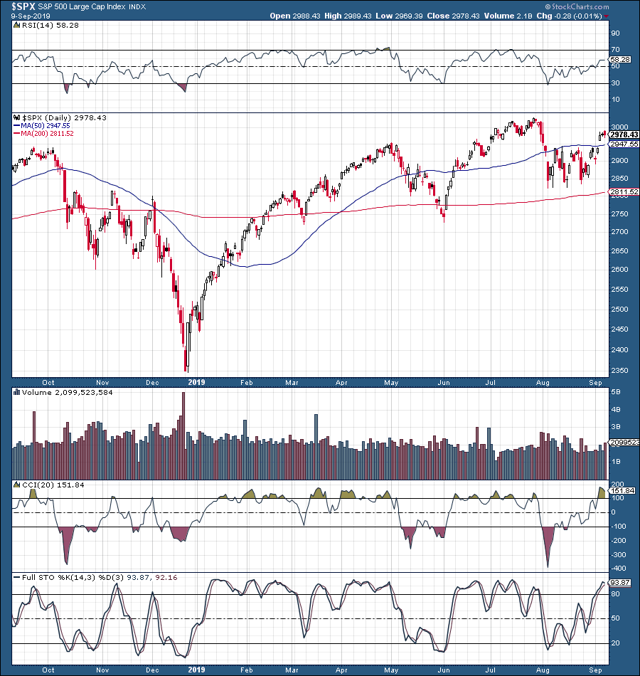

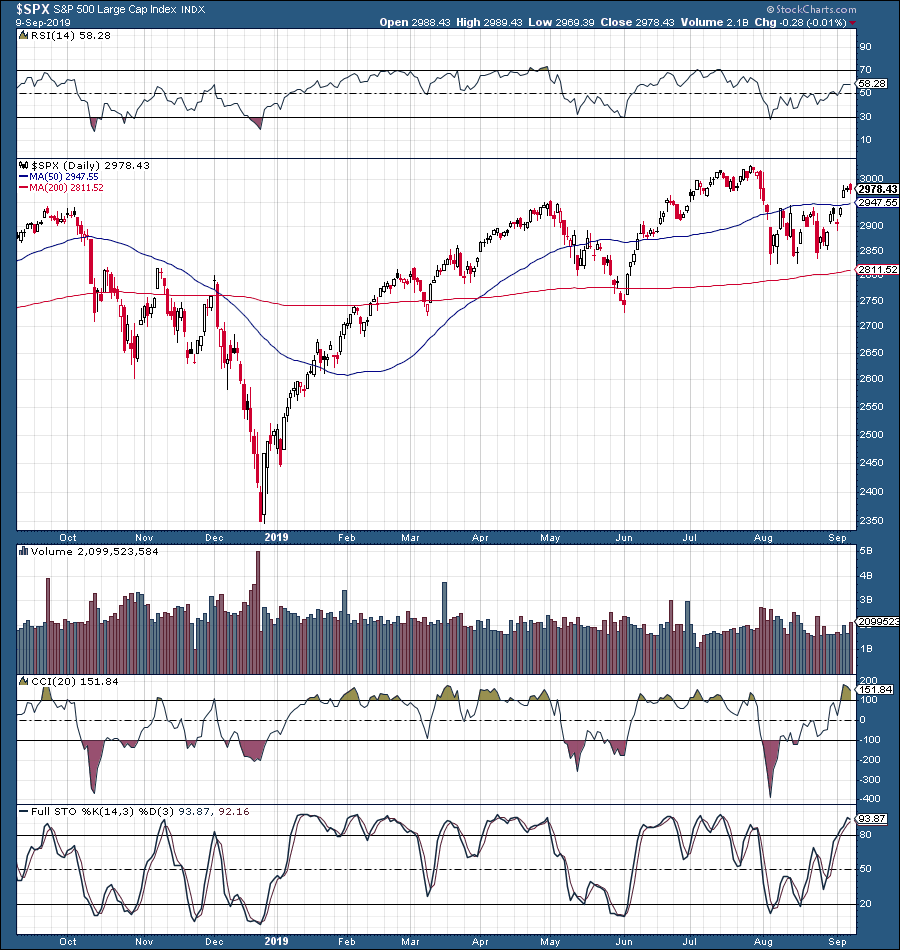

The S&P 500 (SP500)/SPX and U.S. stocks in general are at a crucial inflection point once again.

Despite a great deal of uncertainty surrounding markets today, the S&P 500 is approaching new all-time highs once again.

Image Source: StockCharts.com

Image Source: StockCharts.com

However, despite the rise in equity prices there are still a lot of unknowns. Most notably, it's not clear just how accommodative the Fed will be with regard to supporting markets, and there's still plenty of uncertainty regarding the U.S./China trade deal.

Moreover, clear red flags are continuing to materialize surrounding the overall health and growth prospects of the U.S. economy. Some of the recent economic data is coming in much worse than expected and is highly suggestive of a potential substantial slowdown in the U.S.

Sector and individual stock forward P/E ratios appear too optimistic in many sectors.

Furthermore, we continue to see relatively bearish sector rotation and inverting yields, which are typically precursors to a recession.

Based on these factors and other economic elements, this is likely a very good time to be very cautious. I also believe that this is a time to actively manage and rebalance portfolios, reduce positions in riskier assets, raise cash positions, and move capital into investment vehicles that are likely to benefit from the upcoming economic environment.

Is the Market Expecting Too Much from The Fed?

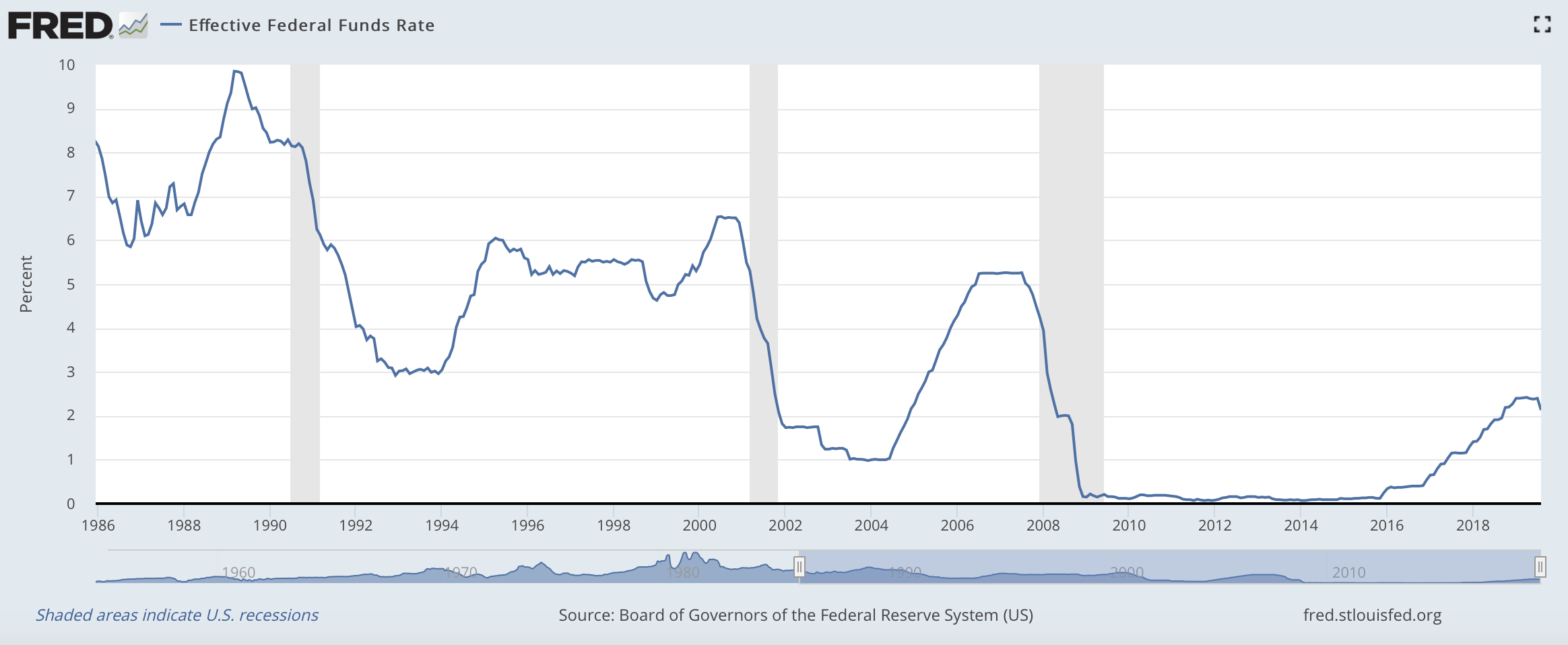

Let’s face it, the Fed plays a dominant role in the direction of the SPX, stocks in general, bond rates, gold, silver, as well as many other assets and trading instruments. Late last year the S&P 500 had a correction of roughly 20% primarily because the Fed was on a tightening path and the economy began to show clear signs of a slowdown. In other words, the U.S. economy was no longer able to sustain growth under “normalizing” interest rate conditions.

.

Image Source: St Louis Fed

We can clearly see that in every subsequent economic cycle the Fed needs to bring rates down lower and hold them lower for longer for the economy to expand. Moreover, in each following cycle the Fed can only “normalize” rates lower and lower before the economy begins to stall. This is due to the enormous amount of debt in the system that simply becomes unsustainable to service when rates rise past a certain point.

You can read about “America’s Impending Debt Crisis” in much more deal in my article here.

Moreover, the Fed funds rate chart shows us a clear correlation between the end of an interest rate hike cycle and the start of a new recession. We can see the funds rate top out in 1989, prior to the 90s recession, a top in 2000, before the 2001 recession, a top in 2007, before the 2008 recession, and we are seeing a top now, probably before a recession that may occur in 2020.

I also want to mention that the Fed has been behind the curve on monetary policy before, and I would not be surprised if the Fed is behind the curve already this time around as well.

After all, who can forget this gem of a quote from the then Fed Chair Ben Bernanke in July of 2007?

July 2007

BERNANKE: The pace of home sales seems likely to remain sluggish for a time, partly as a result of some tightening in lending standards, and the recent increase in mortgage interest rates. Sales should ultimately be supported by growth in income and employment, as well as by mortgage rates that, despite the recent increase, remain fairly low relative to historical norms. However, even if demand stabilizes as we expect, the pace of construction will probably fall somewhat further, as builders work down the stocks of unsold new homes. Thus, declines in residential construction will likely continue to weigh on economic growth in coming quarters, although the magnitude of the drag on growth should diminish over time. The global economy continues to be strong, supported by solid economic growth abroad. U.S. exports should expand further in coming quarters. Overall, the U.S. economy seems likely to expand at a moderate pace over the second half of 2007, with growth then strengthening a bit in 2008 to a rate close to the economy's underlying trend.

Source: Mises.org

Now, I am not saying that we are about to have another housing melt-down, or a 50% stock market crash in the next year, but I can’t help but wonder if the Fed is behind the curve once again.

The Fed is Not About to Bring Out the “Bazooka”

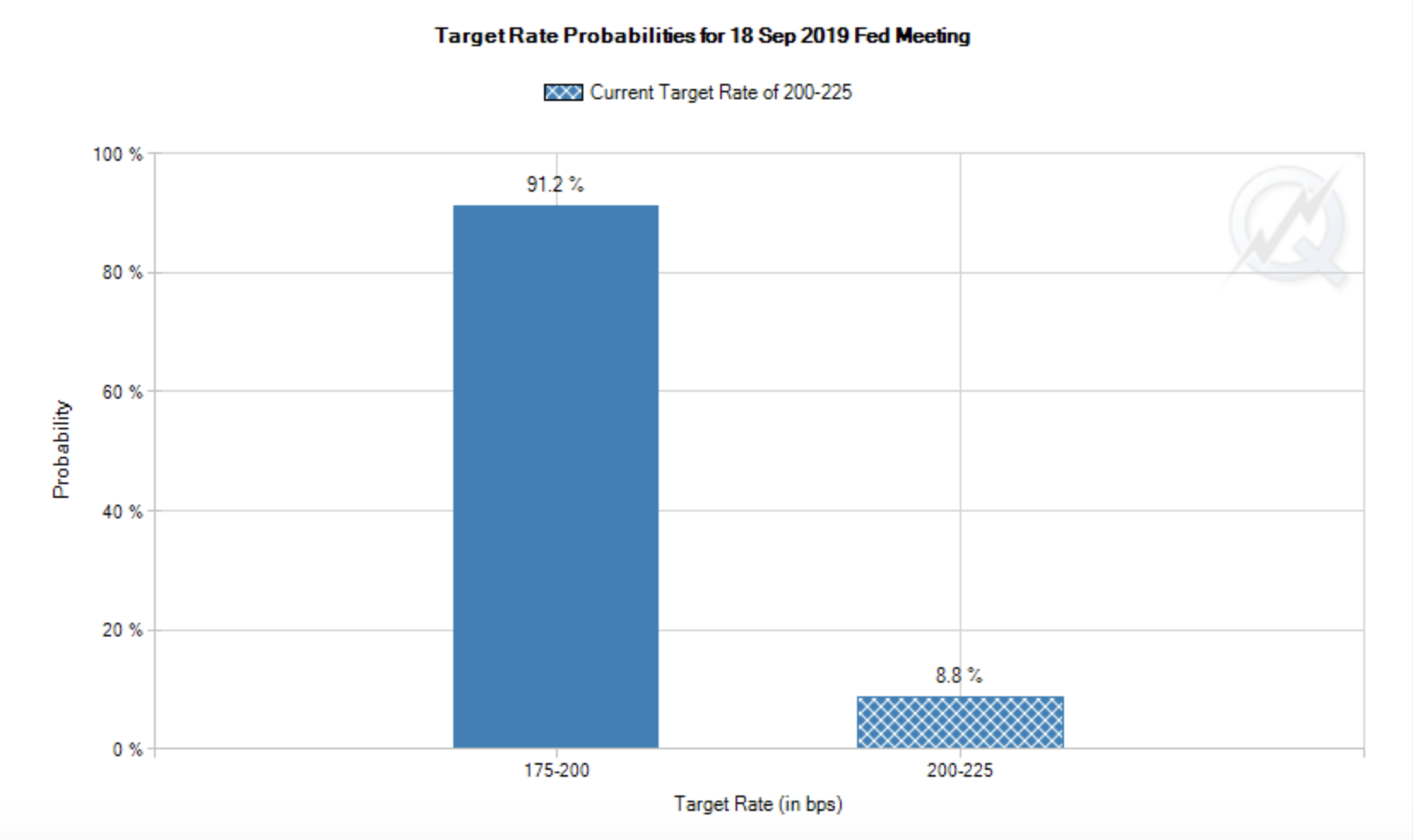

Right now, market expectations are that the Fed is going to lower rates by another 25 basis points on Sept. 18 (91% probability). Will this be enough to keep the economy from contracting further? I have my doubts. Moreover, there's about a 9% chance that the Fed will keep rates as they are today. This would likely be disastrous for equity markets in the short term.

Source: CMEGroup.com

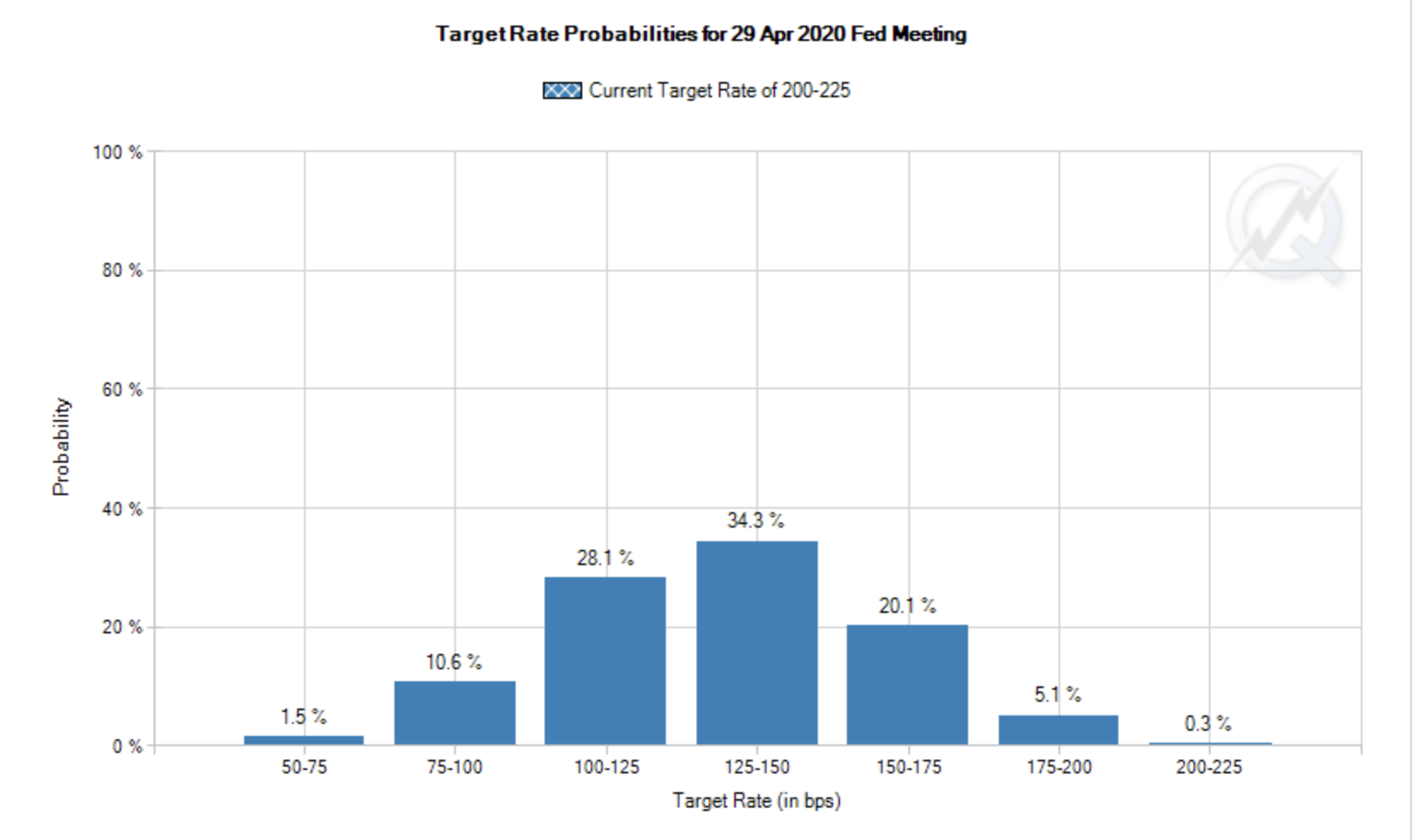

Interestingly, for the most part, the market expects that the funds rate will be between 1-1.75% around six months from now. This is essentially only 25 to 125 basis points lower than where we are today. Will this be enough to revive the U.S. economy? I'm not so sure, as I believe QE is needed to keep this bull market going to prevent the U.S. from falling into a recession.

However, I do not believe that plans for QE will be announced on Sept. 18, which may impact equity prices negatively, in my view.

Some of you might be saying “but the economy appears relatively strong, and the Fed may not need to bring rates down to zero and introduce more QE any time soon.” Well, let’s look at some recent economic indicators and try to put them into context with historical standards.

Red Flags in Recent Economic Data

Concerning the U.S., we saw manufacturing PMI dip below 50, to 49.9 in August. This reading came in worse that the expected 50.5, and lower than July’s 50.4 figure. ISM manufacturing PMI came in at 49.1, vs. the expected 51.1 and prior month’s 51.2 reading. Construction PMI came in at just 45, worse than the expected 45.9 figure. Also, core durable goods orders declined by 0.4% rather than the expected 0.1% rise. These indicators show that the manufacturing base in the U.S. is now officially in contraction mode and the trend is likely to continue.

Perhaps even more troubling, services PMI came in at just 50.9 for August, much worse than the expected 52.9 reading and last month’s 53 figure. This suggests that the services sector in the U.S. is likely about to enter into contraction mode as well.

Other leading indicators like new homes sales came in at just 635K for July, lower than the anticipated 649K figure and much worse than June’s 728K reading. Month-over-month new home sales fell off a cliff in July, down by 12.8%, rather than the expected 0.2% drop. Pending home sales MoM declined by 2.5%, rather than an expected rise of 0.1%.

Now here's where things really start to look troubling - consumer data. Michigan consumer expectations came in at just 79.9 in August, vs. the expected 82.3 figure, and much lower than the prior month’s 82.3 reading. Michigan consumer sentiment fell to just 89.8, vs. the expected and prior month’s 92.1 readings. By the way, this is the lowest reading since 2016. Also, this is not a one month phenomenon, this appears to be a trend now, as the prior month’s consumer sentiment that came in at 92.1 was expected to be 97.2.

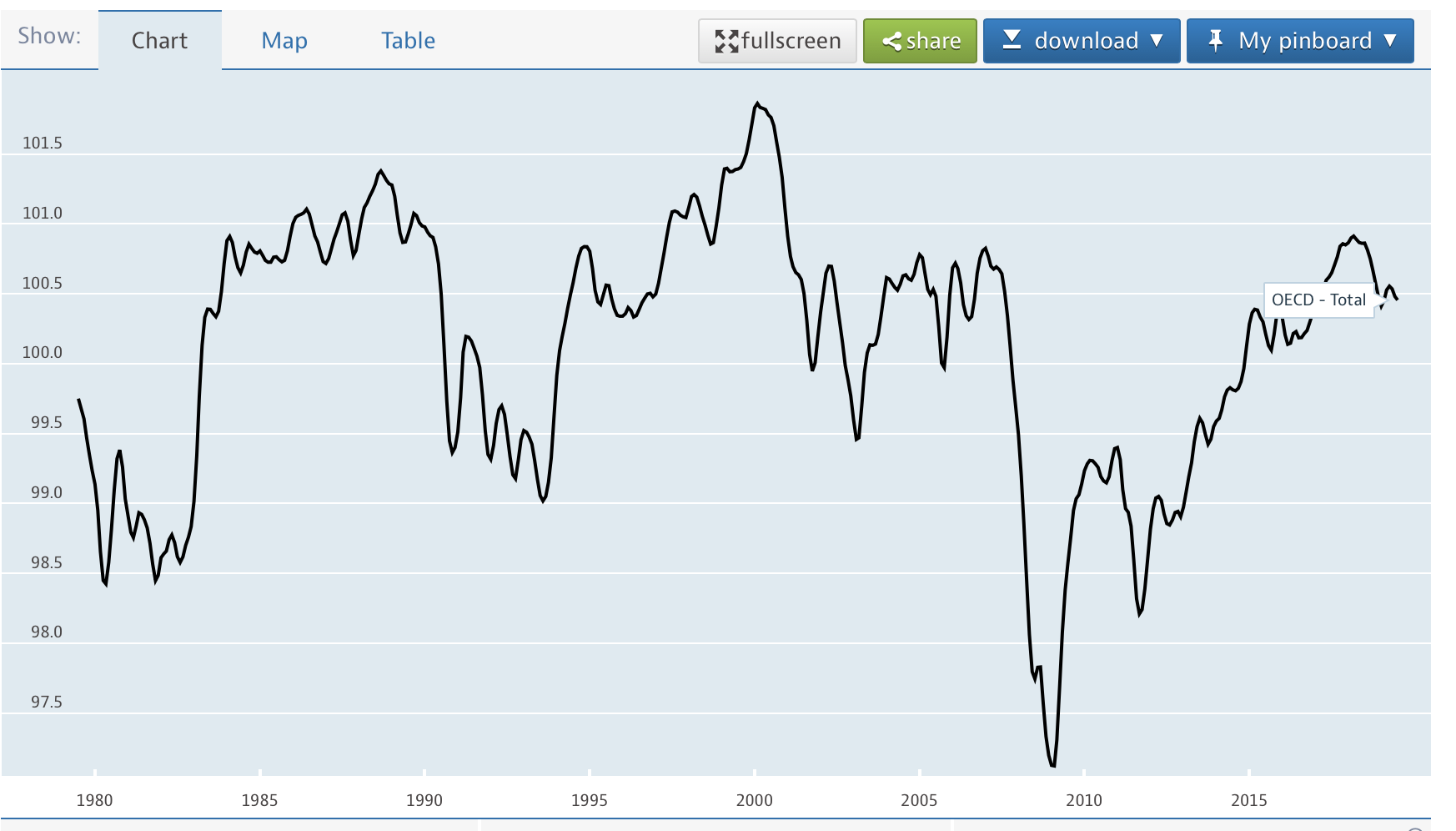

A similar phenomenon can be seen with the consumer confidence index CCI that's typically seen as a precursor to recessions. In early 2018 we saw the CCI top out at around 101, and the index recently dipped below 100.5. Additionally, we see what appears to be a head and shoulders pattern developing in the index’s chart.

Image Source: OECD.com

Perhaps more importantly, we can see that just about every major top in the CCI preceded a recession. We see a top in the late 80s, prior to the 1990 recession, we see a top around 2000, prior to the 2001 recession, then another top in 2007, prior to the 2008 recession, and we see what appears to be a top in 2018, possibly prior to the upcoming 2020 recession.

The consumer may be topping out here, and higher prices on goods manufactured in China due to trade tariffs, higher inflation, enormous debt loads, and other detrimental factors are likely to continue to put additional pressure on the U.S. consumer. As the U.S. economy/GDP is roughly 70% consumer based, a decline in consumer sentiment, confidence, and ultimately spending could push the U.S. economy into a recession relatively soon (6-12 months), from now.

Consumer debt in the U.S., (excluding mortgages) is now at an all-time high, over $4 trillion, which appears to be a ticking time bomb. Moreover, while lower interest rates proposed by the Fed may “kick the can down the road” the explosion at the end of this road may be a lot worse than many market participants anticipate, and there may not be that much road ahead.

Let’s Talk About Employment for a Minute

There has been much debate about the recent non-farm payrolls report. Some say that it's not so bad, some say the economy and the employment portion of the economy are doing just fine.

However, the bottom line is that only 130,000 new jobs were created in August vs. an expected 150,000. That’s more than a 13% miss. By the way, did you know that this year’s monthly job gains are at 158,000, sharply down from last year’s 223K figure?

Also, I want to draw your attention to two factors. One is that a lot of the jobs “created” were part time, or secondary jobs, and that 34K of the 130K jobs that were created were government jobs.

Therefore, the private sector created only 96K jobs, the lowest number since February. Also, who's going to pay for all these new government jobs? Yes, you guessed it, the U.S. taxpayer, the consumer. To put it lightly, the jobs trend is not looking nearly as good as it's being advertised on TV.

I also want to draw your attention to the “multi-decade” low unemployment rate. Firstly, the way unemployment data is calculated now is not like it was calculated in the 1950s, 60s and decades ago.

The real unemployment rate is significantly higher than the advertised 3.7%. The U-6 as it is referred to is the unemployment rate that counts people who haven’t looked for work over the past four weeks and other discouraged “workers” was at roughly 7% in July.

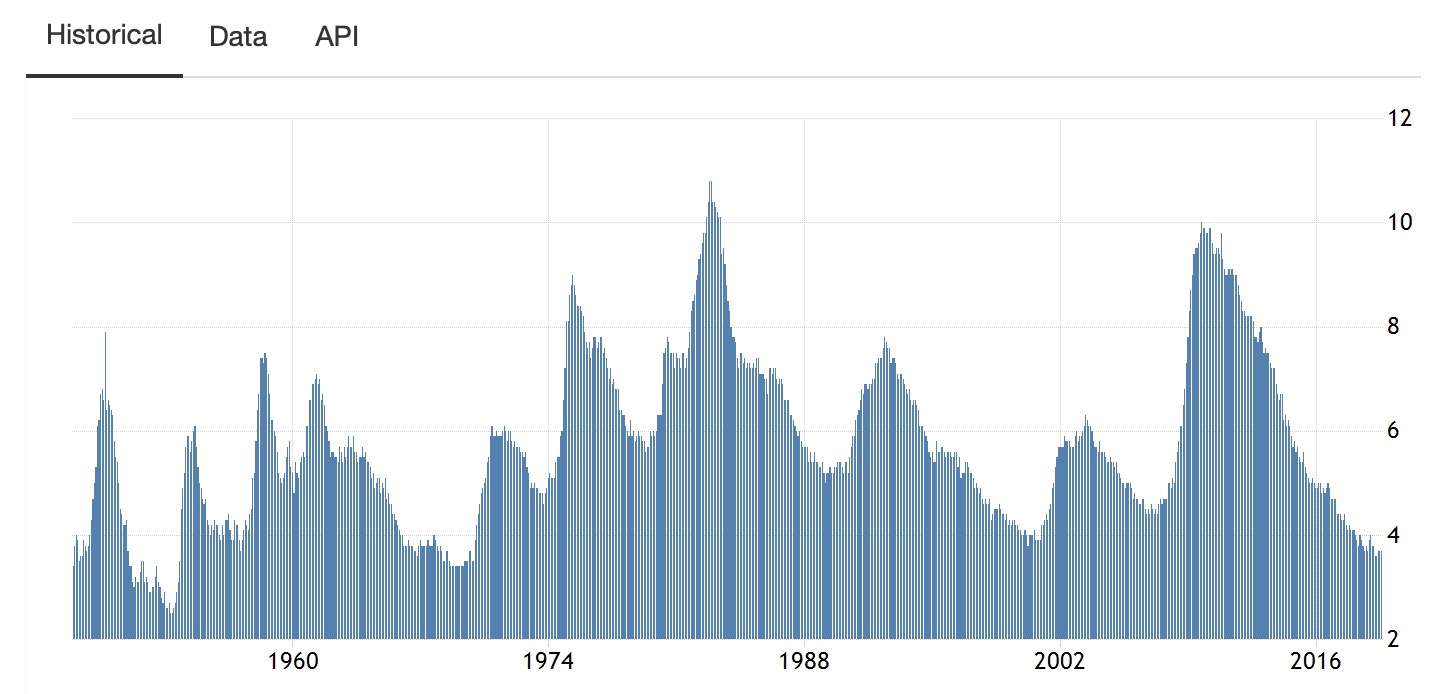

But let’s get back to the “official” 3.7% unemployment rate and see how it correlates with prior recessions. It seems that there's an irrefutable correlation with “rock bottom” unemployment rates occurring directly prior to recessions in the U.S.

Let’s look at some charts:

Source: TradingEconomics.com

Source: TradingEconomics.com

Once again, if we look at recent history, we see that the unemployment rate bottomed in the late 80s, prior to the 1990 recession, then again it bottomed around 2000, prior to the 2001 recession, then again around 2007, prior to the 2008 recession, and it appears to be bottoming right now, which will probably lead to a recession sometime in 2020.

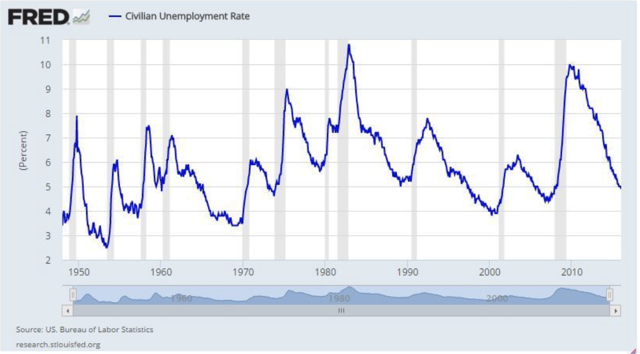

This trend is quite solid and goes back further than the 1980s - just look at this chart here:

Source: Fred.com

Yes, every time the unemployment rate bottomed going back prior to the 1950s a recession followed.

This chart is a bit delayed so the current rate is around where it was in the late 1960s, prior to the recession of the early 1970s.

So, is the Fed Politicized or Not?

I found it almost bizarre what the former New York Fed President Bill Dudley had to say several weeks ago. Dudley essentially urged his former colleagues at the Fed not to “help” President Trump resolve the trade dispute with China. Moreover, Dudley even went as far as to suggest that the Fed try to influence the 2020 election by not cutting rates any further, never mind talk of any QE. Such “Fed policy” would likely help trigger a bear market in equities coupled with a recession in the U.S. just in time for the 2020 Presidential election.

Whether Jerome Powell and other leading members of the Fed knew about the statement ahead of time, or were somehow connected to it remains a mystery. However, Dudley’s statements leave little doubt in my mind that the Fed is as apolitical as it claims to be.

After all, it's not a secret that President Trump has been rather critical of his Fed Chair appointee, and likely wishes he was back in his apprentice chair when it comes to the matter. President Trump can fire just about anyone he pleases in his administration, but he cannot fire the Fed Chair (as the Fed is an independent agency), at least not without due cause, which would likely be very difficult to prove, if not impossible.

Therefore, the market may be too optimistic about what the Fed is prepared to do in the future to support equity markets, and “engineered recession” in 2020 is not out of the question, in my view.

Other Red Flags To Pay Attention To

Bearish Sector Rotation

We continue to see mostly bearish sector rotation - investors piling into “defensive sectors” like utilities, real estate, consumer staples, and some healthcare. For instance, utilities are up by around 18% over the past year and are trading near all-time highs today.

Source: CNBC.com

The problem here is that so much capital has been rotated into this sector is that utilities are now trading at 25.25 times this year’s earnings estimates, which is about double at what this low growth sector typically trades at under “normal market conditions.”

A similar phenomenon can be witnessed in real estate, as this defensive sector is up by about 19% over the past year. This sector also is dramatically overbought as it's trading at 31.27 times last year’s GAAP earnings.

Consumer Staples are up by around 12% over the past year, and are trading at a remarkably high 30.28 times this year’s earnings estimates.

Now let’s look at some more economically sensitive cyclical sectors:

Energy is down by about 18.5% over the past year.

However, it’s trading at around 12.6 times this year’s earnings estimates.

The problem here is that if the global economy continues to slow, oil will likely go lower and so would energy shares.

Nevertheless, for the time being, I believe this sector is deeply oversold and some good companies can have substantial short-term rebounds from current levels.

Financials, another cyclical sector is down slightly for the year, but is trading at just 11 times this year’s earnings estimates. This segment looks relatively attractive compared to most others. However, once you factor in lower interest rates, and the potential for future loan write-offs, this segment too can become a lot “cheaper.”

Healthcare, a relatively defensive segment, is essentially flat for the year, there are some cheap quality names we own in this segment.

Industrials also are essentially flat for the year, but at almost 26 times this year’s earnings estimates seem quite expensive right now.

Materials are down by roughly 4% over the past year and are trading at around 21.5 this year’s earnings estimates. This is not cheap, and this being a very cyclical sector, makes me want to stay away from most names in this segment.

Technology is up by about 8% over the past year, but with the trade war, no earnings growth and trading at 27.5 times this year’s estimates also looks relatively unattractive here.

Consumer discretionary sector is up slightly over the past year, but is trading at nearly 26 times this year’s earnings estimates. This appears expensive considering the “trouble” the U.S. consumer may bump into in the near future.

I also want to draw your attention to the fact that per last year’s GAAP earnings the consumer discretionary segment is trading at a P/E ratio of 25.66. This is lower than the 25.74 this year’s earnings estimate. So, earnings are essentially contracting this year relative to last year’s.

We can see this same phenomenon occurring in other sectors like consumer staples (2018 actual P/E 26.86, this year’s estimate 30.28), in industrials, and in materials. Other sectors are expected to show very little or essentially no earnings growth relative to last year.

The Takeaway

Defensive sectors are clearly outperforming, but are trading at high P/E ratios and are expected to show contractions in earnings or very little growth this year.

Most cyclical sectors are trading at relatively high P/E ratios and are expected to show contractions or very little earnings growth this year.

The only two relatively cheap sectors, energy and financials appear somewhat attractive but if the global slowdown continues, and/or rates continue to decline and loan defaults rise stocks in these sectors should decline as well.

Furthermore, if we look at overall corporate profits this year, Q1 2019 corporate profits came in at $1.79 trillion , a 2.87% decline from last year. While 2019 Q2 profits rose slightly over last year’s Q2 profits, if we combine both quarters, corporate America delivered roughly $3.67 trillion in profits in H1 2018, vs roughly $3.67 in H1 2019, essentially showing no growth in corporate profits thus far year-over-year.

This suggests that corporate profit growth in the U.S. may be topping, and further trade tensions, lower consumer confidence/sentiment, and spending, as well as a continued economic slowdown around the globe may lead the U.S. to a corporate recession relatively soon.

Small Cap Underperformance

Typically, in a healthy economic environment small-cap stocks (Russell 2000) are supposed to lead the market. The opposite is happening right now. In fact, while the SPX is up by about 3.4% over the last year, the Russell 2000 average is down by around 12%.

SPX 1-Year Chart

This implies that market participants have little faith in the growth of the U.S. economy as most small-cap stocks derive most of their revenues and income from the U.S.’s domestic market.

Data by YCharts

Data by YCharts

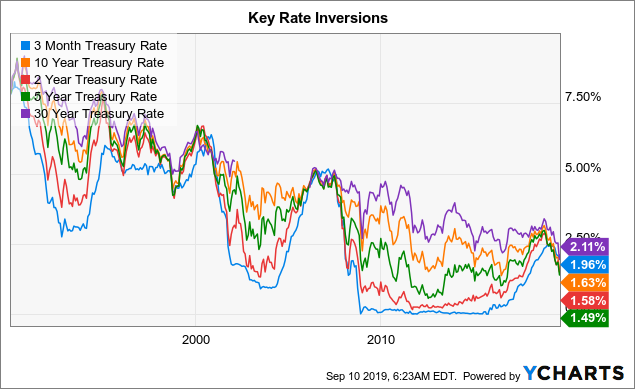

Rate Inversion: A Clear Red Flag

Inverting yields, another typical precursor to a recession, has been sending out troubling signals for a while now. Despite the recent rebound in longer-term Treasuries, we see that the three-month is currently yielding 1.965%, higher than the 1-year, 2-year, 5-year, and even 10-year Treasury. We also, see the 1 and 2-year yielding more than the five-year and the one-year is yielding more than the 10-year. In other words, rates are all over the place, not where they should be in a healthy economic environment.

This shows us that demand for longer term rates is increasing, as market participants expect the Fed will lower rates going forward, possibly down to zero, and quite possibly go negative, like in Europe and in Japan.

Interestingly, if we look at a chart of key rates, we see that inversions typically occur right before recessions and bear markets in equities take place. Once again, we can see rates invert prior to the 1990 bear market, the 2000 meltdown, the crash of 2008, and we are seeing a similar phenomenon transpire right now.

Data by YCharts

China Trade Deal is Far from Certain

President Trump recently acknowledged that "China Policies May Mean Economic Pain" for the U.S.

Furthermore, President Trump essentially capitulated when he moved the deadline on Chinese tariffs.

He feels the pressure from a slowing economy and made a strategic move to delay the tariff deadline to Dec. 15.

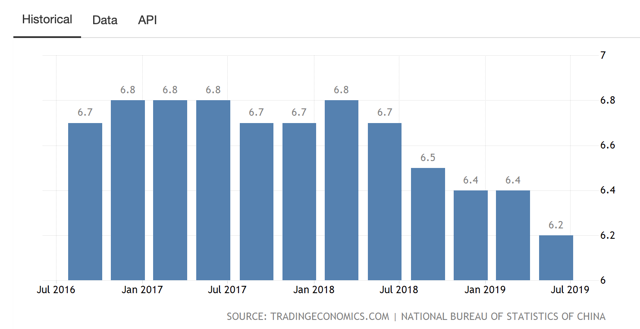

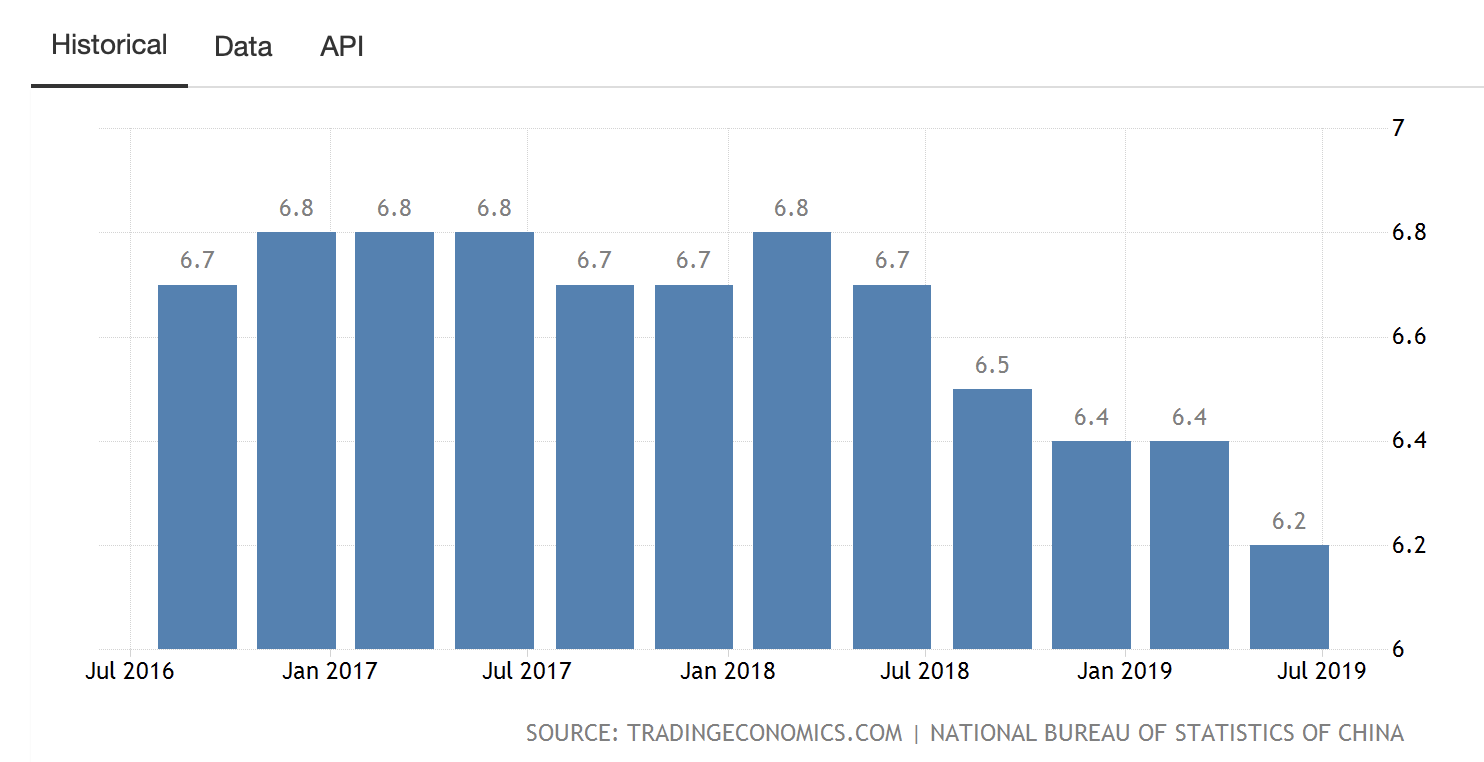

In my view, it’s clear the Chinese have the upper hand here. They have a dictator for life that does not need to worry about elections, the government has complete control over the country’s central bank and its policies, and China has an economy that's expanding at over 6%.

Unfortunately, we don’t have any of that. We have President Trump who has a reelection campaign next year, has no control over the Fed, and the U.S. economy will be lucky if it can sustain positive GDP growth this year and in 2020.

Also, President Trump is not the easiest of Presidents for the Chinese to deal with. President Trump wants to equalize the playing field and make China/U.S. trade fairer and more beneficial for the U.S.

The problem is that this is not beneficial for China and time is on China’s side. Furthermore, the best strategy for the Chinese is likely to stall, wait until the outcome of the U.S. election, and see if they can negotiate with a “softer," more accommodative Democratic President.

Therefore, a comprehensive U.S/China trade deal is far from certain (not likely even in my view), and may not even happen at all until after the 2020 election. This will likely put further pressure on the U.S. consumer, U.S. corporate profits, and will likely help tilt the U.S. economy into a recession just in time for the 2020 Presidential election.

The Bottom Line

There are a lot of moving parts right now, and this is not an easy market to navigate. A lot is riding on the Fed and what it will do to support equity markets and the overall economy. The bottom line is that market participants may be expecting too much from the Fed and the Federal Reserve may not do all that much as Mr. Dudley suggested.

Furthermore, we are seeing continued weakness in key economic data, corporate profits are essentially flat YoY (H1 2018 vs H1 2019), we are seeing bearish sector rotation, P/E ratios are relatively high, and most sectors are seeing flat or declining YoY earnings growth. Small cap underperformance is troubling, the China/U.S. trade deal is far from certain, and may even be and unlikely occurrence before the 2020 election.

Additionally, we are seeing an alarming number of red flags, which are typically precursors to a recession. Inverting yields, rock bottom unemployment, worsening consumer sentiment/confidence data, contractions in manufacturing, worsening housing, and other leading economic data, etc.

In my view, the Fed is behind the curve and may not be as accommodative as market participants expect it to be going forward. Furthermore, the U.S. economy appears to be weaker than many market participants perceive. Therefore, Fed or no Fed, deal or no deal, the recession is approaching, and it's likely to arrive within the next 6-12 months, 18 at the most by my calculations.

Is it Possible That the SPX and Stocks in General Move Higher From Here?

Yes, it's possible, but once again the Fed holds the key. If the Fed cuts by at least 25 basis points on Sept. 18, comes out with a dovish statement, hinting at further rate cuts and future rounds of QE, the SPX could run up to the 3,100-3,500 level over the next 6-12 months. This is possible, but not probable in my view.

Furthermore, even if the Fed decides to be ultra accommodative and we see SPX hit new all-time highs, the Fed is not likely to delay the inevitable recession for much longer. It's possible to prolong this bull run, but eventually the Fed-induced bubble will burst and a grizzly bear market will likely cut most stocks in half, in my humble opinion.

0 comments:

Publicar un comentario