To the extent modern monetary theory is true, it is unoriginal; to the extent it is original, it is false

Martin Wolf

The state is the most important of all our institutional innovations. It is the ultimate guarantor of security. But its power also makes it frightening. For this reason, people sometimes pretend it is weaker than it is. In one area of economics, this is particularly true: money. Money is a creature of the state. Modern monetary theory, a controversial account of this truth, is analytically correct, so far as it goes. But where it does not go is crucial: money is a powerful tool, but it can be abused.

L Randall Wray of the University of Missouri-Kansas City set out these ideas in Modern Monetary Theory. They have the following fundamental elements.

First, taxes drive money. This doctrine is called “chartalism”. Governments can force their citizens to use the money it issues, because that is how people pay their taxes. The state’s money will thus become the money used for domestic transactions. Banks depend upon the government’s bank — the central bank — as lender of last resort. The IOUs of banks — the predominant form of money in today’s economies — are imperfect substitutes for such sovereign money. They are imperfect, because banks may become illiquid or insolvent and so may default. That is why banking crises are common.

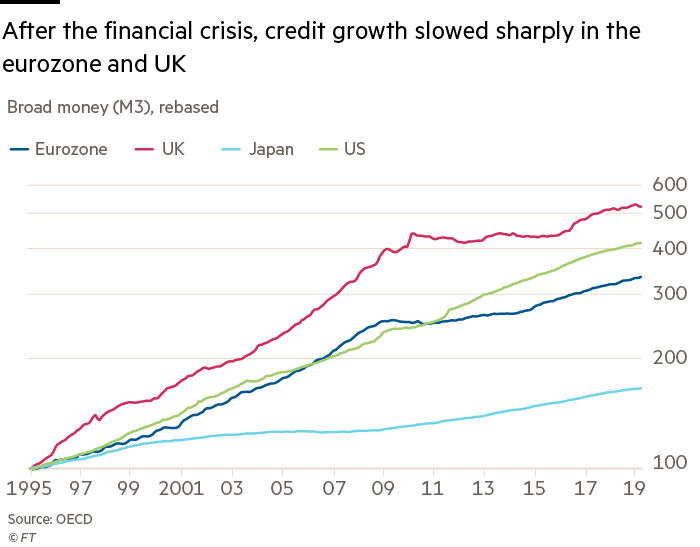

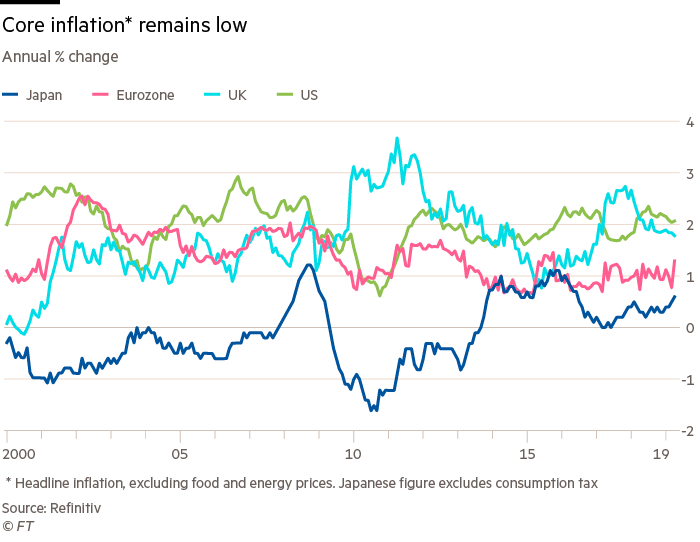

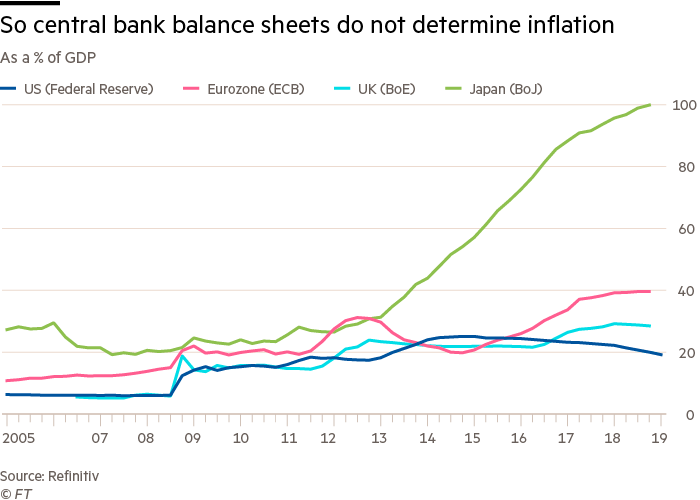

Second, contrary to conventional wisdom, no mechanical relationship exists between holdings of central bank liabilities by banks (that is, reserves) and creation of bank money. Since the financial crisis, central bank balance sheets and bank reserves have grown hugely, but broader monetary aggregates have not. The explanation is that the dominant driver of the money supply is the (risk-adjusted) profitability of lending, which is high in booms and low in busts. The weakness of credit also explains why inflation has remained low.

Third, governments need never default on loans in their own currency. The government does not need to raise taxes or borrow to pay its way; it is possible for it to create the money it needs. This makes it simple for governments to run deficits, in order to ensure full employment.

Fourth, only inflation sets limits on a government’s ability to spend. But, if inflation emerges, the government has to tighten demand, by raising taxes.

Finally, governments do not need to issue bonds in order to fund themselves. The reason for borrowing is to manage demand, by altering interest rates, or the supply of reserves to banks.

This analysis is correct, up to a point. It also has implications for policy. A sovereign government can always spend in order to support demand. Again, expansion of the central bank balance sheet does not make high inflation likely, let alone inevitable. Some believers in MMT argue that the power to create money should be used to offer a universal jobs guarantee or finance programmes such as the Green New Deal proposed by Democrats in the US. But such ideas do not follow from their analysis. These are just suggestions for where the state should spend.

What then are the problems with MMT? These are twofold: economic and political. An important economic difficulty, clear from painful western experience in the 1970s, is that it is hard to know where “full employment” lies. Excess demand may exist in some sectors or regions, and deficient demand elsewhere. Full employment is a highly uncertain range, not a single point.

A still more important economic mistake is to ignore the expectations that drive people’s behaviour. Suppose holders of money fear that the government is prepared to spend on its high priority items, regardless of how overheated the economy might become. Suppose holders of money fear that the central bank has also become entirely subject to the government’s whims (which has happened often enough in the past). They are then likely to dump money in favour of some other asset, causing a collapsing currency, soaring asset prices and booming demand for durables. This may not lead to outright hyperinflation. But it might lead to a burst of high inflation, which becomes entrenched. The focus of MMT’s proponents on balance sheets and indifference to expectations that drive behaviour are huge errors.

These mistakes are economic ones, but there is a related and far worse political error, as Sebastian Edwards of University of California, Los Angeles, has argued. If politicians think they do not need to worry about the possibility of default, only about inflation, their tendency may be to assume output can be driven far higher, and unemployment far lower, than is possible without triggering an upsurge in inflation. That happened to many western countries in the 1970s. It has happened more often to developing countries, especially in Latin America.

But the economic and social consequences of big spikes in inflation can be very damaging.

Yet the same is also true for high unemployment. So, in managing a modern monetary economy, one has to avoid two gross errors. One is to rely on private sector demand too much, since that can all too easily end up with highly destructive financial booms and busts. The opposite error is to rely on government-led demand too much, since that may well generate destructive inflation booms and busts.

The solution, nearly all of the time, is to delegate the needed discretion to independent central banks and financial regulators. Yet proponents of MMT are right that during a period of structurally feeble private demand (as in Japan since 1990) or a deep slump, a sovereign government must and can act, on its own or in co-operation with the central bank, to offset private weakness. There is then no reason to fear the constraints. It should just go for it.

0 comments:

Publicar un comentario