The Similarities Between The 1920s And The 2010s

by: Cashflow Capitalist

Summary

- There are some eerie similarities between the 1920s and 2010s.

- Many of the patterns that played out in the 1920s have been playing out in recent years and decades.

- Accommodative monetary policy fueled debt growth and excessive speculation in the 1920s just as they have today.

- The future may not repeat the past, but will it rhyme?

- Many of the patterns that played out in the 1920s have been playing out in recent years and decades.

- Accommodative monetary policy fueled debt growth and excessive speculation in the 1920s just as they have today.

- The future may not repeat the past, but will it rhyme?

History doesn't repeat, but it rhymes.

This trusty aphorism, often attributed to Mark Twain, strikes just the right balance between perceptiveness and vagueness. Of course, history never repeats. That would be impossible. But rhyming words, though they sound similar, can connote far different concepts.

Indeed, periods of history can, on the surface, look new and involve new elements while also sounding eerily reminiscent of earlier periods. Today's world doesn't look or feel like any prior age of history. Technology has advanced. Entertainment has taken on many new forms. Previously unheard of transportation methods and medical procedures are regularly enjoyed by average people.

And yet, fundamental aspects of human behavior haven't changed. We are still the same flesh-and-blood creatures with the same motivations, still responding to incentives and disincentives.

Every human action spurs a reaction, and on and on, forming cycles, ups and downs. Periods of war and peace. Prosperity and poverty. Innovation and convention.

What prior period of history rhymes with the present one when it comes to finance?

I humbly submit the 1920s as a period of eerie reminiscence to our current decade, the 2010s.

Now, I know many may object to this comparison on the same basis as famed hedge fund manager Ray Dalio, who asserts that we have already reached the end of our long-term debt cycle and are now in the midst of a "beautiful deleveraging." Certainly, from the perspective of interest rates, we have hovered around zero percent on the ultra-short end for about as long as during the Great Depression in the 1930s, but we have not seen the sustained and inescapable deleveraging witnessed during that decade. Nor have we spent the better part of the decade locked in a bitter depression.

In a previous article, I argued that we have not actually reached the end of the road in this long-term debt cycle, but rather that the next downturn will finally get us there. If this is true, then the 2010s are already more like the 1920s than the 1930s. But there are many more similarities that are worth discussing.

Let's start with the non-financial realm:

1. Both decades were periods of intense culture wars between "modernists" and "traditionalists"

Today, you might substitute the word "modernist" for "progressive," as well as the word "traditionalist" for "conservative." Still, the basic meanings of the words hold for both today and the 1920s.

Interestingly, the debates and conflicts between these camps are based on the same subject matter today as they were in the '20s. Only the specifics are different.

Take science for instance. In the 1920s, a fierce debate raged over Darwin's theory of evolution, culminating in the Scopes Trial of 1925. Clarence Darrow, defending the school teacher John Thomas Scopes on trial for the teaching of evolution, represented the modernists. Former Secretary of State William Jennings Bryan represented the traditionalists, who were repulsed by a newfangled theory that did not sit well with a literal reading of the Bible.

The "evolution issue" of today is climate change. The modernist/progressives (perhaps represented by Alexandria Ocasio-Cortez) argue with quasi-religious zeal that climate change will inevitably ruin the planet unless dramatic measures are taken immediately. The traditionalist/conservatives (perhaps represented by Donald Trump) are skeptical of the supposed ravages that climate change will bring, if they accept the validity of the theory at all.

We haven't had the "Scopes Trial" of climate change yet, though perhaps it is coming.

Both decades were also defined by a conflict over mind-altering substances. In the 1920s, it was alcohol, resulting in the Prohibition. In the 2010s, it's marijuana. Though the Prohibitionists had their way in 1920, both production and use of alcohol grew over the course of the decade. Similarly, marijuana prohibitionists had their way throughout most of the country in 2010, but in 2019, it seems inevitable that the plant will be enjoyed legally and recreationally across the country in the foreseeable future.

Both decades struggled with race relations. In the 1920s, the Ku Klux Klan made a resurgence even as the NAACP gained ground and anti-lynching measures were passed. Today, various white nationalist groups seem to be emboldened even as an African American occupied the White House for most of the decade and reparations measures are being endorsed by presidential candidates.

Both decades were marked by high immigration, even as the native population bristled at the influx and took measures to cut off the flow. In the 1920s, this led to the passing of the Emergency Immigration Act of 1921 and then the Immigration Act of 1924, which successively restricted immigration inflows. In the present decade, it led to the election of the most anti-immigration president in decades (echoes of "Build that Wall!" resound in the distance).

Both decades could be seen as periods of female empowerment. In the 1920s, women were empowered by entering the workforce, consuming countless new items in the home, and enjoying new birth control methods. In the 2010s, women felt empowered by the first female presidential nominee of a major party, pushes for equal pay for equal work, and the 2017-2018 Women's Marches.

I might also add that the Russian Revolution of 1917 spurred a worldwide wave of interest in Marxist thinking. Socialism became feared and loathed in capitalist countries in the 1920s, even as its popularity took off with American immigrants and laborers. Similarly, "socialism" was a dirty word in American politics prior to Bernie Sanders' 2016 presidential campaign. Now, it's the hot new movement.

2. Both decades began with a major economic downturn

We all know about the Great Recession of 2008-2009 (extending into the early years of the 2010s in the experiences of many, though perhaps not in official reckoning). Most people probably do not know that the 1920s also began with a devastating economic downturn, worse than the Great Recession by many standards.

In his excellent book, The Forgotten Depression, Jim Grant documents the severity of the downturn.

GNP plummeted from $91.5 billion in 1920 to $69.9 billion in 1921, a 24% nominal decrease.

Even adjusting for falling prices shows a 9% decline. Compare this to the Great Recession's 4.3% inflation-adjusted decline in GDP.

Industrial production fell by 31.6% from 1920 to 1921 compared to the Great Recession's decline of 16.9%. Unemployment reached 15.3% in 1921 (though other estimates put it as high as 19%) compared to the Great Recession's peak unemployment rate of 10%. In but one area the Great Recession has the recession of 1921 beat: In 1921, the Dow Jones Industrial Average fell 46.6%, while the Great Recession brought about a decline in the DJIA of around 48%. Peak to trough, corporate profits plunged 92% (Grant, 67-69).

Wartime deficit spending, accommodated by the Federal Reserve's easy money policy through 1919, created a nasty inflation that needed to be mopped up. And mopped up it was, when the Fed lifted its discount rate from 4% in late 1919 to 7% in 1920 (we'll return to the subject of interest rates shortly).

In any case, though much shorter-lived, the recession of 1920-1921 was at least as sharp and painful as the Great Depression or the Great Recession, despite being the last "governmentally unmedicated" (to use Grant's words) recession in American history. This is how the 1920s began, just as it was how our present decade began.

3. Both decades were marked by economic growth and prosperity

Unemployment averaged 3.3% from 1922 to 1929. But the average doesn't tell the whole story.

After peaking at ~15% in 1921, unemployment fell to 6.7% in 1922 and 2.3% in 1923. Compare this to the much more drawn out Great Depression, in which unemployment jumped from 3.2% in 1929 to 8.7% in 1930, continuing to shoot up to 25% by 1933. Compare also to the tepid recovery following the Great Recession, edging downward from 10% unemployment in October 2009 to 9.4% in October 2010 and 8.8% in October 2011 to finally arrive at our current 4%.

We all know the story of economic growth in the 2010s: Moderate yet respectable 2%-average annual GDP growth. The longest stock bull market in history. Innovators continuing to find new ways to improve life via the Internet.

The 1920s were also an age of innovation. "In 1920, only 35 percent of homes had electricity; by 1930 the number was 68 percent. Similar increases occurred in the number of households with indoor plumbing, washing machines, and automobiles." (From America: The Essential Learning Edition, Vol. 2, p. 786).

From 1924 to 1929, gross national product (GNP) increased annually by 7%. Per capita income grew 30% from 1922 to 1928, and though that increase in national income was not distributed equally, workers were getting better off at a rapid rate. Real earnings for employed wage earners increased 22% from 1922 to 1928.

During this same time period, industrial production rose by 70% while the average workweek shrank by 4%. Illiteracy nearly halved during the decade as education spending quadrupled.

This as total federal expenditures shrank from $5.1 billion in 1921 to $3.3 billion in 1929.

The US increasingly exported its numerous products overseas: movies, vacuum cleaners, radios, toasters, refrigerators, cars, and other gadgets. By the end of the decade, America was producing around 85% of the world's cars (Data from the previous three paragraphs taken from Silent Cal's Almanack, 19).

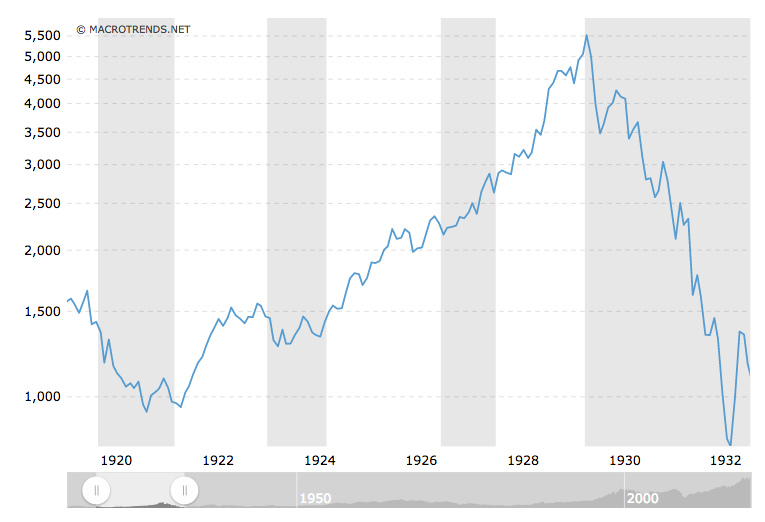

Total wealth nearly doubled during the 1920s, and GDP rose by 70%. And all this corresponded with a booming stock market, which enjoyed 20% average annual gains from 1921 to 1929. See, for instance, the marvelous bull run of the Dow Jones Industrial Average:

Source: Macrotrends.net

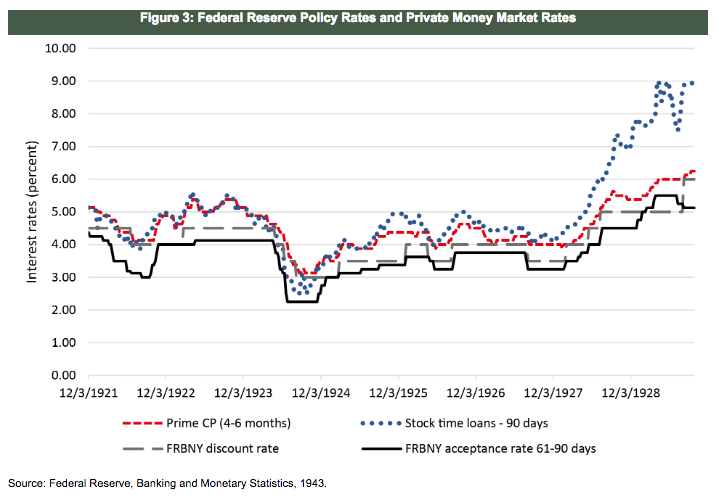

4. Both decades had similar interest rate patterns

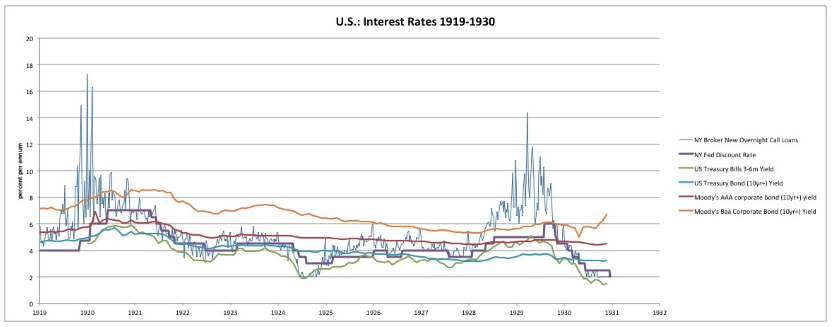

While the Fed operated a little differently under the gold standard, it did have something similar to the "Fed Funds rate," namely the New York Fed discount rate, all short-term loans with the Federal Reserve although not all overnight loans.

Source: New World Economics

This chart is a bit busy and the writing is small, so you may need to click on the image to enlarge it.

Notice that the bold purple line (the NY Fed Discount Rate) stair-stepped up from 4% in 1919 to a staggering 7% in 1920 - an effort by the central bankers to reign in postwar inflation, as previously stated. This ought to remind us of the 4.25% hike in the Fed Funds rate carried out prior to the Great Recession.

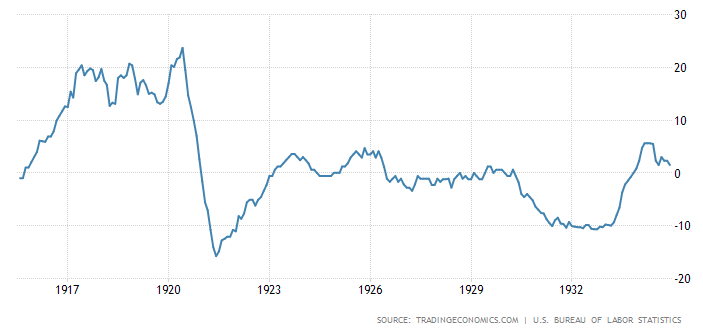

After the recession of 1921, it pushed the discount rate back down to around 4% or under, where it stayed for the majority of the decade, despite inflation rising a bit above 4% in 1923 and 1925-26:

Inflation rate from 1914 to 1940. Source: Trading Economics

In other words, real (inflation-adjusted) interest rates on the shorter end of maturity were, at times, near zero, other times 5 or 6%, and often the same as the nominal rate.

Near the end of the decade, just like our own, the Fed crept its main rate back up in order to tame a raging stock market. At the highest, the NY Fed discount rate hit 6%. This proved too much for the economy to bear and pricked the dangerously inflated stock market bubble.

Notice one other thing: The orange and red lines in the chart of interest rates above are investment grade (red) and non-investment grade (orange) bond yields. After a slight rise at the beginning of the decade, they fell along with the Fed discount rate for the majority of the decade. Investment grade bonds enjoyed a fall in yields from above 6% to below 5%. Non-investment grade bonds enjoyed a drop from above 8% to below 6%. The same has happened in the present decade, in which corporations are enjoying some of the lowest cost of debt in history.

5. Both decades witnessed a rise in installment plan purchases

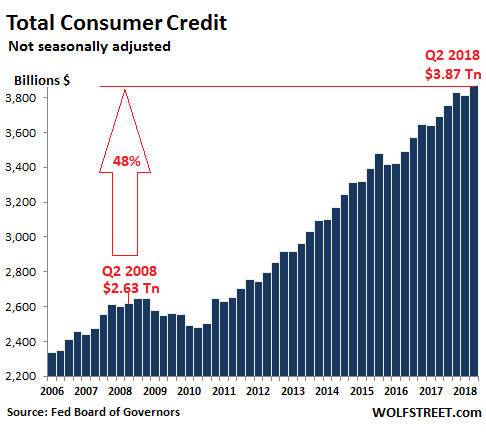

In another previous article, I discussed the way in which low interest rates hurt the poor and middle class. One way they (inadvertently) do this is by inducing lower-earners to forego saving and instead purchase all sorts of durable goods (and even some non-durable products) on installment plans. "Buy now, pay later" seems to be the motto of the decade, whether it be for vehicles, cell phones, TVs, furniture, medical bills, or even small items like bed sheets or concert tickets. Hence the explosion of consumer debt:

Source: Wolf Richter

Funnily enough, the same motto applies to the 1920s, which saw for the first time in American history a rise in installment buying. Prior to this, consumer debt was heavily frowned upon. But through a combination of low interest rates and a burgeoning advertising industry, Americans were swayed to "buy now, pay later."

The authors of America: The Essential Learning Edition attest that as "paying with cash and staying out of debt came to be seen as needlessly 'old-fashioned' practices, consumer debt almost tripled during the twenties. By 1929, almost 60 percent of American purchases were made on the installment plan" (p. 786).

The country seemed to be engulfed in a new consumerist culture, fueled by targeted radio and print ads. One journalist, who apparently viewed this newfound consumerism unfavorably, penned in 1920:

During the war, we accustomed ourselves to doing without, to buying carefully, to using economically. But with the close of the war came reaction. A veritable orgy of extravagant buying is going on. Reckless spending takes the place of saving, waste replaces conservation (America, 785).

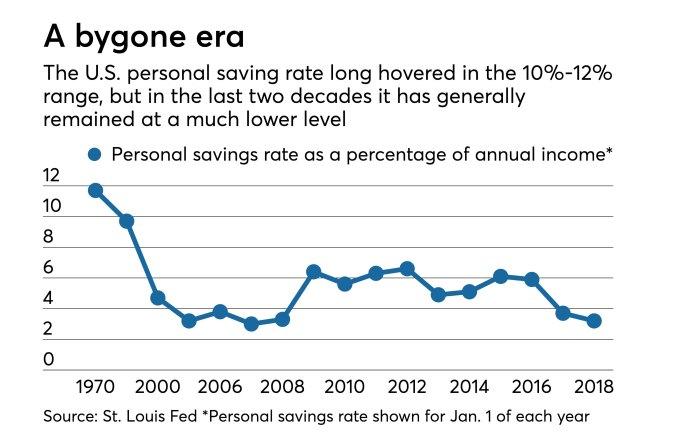

This might seem like excessive exaggeration, but data backs up the idea that the balance of spending and savings became significantly tilted toward spending in the '20s. One study shows that the personal savings rate fell from 12.9% in 1920 to 4.1% in 1930, before shooting back up in the Great Depression to end the decade in 1940 at 12.6%.

This should remind us of our own era, in which the personal savings rate has collapsed right along with interest rates:

Source: American Banker

And an increasing amount of this spending during the decade was channeled through installment buying. According to data compiled by the San Francisco State University, in 1925, there was $1.38 billion of consumer credit outstanding. In 1929, there was $3 billion of consumer credit outstanding, and $7 billion worth of consumer goods were purchased on installment plans - this in a year when the US economy produced $105 billion in GDP.

By 1927, 15% of all consumer durables were bought on an installment plan. Sixty percent of automobiles were financed, and an astonishing 80% of radios were financed. Around 1,500 installment credit companies sprang up in the 1920s, competing with each other to capture relatively low-interest consumer loans.

Average purchases of major durable goods rose from 3.7% of disposable income between 1898 and 1916 to 7.2% between 1922 and 1929. Accompanying this rise in purchases of durables was a drop in the personal savings rate, from 6.4% of disposable income in the former period to 3.8% in the latter.

Meanwhile, on the top end of the income spectrum, just like in our present decade, the wealthy redirected their savings into investments. While 80% of American families had no savings at all in the '20s, the top 0.1% of earners enjoyed 34% of the nation's savings, and the top 2.3% of earners held fully two-thirds of the nation's savings. Income (including dividends and capital gains) for the top 1% of earners increased by 75% from 1920 to 1929.

Steadily falling corporate bond yields (i.e. cost of debt) along with high innovation and productivity growth helped corporate profits soar 62% from 1923 to 1929. This certainly "rhymes" with rising corporate profits during our current decade, although those have come without much innovation or productivity growth.

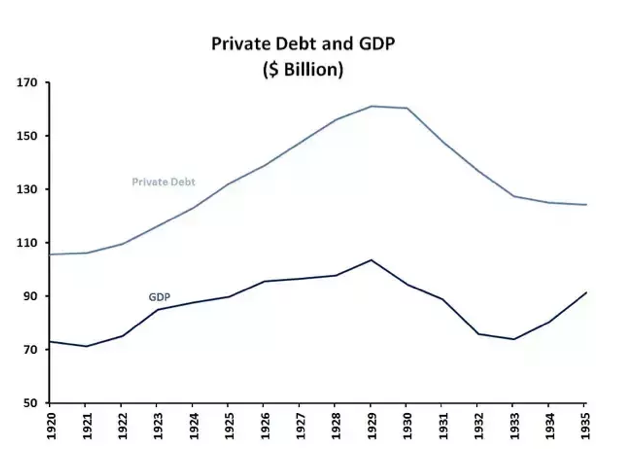

6. In both decades, a large portion of total debt growth was corporate debt

Staying on the theme of corporate debt, it's important to note that during the 1920s, corporate debt expanded rapidly over the course of the decade. We can see, for instance, the run-up of private credit in this chart:

Source: Derived from Historical Statistics of the United States, Census Bureau

Source: Derived from Historical Statistics of the United States, Census Bureau

By the end of the decade, corporate debt had become the largest share of the total credit market by a wide margin.

Source: New World Economics

Source: New World Economics

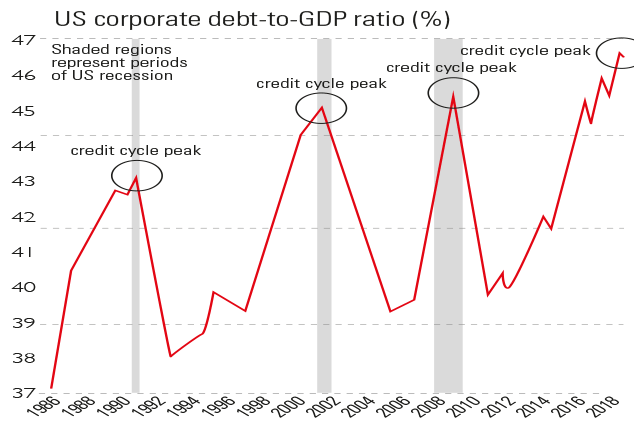

Second only to corporate debt was mortgage debt, which grew by more than eight times just from 1920 to 1929. Both of these - corporate and mortgage debt - echo our own decade.

Mortgage debt quickly bounced back during the recovery after the Great Recession, and corporate debt roared back even more strongly, now cresting 46% of GDP.

Source: MoneyWeek

7. In both decades, the Fed's balance sheet shrank late in the decade

In the 2010s, Fed Treasury assets remained well in excess of 10% of GDP. Total assets (including mortgage-backed securities) exceeded 20% of GDP.

Some say that rising interest rates late in the decade were a result of high demand for borrowed money, mainly from investors speculating in the stock market. This is only partially true. For the most part, private market rates (including broker lending rates and money markets) followed the course of the Fed's discount rate over the decade. Margin rates only disconnected in 1928 and 1929. This is when the "equity" portions of margin loans compressed down to 10-20%, meaning that speculators would borrow 80-90% of the cost of stocks in order to invest.

By the second half of 1928, though, most of the damage had already been done. Credit expansion had already spiraled out of control. Much focus tends to be placed on the astonishing margin debt-to-GDP of 8.14% hit in 1929 - and it deserves astonishment - but such a lofty number isn't reached under normal financial circumstances. Even in our current historically low interest rate environment, margin debt peaked only at 3.37% of GDP (higher than in 2000 or 2007) and, after a brief deleveraging in December, is on its way back up in 2019.

What role did the Fed play in this debt expansion?

According to the Federal Reserve itself:

We find that changes in all three policy instruments [the discount rate, the slightly shorter-maturity acceptance rate, and Treasury holdings] are followed by changes in market interest rates during the following week. Changes in the discount window rate appear to have large effects ... Purchases of Treasury securities seem to have also influenced private rates.

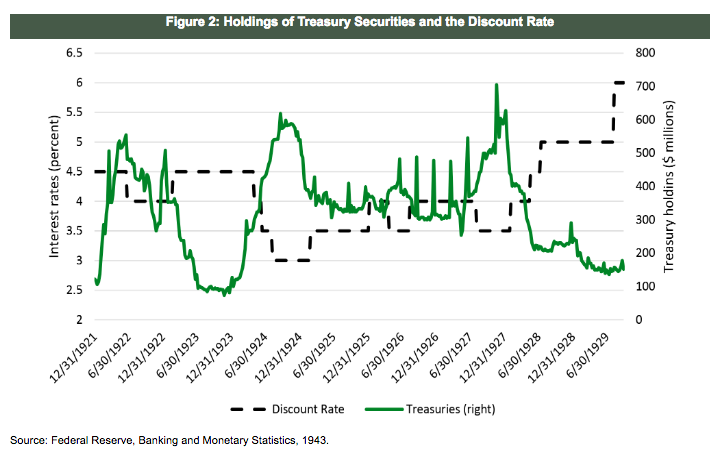

Here we return to the Fed's balance sheet. From Q4 of 1927 to Q2 of 1929, the Fed shrank its Treasury holdings from $700 million to under $200 million. This had the duel effect of further lifting interest rates, making borrowing more expensive, and finally (after a long period of easy money) attracting investment capital away from higher-risk assets and back to bonds.

Interestingly, in the late 1920s, the Fed found itself in a similar position as it has been in the last few years - shrinking its balance sheet while raising interest rates after a long period of holding interest rates lower than they otherwise would be. Only, in the '20s, the Fed had much smaller holdings of Treasuries and so had to rely more heavily on interest rate hikes, going all the way to 6%.

What Does the Future Hold?

Now that interest rates appear to have paused and balance sheet reduction will presumably soon pause at the timid hands of Fed officials who don't want to make the same mistakes as in the past, where do we go from here?

It's clear from the experiences of the Great Depression and Great Recession that deleveraging does not occur unless serious pain forces it to occur. So the economy and markets will eventually tread down one of two paths. Either monetary policy continues to be accommodative and debt levels remain elevated (or even rising) or it ceases to be accommodative and a very painful deleveraging (mainly concentrated in housing, corporates, and municipalities) unfolds.

I think central bankers are too skittish to let the latter scenario play out. That leaves the former. But how long can we tread down the path of ever-rising debt? This line of reasoning persuades me that some sort of jubilee (debt forgiveness) scenario will eventually be implemented by fiscal policymakers or monetary policymakers or both (see my article on the Year Of The American Jubilee).

The future is opaque, but one thing about it is certain: It may not repeat, but it will rhyme.

0 comments:

Publicar un comentario