The National Debt Math Doesn't Add Up

by: Doug Eberhardt

Summary

- Presidents campaign on promises to reduce an out of control national debt yet the debt keeps marching higher during every Presidents term.

- The Budget's set by Congress always fall short.

- What supports government spending and what does the data tell us today?

- Everyone ignores the elephant in the room; interest on the national debt.

- Gold & silver maintain purchasing power over time. Dollars pay interest and held up well. One has $22 trillion of debt backing it.

- The Budget's set by Congress always fall short.

- What supports government spending and what does the data tell us today?

- Everyone ignores the elephant in the room; interest on the national debt.

- Gold & silver maintain purchasing power over time. Dollars pay interest and held up well. One has $22 trillion of debt backing it.

When it comes to the national debt, it amazes me how the debt is such an important Presidential campaign issue to criticize the past President while running for office, but once the incumbent takes the reins, Congress and special interest groups take over and get to work spending every dime and more through the process known as legislation that the President rubber stamps their approval.

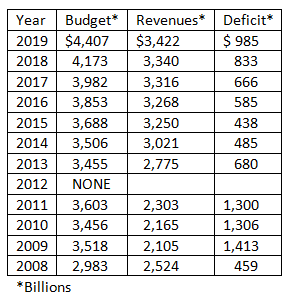

It is Congress' job to "raise and provide public money and oversee its proper expenditure." Of course the words "proper expenditure" Congress ignores. Just take a look at the budget set out by Congress for the last 11 years and the actual result.

Yes, revenues have increased every year. That's a good thing. But living within its means, is not what politicians on both aisles do well. Yes, both Republican and Democrats are at fault here, not just the head honcho.

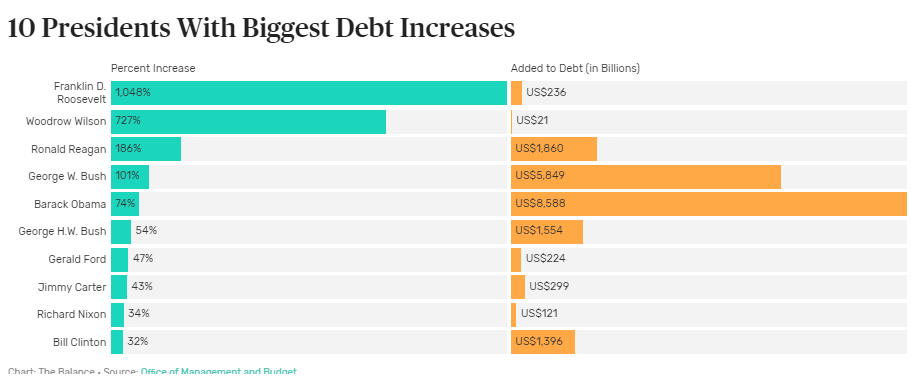

Here's how past presidents have stacked up when it comes to percentage increases for the national debt.

Congressional Budgets Always Fall Short

There has been failure after failure of meeting the budget set out, and many would consider this time-frame of declining unemployment to historic lows and the best ever for the stock market hit in 2018 "roaring" for most individuals. Up until this year consumers in general have enjoyed increased income year after year and have maintained a good savings rate. That’s all changing now with the Fed raising rates and putting a damper on things. It’s not the trickle down effect that Trump was looking for with his tax cuts. Let's look at the data a bit more to see where we really are and try and conclude how this may affect your investment strategy moving forward.

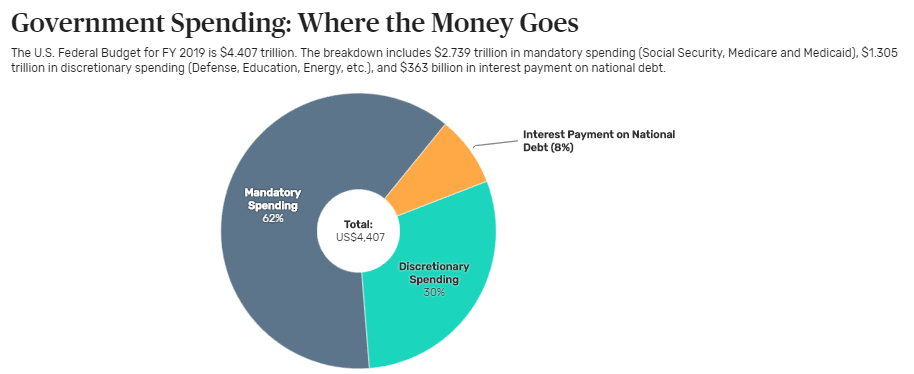

Where The Money Goes

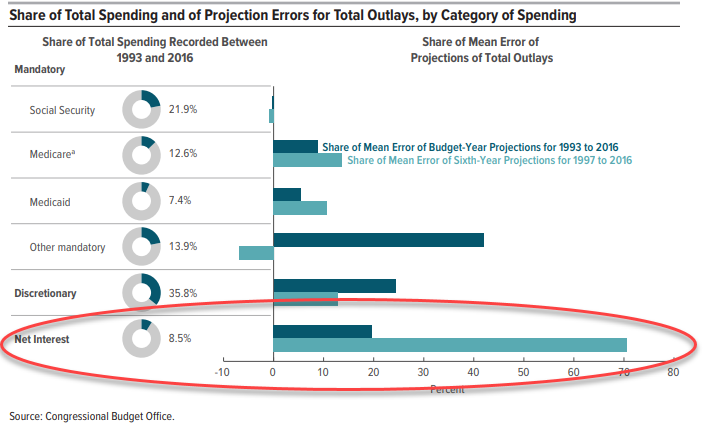

Mandatory spending by government and future obligations are one thing, but projections by the CBO never seem to keep up with Congressional spending. Budgets come out and are ignored every year, even the so called good years.

For 2019 the interest on the national debt is projected to be $363 billion. In 9 years it is supposed to have doubled to $761 billion if interest rates rise. But on what amount of debt? It’s not like Republicans are doing anything to rein in spending and reduce the national debt as Trump said he would. And if Democrats take over even more in 2020, one can speculate quite easily that social program spending will increase as most all democrats running or on the finance committee are or will go after banks and the wealthy thus freeing up more money towards a “Green New Deal” among an increase in other public services.

At a time of the uber wealthy meeting in Davos concentrating on climate change, one can expect a change for the business climate in the near future as well, and it won’t be pretty if you are an investor. At times it will be great and at other times, a hint of a bigger recession looms, if one does the math. An investor must have the ability to be able to trade both sides of the market in the years ahead.

What Supports Government Spending?

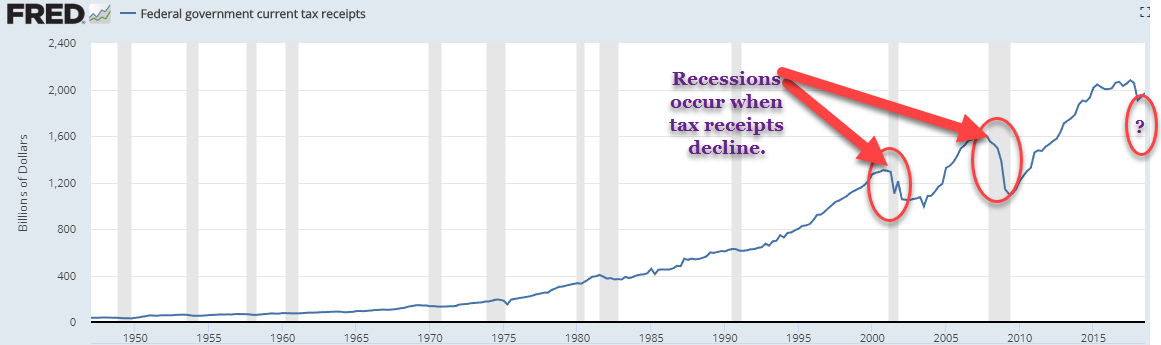

Tax receipts are what one should look at to see if the spending by Congress is getting out of control.

When the government keeps spending, in good or bad or war times, there is an eventual period of time where it catches up to them. This is what we call a recession. Judging from current tax receipts, we may be on the verge of a recession within the next year, but we need to look at the data a bit closer to see if it backs it up.

This is a good time to review GDP again which is essentially what backs the U.S. dollar because a strong dollar is a sign of a healthy economy.

GDP = C + I + NX + G

where:

“C” is equal to all private consumption, or consumer spending, in a nation’s economy“I” is the sum of all the country’s businesses spending on capital

“NX” is the nation’s total net exports, calculated as total exports minus total imports. (NX = Exports – Imports)

“G” is the sum of government spending

Business spending has slowed for the third-quarter of 2018 and the US trade deficit with China hit a record in January 2019.

But the two most important parts of the GDP equation above are consumer and government spending. If consumers are spending, in general, the government can cut its spending to help stimulate the economy.

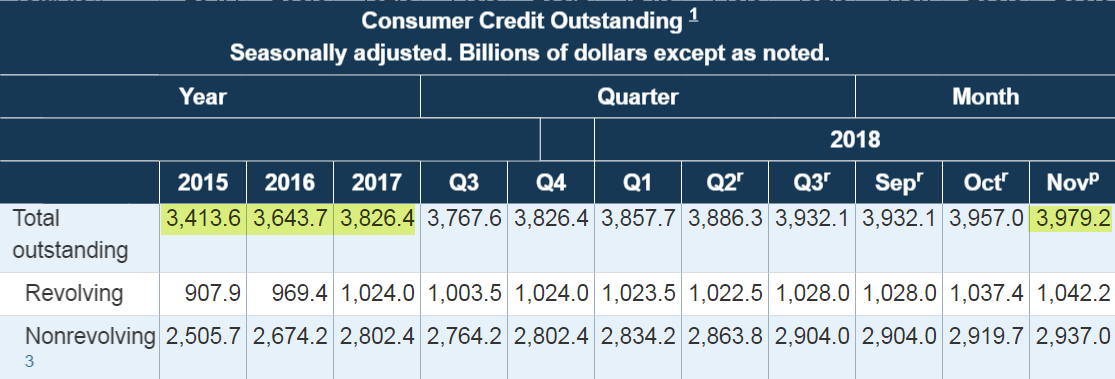

Today we have consumer spending slightly increasing but it is clear they are doing the spending by using more credit and doing it at a higher rate than before the last recession. This is confirmed with the fact that the Personal saving rate has also declined to just 6%, the lowest since January 2014. Part of the increase in income are the minimum wage laws that have been passed in many states the past few years and in general, more people working with record low unemployment.

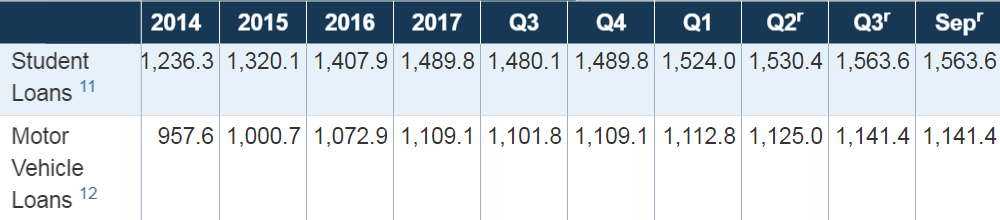

But the consumer has bigger issues than meets the eye right now. Consumer credit outstanding is increasing as well as student loan and auto loan debt with higher interest rates.

Interest rates on Credit card plans and New Car Loans have moved up with the Fed raising rates from 11.91% in 2013 to 14.38% Q3 2018 for Credit cards and for New Car Loans, 4.7% in 2013 to 6.4% by Sept 2018.

We can thank the Fed for this as they clear their balance sheet.

If consumer spending is 70% of GDP, and the consumer is tapped out even with higher wages for some, the government is all that is there to pick up the spending pace and we know they have and will. It’s what they do best. But there is one glaring issue with government spending that is ignored; the Interest Payment on National Debt.

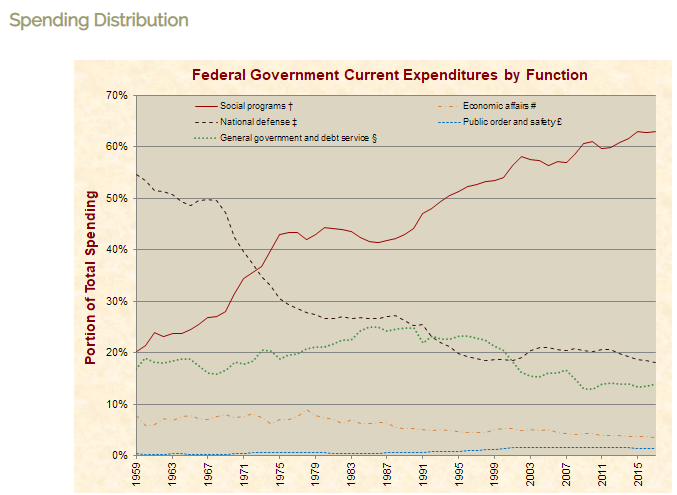

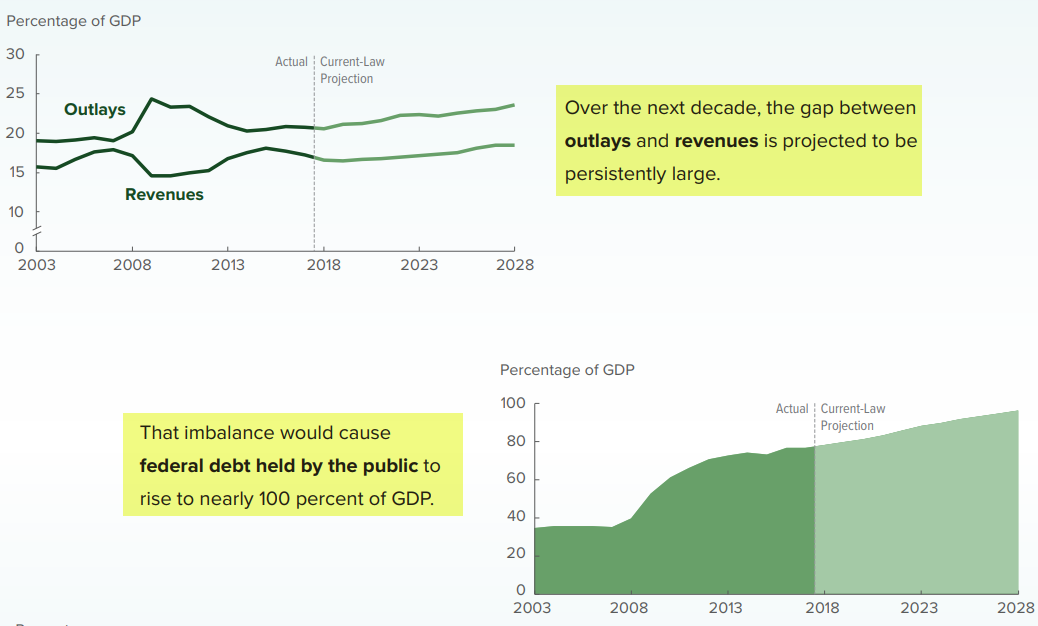

This is the outlook for the next decade for government outlays and revenue.

Not only are projections moving forward showing a huge imbalance, past predictions on each category of spending has been off by a large percentage, especially related to Net Interest. Is it any wonder that the WSJ finally came out on Friday and said that the Fed may be moving closer to ending its balance sheet reduction?

One recent article from The New York Times quotes Marc Goldwein, senior policy director at the Committee for a Responsible Federal Budget says that "by 2020, we will spend more on interest than we do on kids, including education, food stamps and aid to families." You'll see more and more talk about the interest on the national debt in the years to come. But for now it is swept under the rug as most ignore the elephant in the room.

Even the Council on Foreign Relations - CFR has weighed in on the national debt dilemma saying that "Major budget legislation signed by President Donald J. Trump, along with continued growth in entitlements and higher interest rates, will see the debt nearly double by 2028 [PDF], coming close to the size of the entire U.S. economy."

We'll find out what the Fed says this week, but they have been talking the dovish talk for a couple weeks now and the stock market has shot up without looking back. While we most likely have a pullback in the market post Fed, it should be followed by a run to the 2900 level in the S&P.

What About Gold Today?

In my last article from November, I stated that gold had one more dip after this run up. I try and time my articles with these turns the best I can, as well as in my comments. Come Monday, 1/28, we may be close to a top into the Fed meeting this week and a run lower in metals commences.

Senior Editor Gil Weinreich had a podcast where he asked the Pros And Cons Of Owning Gold.

He was correct to point out that gold's returns over time are unimpressive when comparing to stocks. But he also said that it is not the relevant comparison and I agree.

If one were to look at gold as a currency, then it is true, it has had times where it has performed well, and other times it has not versus stocks. The same can be said of the U.S. dollar though. Technically one could have a podcast titled "Pros And Cons Of Owning Dollars." The fall from 2002 to 2008 in the dollar from 120 to 74 was 38%. This means your U.S. stocks had to earn 38% just to break even during that time.

In that context, gold and the dollar each have not outperformed stocks but only one of those two has maintained purchasing power over time. That's the key. My 1964 90% silver quarter can still buy me a gallon of gas exchanged for the scrip of the day and my 1965 quarter buys me 25 cents worth of gas since that year. This scenario has proven itself over time and I'll also point out that only one of those two; gold and the dollar, has trillions of debt backing it. Thus it could be said that gold is the best hedge against the one thing that most all other assets (dollars, bonds and CD's) are priced in; dollars.

Asset allocation models tell you to dip into one over the other. Gold is over 31% below its all-time highs. The dollar is 31% above its 2008 low. Which will be a better value moving forward based on the analysis of the data above if GDP really does back the dollar? The answer is clear if you connect the dots from this article.

My recommendation is to buy physical gold and silver on any dips and if one can't do that then one of the various ETFs like (GLD), (SLV), (OUNZ) that represent ownership, even though you'll see many post reasons not to in the comment section. I view these ETFs more as trading vehicles, not long term wealth building. For sentiment on trading miners, like triple leveraged ETFs (JNUG), (NUGT), (JDST) and (DUST), please follow along in the comment section.

0 comments:

Publicar un comentario