Recessions and bear markets — the terrible twins

A global recession is unlikely this year, unless a bear market causes one

Gavyn Davies

The severity of the collapse in markets late last year was quite surprising, given that global gross domestic product continued to grow very close to trend in the fourth quarter. Many global markets, including the major risk assets, the yield curve and credit spreads, are now pricing a probability of recession of at least 50 per cent within 12 months.

This recession risk seems far too high, especially in the US. The strength of the American labour market, and the recent indications from the Federal Reserve that it will pause its rate increases, should protect the economy from a severe setback this year. As goes America, so goes the developed world.

With investors too pessimistic about immediate economic prospects, risk assets may continue to recover from present depressed levels. An alternative, however, is that asset price turbulence will return, setting in train a tightening in financial conditions that independently causes a recession.

The inter-relationships between recessions and bear markets are complex and not very well understood. It is clear that they tend broadly to coincide in their timing. However, it is far from clear which causes which.

Economists often assume that recessions are basically caused by economic fundamentals, with the financial markets reacting when these fundamentals deteriorate.

Sometimes investors may be able to discern rising recession risks before they actually appear in hard economic data, in which case the onset of the bear market may precede and apparently “predict” the official start of the economic downturn.

Notwithstanding these varying time lags, the main direction of causation in these examples is from the economy to the markets, not the other way round. Understanding this mechanism is one of the main justifications for employing economists in the financial markets in the first place.

However, in recent cycles, leverage in the financial system has generated such large gyrations in asset prices, liquidity provision and risk appetite that it has independently caused recessions in the real economy.

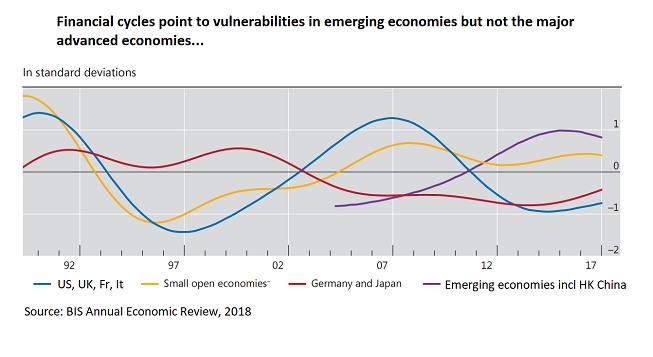

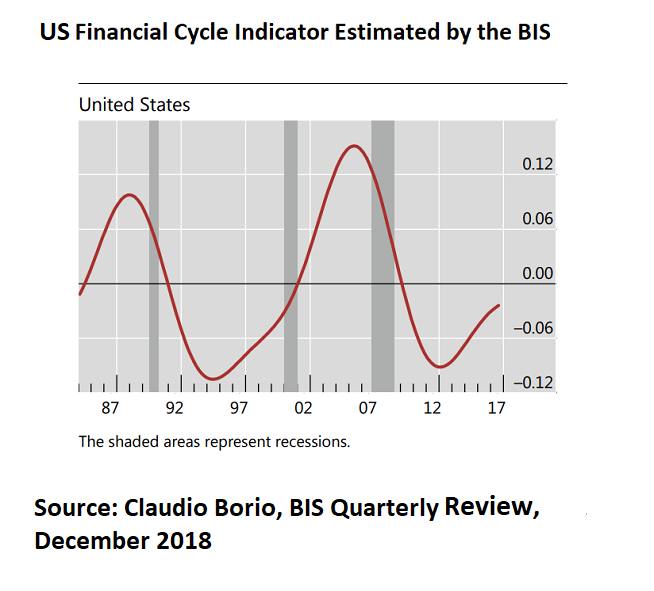

Recent work by Claudio Borio at the Bank for International Settlements, has argued persuasively that, since the mid 1980s, the financial cycle has operated with a much longer amplitude than the economic cycle, and that it has predicted the onset of economic recessions.

There is no doubt that a collapse in the financial cycle was the dominant force during the recession of 2008-09. Fortunately, the current state of the financial cycle is not pointing to severe vulnerabilities in the US and other advanced economies, though many emerging markets, including China, seem very overstretched (see appendix).

An ambitious objective for macro-economists would be to develop models that are capable of understanding and forecasting financial and economic variables within a single, all-encompassing system of equations. However, even the most advanced macroeconomic models currently in use in the central banks are some distance away from such an achievement.

This uncertainty about the appropriate model has fostered different interpretations about the present economic conjuncture, even among mainstream new Keynesian economists who usually agree on the main economic issues:

1) The leadership of the Fed is optimistic that the US economy will slow this year, but that recession risks are low, because the labour market, corporate finances and financial imbalances in the private sector remain in good shape. When the markets realise this, asset prices will recover and the FOMC may resume its tightening path. However, if financial turbulence returns, the central bank will be willing to relax policy, using both lower interest rates and a slower run down in the balance sheet. A data determined Fed will not make a large policy error.

2) Ben Bernanke recently argued that economic expansions do not die of old age, but are murdered, presumably by the central bank. This implies that most recessions are caused by a tightening in monetary policy needed to keep inflation in check. This standard view, stemming from repeated episodes before the 1980s, sees little recession risk this year because inflation remains well below target.

3) A more pessimistic assessment, supported by Lawrence Summers, is that a recession is at least 50 per cent likely in the next year or two. My interpretation of Summers’ remarks is that he expects a spontaneous slowdown in aggregate demand, triggered by the Chinese slowdown, the depressing impact of secular stagnation on equilibrium interest rates and a failure of the US fiscal authorities to prepare infrastructure programmes in advance to stabilise demand. On this view, recent financial turbulence is correctly anticipating, not causing, a weakening economy.

4) A different view is that financial instability will be sufficient on its own to cause the next recession. Brad DeLong argues that only one of the past four recessions (in 1979-82) was “conventionally” caused by a hostile Fed, while the other three were directly caused by instability in the financial system. While the specific trigger for the next downturn is inherently unpredictable, he thinks the culprit will be a sudden, sharp “flight to safety” after the revelation of a fundamental (but unexpected) weakness in financial markets. That, says DeLong, is the main factor that has been generating downturns since at least 1825.

Conclusion

Bear markets and recessions occur as terrible twins, but each can cause the other, and they may interact to make each other worse.

Optimists think that advanced economies are safe from a severe downturn, mainly because inflation is still very low and the financial cycle is not over-stretched. Meanwhile, pessimists think that stagnationary forces will prevail, perhaps triggered or exacerbated by an unpredictable financial shock, and they fear that policymakers will be unable to stabilise imploding aggregate demand. They also point to extremely advanced financial cycles that may be ready to implode in China and other emerging markets.

In my opinion, the optimists probably have the weight of evidence on their side for now, especially since the Fed has revealed its true, dovish colours. Recessions and bear markets may both be avoided in 2019. But there are no certainties in this field, just informed guesses.

Appendix: BIS estimates of the financial cycle

0 comments:

Publicar un comentario