Thoughts On Friday's Dollar Coup

by: The Heisenberg

- On Friday, a double whammy from the PBoC and Jerome Powell sent the dollar tumbling, much to the delight of those hoping the greenback would take a breather.

- This helps to shore up delicate sentiment in emerging markets where outflows have picked up amid concerns about an increasingly challenging external environment.

- Here's a quick recap of global dollar liquidity dynamics, a visual trip through Friday's action and a quick note on September.

- This helps to shore up delicate sentiment in emerging markets where outflows have picked up amid concerns about an increasingly challenging external environment.

- Here's a quick recap of global dollar liquidity dynamics, a visual trip through Friday's action and a quick note on September.

On Wednesday, I suggested that if you're long risk assets of any kind, you're implicitly short the dollar (UUP).

That's not exactly some kind of revelation. That is, it's no secret that the proximate cause of the emerging market (hereafter "EM") unwind is hawkishness from the Fed and the concurrent USD-positive widening in the policy divergence between the U.S. and the rest of the world.

When you think about idiosyncratic flareups in Turkey and Argentina (to name two), you should view them through the lens of vulnerability to a rollback of post-crisis accommodation by developed market (hereafter "DM") central banks. The Fed is the furthest along on the normalization path and U.S. fiscal policy is prompting the FOMC to lean more hawkish than they otherwise might.

Additionally, the increased Treasury supply necessitated by the tax cuts and spending bill helped catalyze an acute dollar funding squeeze in Q1 and at least two EM central bankers (the RBI's Urjit Patel and Bank Indonesia's Perry Warjiyo) have cautioned Jerome Powell to be mindful of these dynamics when thinking about the future course of Fed policy and the pace of balance sheet unwind.

Additionally, the increased Treasury supply necessitated by the tax cuts and spending bill helped catalyze an acute dollar funding squeeze in Q1 and at least two EM central bankers (the RBI's Urjit Patel and Bank Indonesia's Perry Warjiyo) have cautioned Jerome Powell to be mindful of these dynamics when thinking about the future course of Fed policy and the pace of balance sheet unwind.

Some developing economies are more vulnerable than others, and there of course are idiosyncratic factors at play (e.g., Turkish President Recep Tayyip Erdogan's recalcitrant attitude on rate hikes).

But the entire EM complex benefited from the hunt for yield catalyzed by a decade of DM accommodation that pushed investors out the risk curve and down the quality ladder. Now, the tide is going out on that, which means the entire space is exposed to a greater of lesser degree.

(Source: BofAML)

(Source: BofAML)

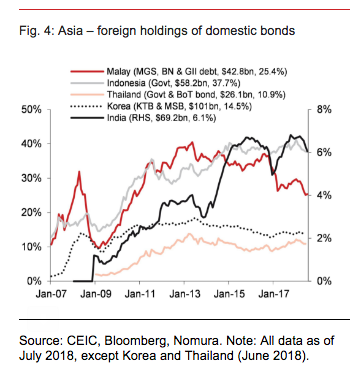

Note how I mentioned BI's Perry Warjiyo above. Indonesia has hiked rates four times since May in an effort to shield the rupiah from the storm. As of July, foreign bond ownership in Indonesia was nearly 38% of outstanding.

(Source: Nomura)

(Source: Nomura)

In case it isn't clear enough, the problem with that in an environment where the global hunt for yield is reversing on the back of Fed tightening is that it sets up a potential exodus, with serious consequences for countries that rely on external funding. On Tuesday, Indonesia's Finance Ministry said it's aiming to reduce the amount of sovereign debt owned by offshore accounts by nearly half, to 20% from the 38% shown above. That's an effort to make the country less vulnerable to episodes like what's going on right now.

The risks grow when acute flareups (e.g., Turkey) prompt investors to indiscriminately abandon EM assets if for no other reason than to fund redemptions. Here's something I posted on Twitter Friday morning that speaks to this:

Consider that with the following excerpt from a note penned by Nomura's Charlie McElligott:

Just as QE pushed investors into riskier EM assets, DM monetary policy normalization stands to have the opposite effect, refocussing investor attention from EM yields to EM risks. A VaR shock, as experienced in previous instances of specific EM stress, is possible. Like the Russia-led VaR [shock in 2014], the contagion effect is driven by the need of real money investors to sell their holdings (even those with strong local fundamental stories) in other markets to fund redemptions, as indicated by discussions with EM real money investors, as well as by the strong historical relationship between global EM and specific EEMEA/LatAm/Asia dedicated funds’ net flow data.

I'm feeling a bit deadpan on Friday, so let me just preempt any potential pushback from readers by saying that exactly none of the above is debatable. These simply are the dynamics at play and while you can quibble with the potential scope and severity of an unwind, you cannot argue that what's happening right now isn't happening or that it's not down to Fed tightening and the surging dollar colliding with the vulnerabilities engendered by nine years of accommodation in DM markets.

Nedbank’s Neel Heyenke and Mehul Daya have been two of the most vocal analysts this year when it comes to cautioning against the prospect of a dollar liquidity shortage leading to a further unwind across markets, and especially in EM. For their part, they believe deglobalization will exacerbate the situation. Their research has been getting more and more attention of late. For instance, it was featured in a Financial Times post on Thursday. I've been highlighting it over on my site all year long. Here's some interesting commentary from a special report Nedbank released earlier this month on this subject (more here):

Should global growth become less synchronized the US deficit will shrink. This will provide less USD into the global financial system resulting in a shortage of dollars. Tighter monetary policy from the Fed, a higher Fed funds rate and shrinking of the Fed’s balance sheet, will further slow down USD creation.

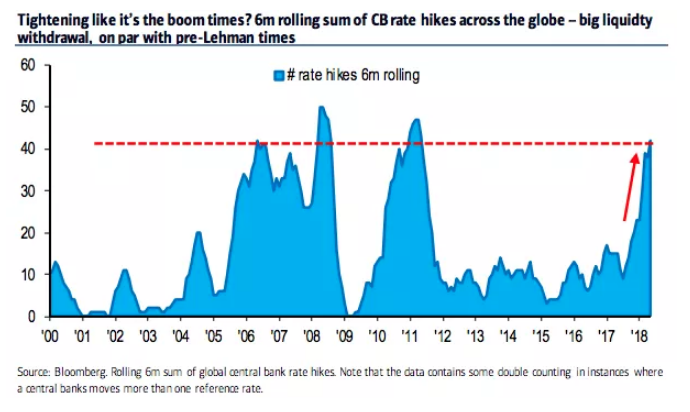

One way to protect yourself if you're an EM central banker is to hike rates, but the self-defeating nature of that in an environment where global growth seems to have peaked and trade frictions threaten to dent the prospects further, should be obvious. You can hike to protect the currency and guard against capital flight, but that risks undercutting domestic economic conditions and also has the potential to drive local stock prices lower. Worse, it actually contributes to the same tightening of global financial conditions that caused the problem in the first place. Here's a helpful excerpt on that from a note out last week by BofAML's Barnaby Martin:

The orthodox response to EM currency stress is central bank rate hikes. But this will serve to exacerbate the Fed-inspired liquidity drain already at work across markets. Note that year-to-date, the number of central bank rate hikes across the globe has shot up, and the pace is now almost on par with the pre-Lehman peak. And with less liquidity comes less “crowding” by markets into risky assets. Thus, investors should prepare for an ongoing period of high performance dispersion and idiosyncratic risk, in our view.

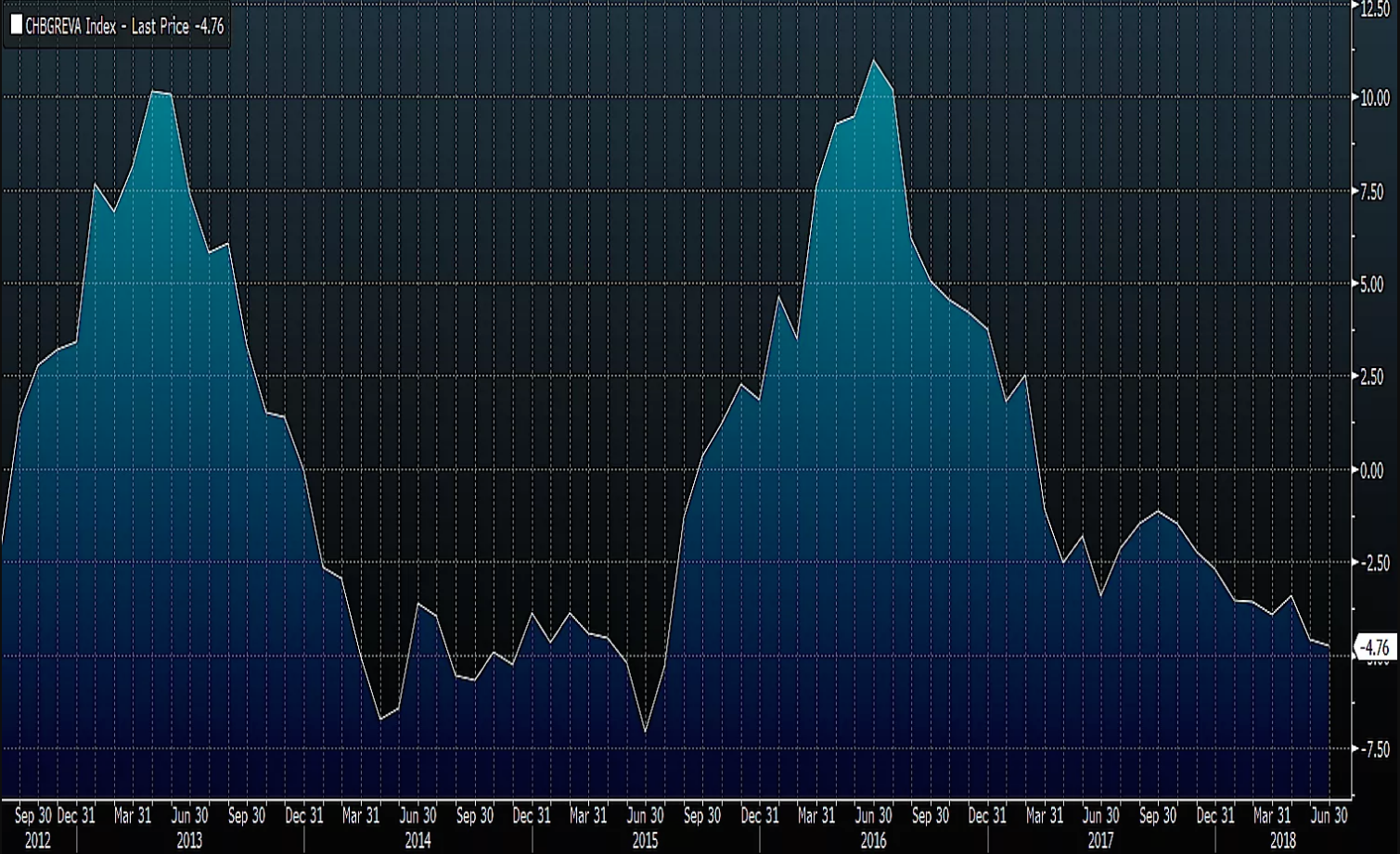

And it's not just Fed tightening or tentative normalization from other DM central banks (e.g., the ECB winding down its asset purchase program) that's at play when it comes to the liquidity tide receding. Credit creation in China is a key piece of the macro puzzle and as Citi’s Matt King recently noted, a slowdown there “is being reflected not only in directly affected variables like Chinese fixed asset investment but also in the rise in global volatility.”

Here's a look at Bloomberg's China credit impulse index (it's basically just new credit as a percentage of GDP):

(Source: Bloomberg)

(Source: Bloomberg)

If you lose the China credit impulse at the same time that DM central banks turn off the liquidity spigot, it's trouble.

For all of the reasons above, the dollar rally needed to abate. I went over that extensively on Wednesday in the post linked here at the outset. Donald Trump's criticism of the Fed (as published by Reuters on Monday) was thus a welcome development for global risk sentiment.

The question, though, was whether Jerome Powell would effectively negate that by saying something overly hawkish on Friday in his closely-watched speech in Jackson Hole.

Well, at around 7:00 AM ET (so, three hours prior to Powell's speech), the PBoC announced that it would be bringing back the counter-cyclical adjustment factor (hereafter "CCAF") in the yuan (CYB) fix. Regular readers are familiar with this. If you need a refresher course on the CCAF, you can find the history of it here, but suffice to say it's yet another tool the PBoC has at its disposal when it comes to ensuring the currency doesn't careen too far one way or another (i.e., weaker or stronger).

The reintroduction of the CCAF (which basically just means the central bank called banks that contribute to the daily fixing and informed them to start using it again) is the fourth measure taken this month aimed at ensuring the yuan doesn't hit the psychologically important 7-handle. The other three measures were: the reinstatement of forwards rules on August 3, the chiding of onshore banks for selling RMB on August 7, and a move to squeeze offshore liquidity on August 16. Here's an annotated chart of the onshore yuan going back to the 2015 devaluation:

(Source: Heisenberg)

(Source: Heisenberg)

Fast forward three hours from the PBoC news and Powell struck a reasonably dovish tone in Wyoming. Specifically, these were the key soundbites from his Jackson Hole speech:

While inflation has recently moved up near 2 percent, we have seen no clear sign of an acceleration above 2 percent, and there does not seem to be an elevated risk of overheating.

That's as dovish as you're going to get from Powell, given the current economic backdrop.

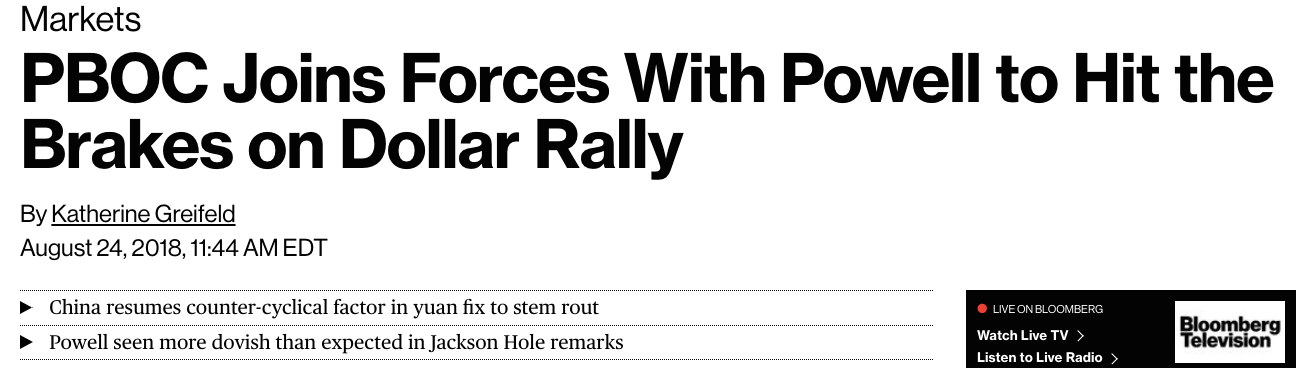

While I'm not one to posit conspiracy theories, it certainly is convenient that Powell avoided being hawkish and the PBoC brought back the CCAF in the same morning. It's even more convenient that this comes during a week that found Donald Trump expressing more concerns about the strength of the dollar and also featured a low-level meeting in Washington between U.S. and Chinese trade representatives.

And look, I'm not the only one suggesting that this was likely some semblance of coordinated.

Here's a screengrab from a feature Bloomberg article out Friday:

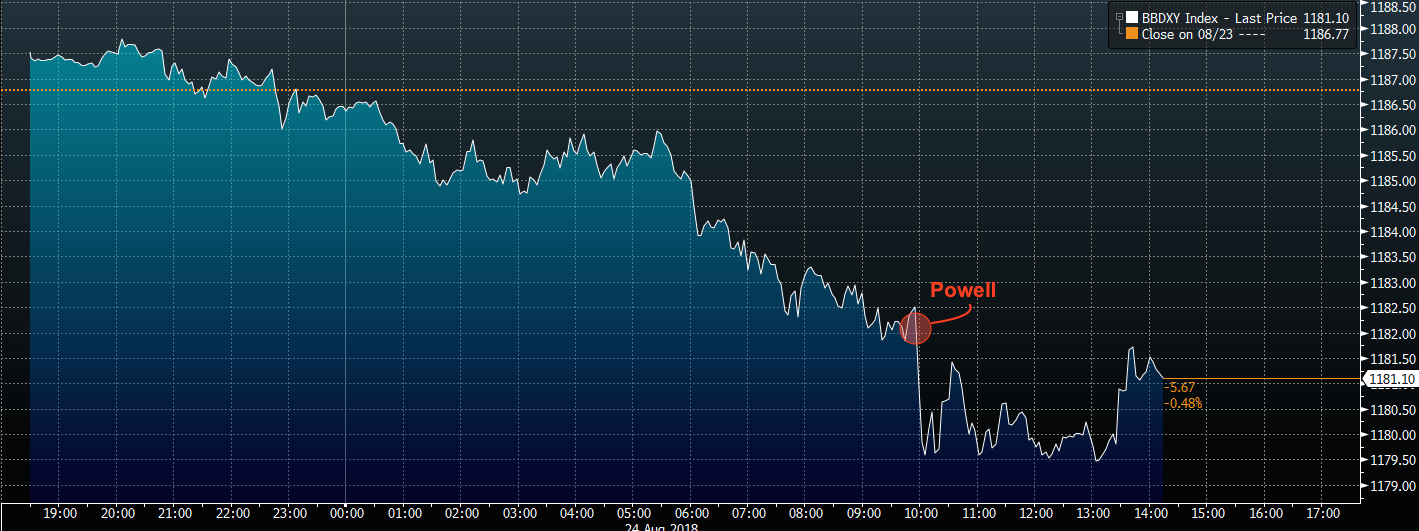

At one point, the Bloomberg dollar index was down some 0.6%.

(Source: Bloomberg)

(Source: Bloomberg)

That largely negated Thursday's gains and putting the greenback on track for its largest weekly decline since the week ended July 6.

(Source: Bloomberg)

(Source: Bloomberg)

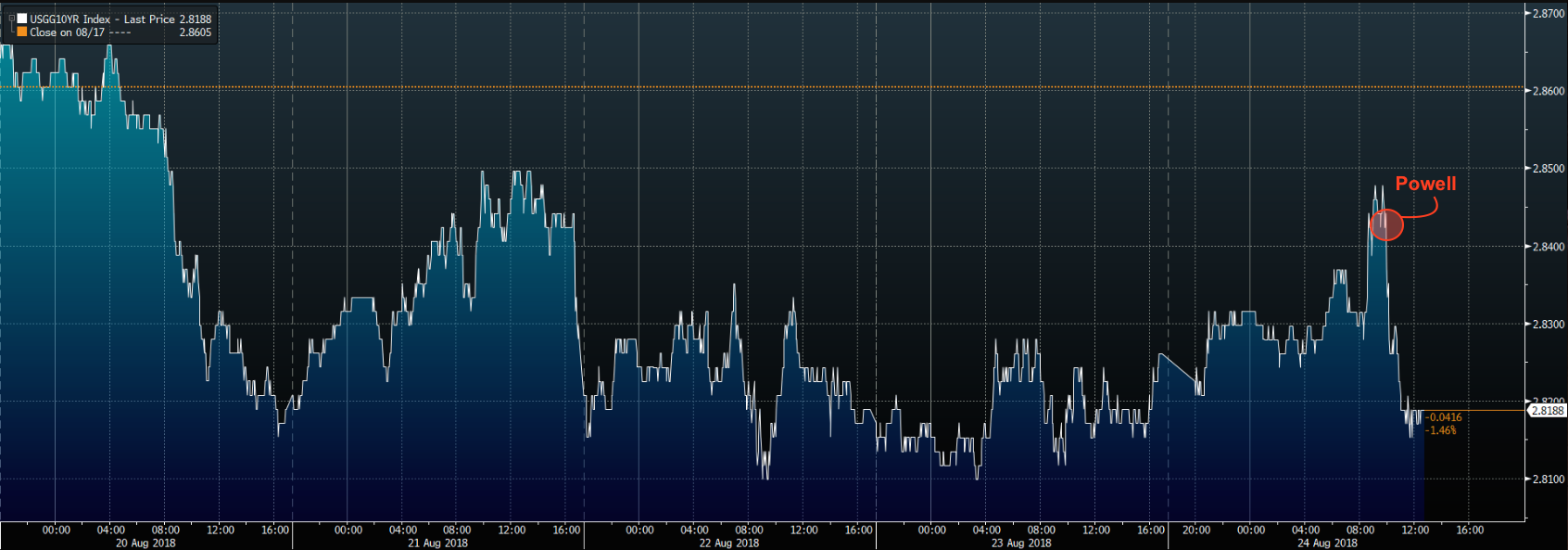

You're reminded that positioning in the dollar is extremely stretched. By that, I mean net long to the tune of $24.3 billion overall, the most since January 2017. That position is ripe for an unwind, as is the record spec short in the 10Y Treasury. As a reminder, the net non-commercial short in the 10Y increased to a record 698,194 contracts in the week through last Tuesday.

(Source: Bloomberg)

(Source: Bloomberg)

A dovish Powell has the potential to squeeze that short - just ask Jeff Gundlach, who said as much on Twitter last Friday. Sure enough, yields snapped lower on the Fed chair's speech, as Treasurys pared early losses. As of this writing, 10Y yields are down ~4bps on the week.

(Source: Bloomberg)

(Source: Bloomberg)

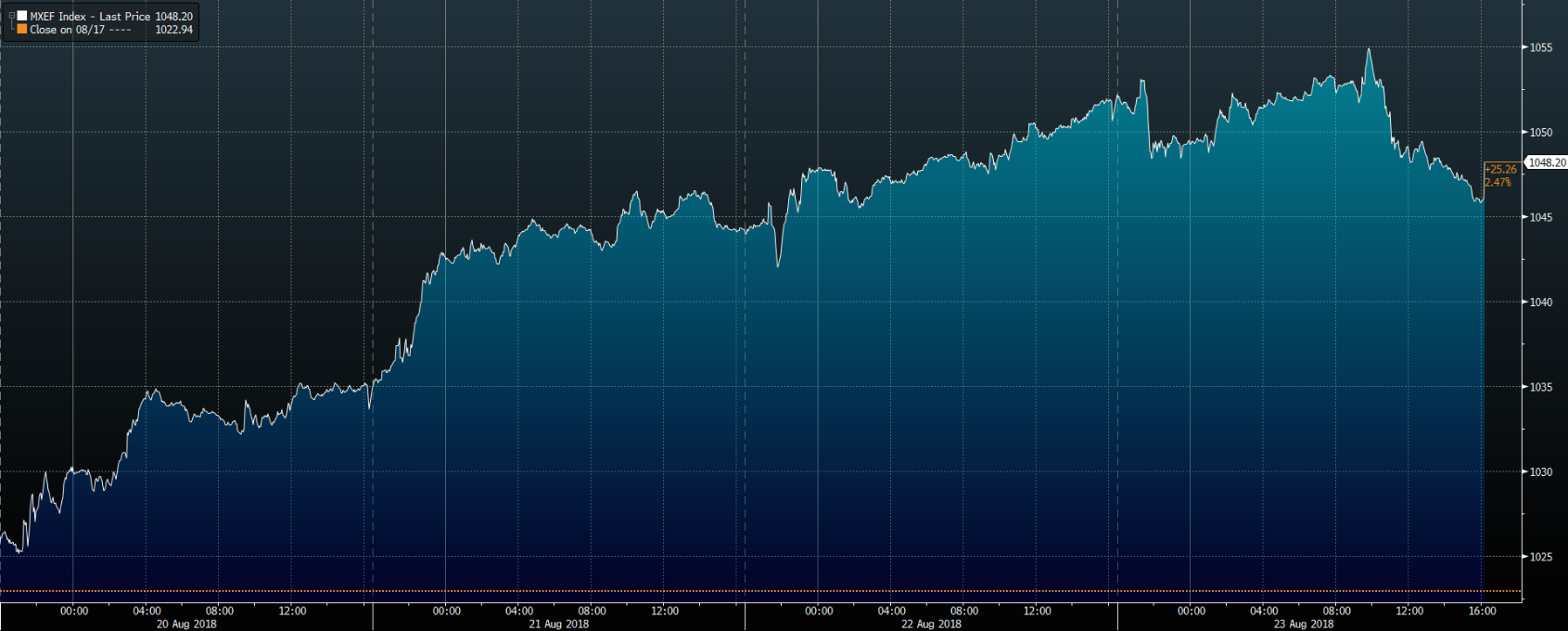

Again, this is welcome news for EM and for risk more generally. EM equities (NYSEARCA:EEM) are up nicely on the week and extended gains Friday amid the slump in the dollar.

(Source: Bloomberg)

(Source: Bloomberg)

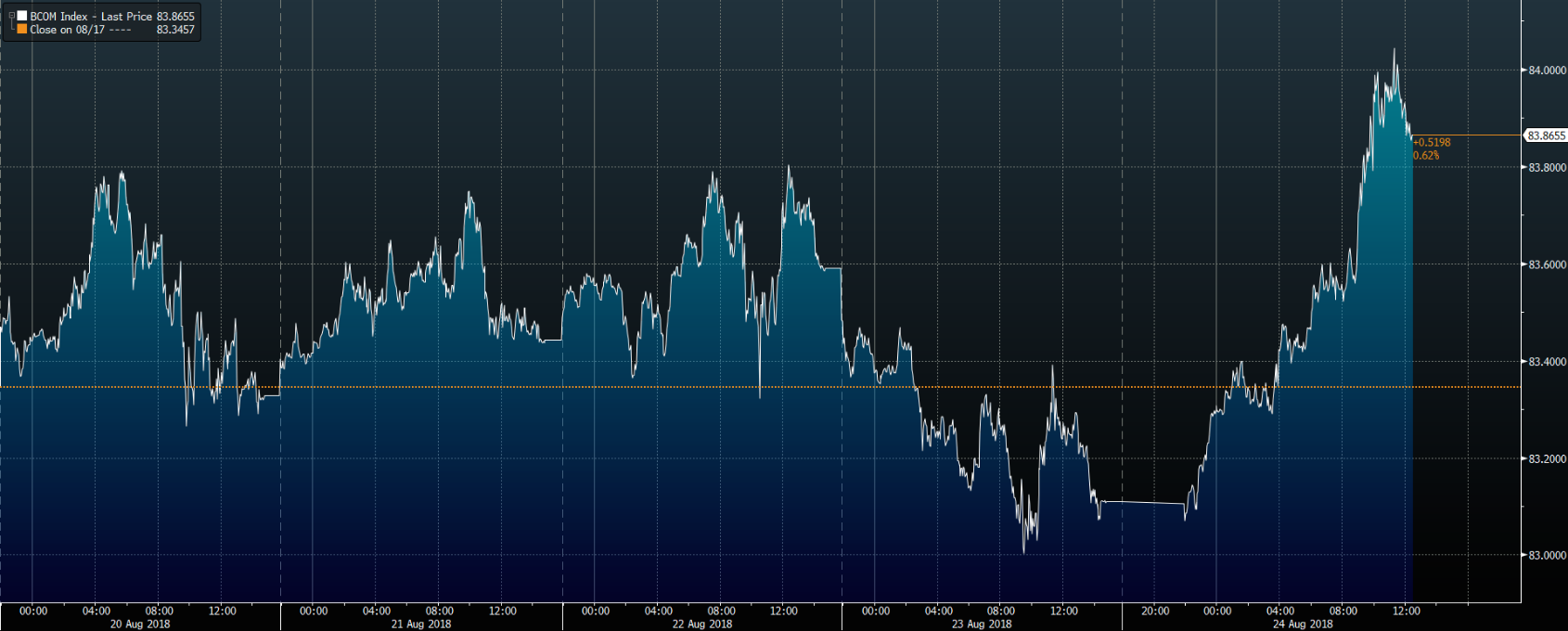

Meanwhile, commodities erased Thursday's losses and then some, extending gains as soon as Powell's comments hit the tape.

(Source: Bloomberg)

(Source: Bloomberg)

You get the idea. Do remember that a recovery in global risk sentiment will likely be key to preserving the rally in U.S. stocks (SPY) going forward.

So far in 2018, Wall Street has managed to shake off losses incurred around the globe thanks in no small part to the effects of late-cycle stimulus (e.g., record earnings and the buyback bonanza). If those effects fade (and you don't have to be a bear or a pessimist to know that they will), then U.S. shares will no longer be inoculated from the global risk-off environment. That's why it's key that the dollar doesn't resume its ascent in the month ahead.

You'll want to watch the latest CFTC data out this evening for signs that this week's action caused an unwind in either the dollar long or the spec short in the long-end of the curve. If those positions weren't shaken out by Tuesday, it would speak to just how convinced market participants are about the durability of the dollar rally, as the data will capture Monday's comments from Trump about Fed policy.

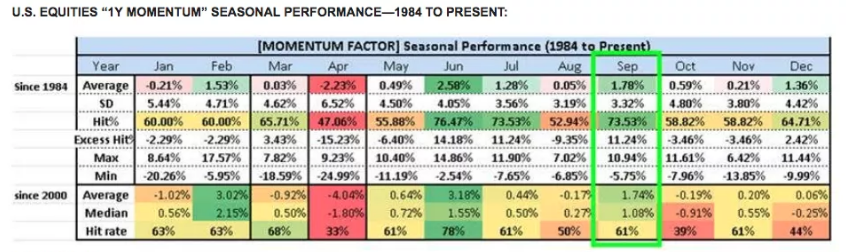

Meanwhile, for those of you who might be inclined to bet on a resumption of the trades that have been working for U.S. equity funds (i.e., long momentum/growth and short value), the above-mentioned Charlie McElligott thinks the stage is set for a "monster" momentum rally in September. That's a call based on seasonality:

(Source: Nomura)

(Source: Nomura)

But be careful, because that prediction came with a caveat which serves as the perfect way to end this post.

After September, McElligott thinks things might get dicey again. His reasoning: a resumption of the tightening in financial conditions catalyzed by ongoing QT and the possibility that the slowdown in the Chinese credit impulse bleeds over into growth proxies.

With that, I'll leave you with a quote from Charlie's Friday missive:

My call to get long U.S. Equities “1Y Momentum” into September is going bonkers in the best of fashions—the Nomura Momentum Factor is now +3.1% in two sessions.

Finally to reiterate, I DO then believe that following this Equities burst into September that we will see reinvigorated October cross-asset volatility. The macro-catalyst being the “QT escalation” theme I’ve been speaking to leading to potential interest rate volatility / tantrums. I too expect high-potential for position asymmetry to tip-over, as both systematic- and fundamental- investors accumulate leverage and large position size via lower realized volatility into the risk rally.

0 comments:

Publicar un comentario