The 800-pound gorilla effect

Donald Trump is sending shockwaves through global commodities markets

Possible sanctions on Iran and Venezuela are the next big threat

THE notion that the gentle flap of a butterfly’s wings can cause chaos on the other side of the world is well known. But commodity markets have been tested in recent weeks by what could be called the 800-pound-gorilla effect: the idea that chest-beating in the White House can unleash turmoil in global metals, agricultural and energy markets.

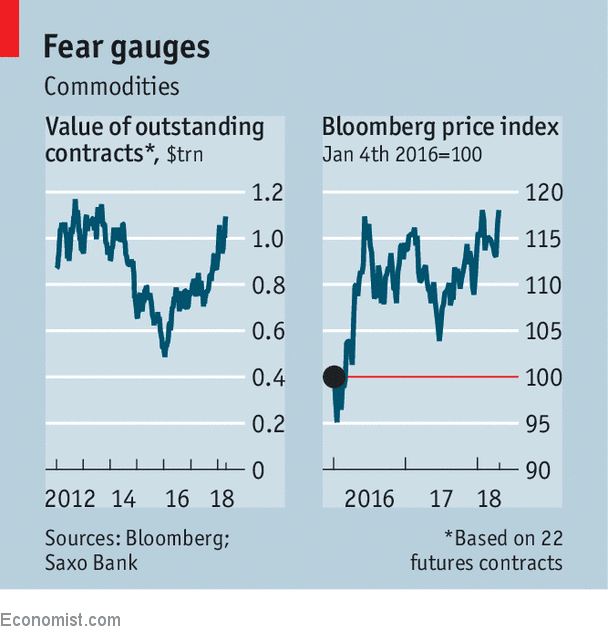

President Donald Trump has slapped sanctions on Russia’s biggest aluminium producer, Rusal, intensified a trade tiff with China and tweeted a gibe against OPEC, the oil-producing cartel. His actions have shaken commodity markets at a time when speculation in futures is near the record heights of 2012, making markets even more volatile (see chart). Aluminium, nickel and palladium prices have soared and then plummeted. Soyabean markets are under threat. Oil prices are at their highest levels for more than three years.

Physical trade has been affected too, with some shipments to Rusal of bauxite and alumina, the raw materials of aluminium, suspended for fear of sanctions-busting, and cargoes of American sorghum to China diverted in mid-ocean because of Chinese trade restrictions. Pushing oil prices yet higher is the possibility that Mr Trump could impose sanctions on oil shipped from Iran and Venezuela next month, tightening the global supply of crude just as America’s summer driving season starts. Geopolitics has often upset global trade in commodities. But rarely has America’s government been such a source of upheaval across so many markets.

Metals have suffered most directly. From April 6th, when America’s Treasury prohibited Americans from dealing with Rusal and its boss, Oleg Deripaska, and threatened sanctions against non-citizens who traded with them, aluminium prices rose by more than 30% as buyers scrambled for non-Russian metals. Then on April 23rd, when the Treasury temporarily softened the proposed sanctions to spare “the hardworking people” of Rusal and its subsidiaries, and said it might lift them on Rusal if Mr Deripaska ceded control, they gave up around half of those gains.

Nickel prices also soared until April 19th on expectations the sanctions could extend to Norilsk Nickel, a Russian producer. José Cogolludo, global head of commodities at Citi, notes bashfully that shortly before the sanctions-related rally, the bank had been telling investors that nickel prices would hit $16,000 a tonne by 2020. They reached $17,000 in days—before falling back when the sanctions were eased.

Mr Cogolludo says that hedging of metals reached unprecedented levels as corporate clients sought to protect themselves during the price moves and speculators tried to cover short positions. He adds that computer-driven models, which account for most speculative activity in metals markets, respond quickly to market signals but are rarely good at deciphering geopolitical risk. This may have led to overshooting.

Agricultural commodities have suffered collateral damage from trade tensions between America and China. After the Trump administration imposed tariffs on steel and aluminium imports in March, in mid-April China announced a 179% preliminary anti-dumping duty on imports of American sorghum, a niche animal feed. This stopped American exports, which account for almost all sorghum entering China, in their tracks.

More significantly, China responded to an American proposal in April to slap 25% tariffs on 1,300 goods from China by threatening similar levies on 106 American imports, including soyabeans and cotton. According to Stefan Vogel of Rabobank, 35% of China’s 97m tonnes of soyabean imports come from America, which are not easily replaceable. So the market is betting that China will not carry out its threats. But if traders are wrong, and a tariff war breaks out in earnest this summer, the disruption could be severe. He says prices of soyabeans in America would plummet. Those of soyabeans in South America, spared the Chinese tariffs, could soar.

Some say that Mr Trump is showing a pattern of making threats and then backtracking, which creates noise but does little lasting damage. That view may be tested in the oil markets on May 12th. The president has threatened to reintroduce sanctions on Iran unless Britain, France and Germany agree to renegotiate the Iranian nuclear deal by then.

Some oil bulls say Mr Trump’s nomination of Mike Pompeo as secretary of state and his appointment of John Bolton as national security adviser—both Iran hawks—have made sanctions likelier. These could remove at least 500,000 barrels a day of Iranian oil from a market that is already looking tighter because OPEC and non-OPEC producers have restrained output. Abhishek Deshpande, head of oil research at J.P. Morgan, says such sanctions could raise average annual oil prices by about $10 a barrel (Brent crude has been trading near $75). Additional measures threatened against Venezuela if elections on May 20th are not free and fair could squeeze the market yet more.

But Bob McNally of Rapidan Energy Group, a consultancy, argues that the impact of higher petrol prices on American drivers may persuade Mr Trump to accept compromises on Iran and Venezuela. Nerves ahead of mid-term elections, he reckons, explain the president’s first tweet aimed at OPEC. On April 20th Mr Trump blamed the cartel for “artificially very high” prices—although high prices are also a windfall for American shale producers.

OPEC ministers, disturbed by the tweet while at a birthday party in Jeddah for the organisation’s secretary-general, Muhammad Barkindo, were not conciliatory. They claimed, however implausibly, that they were not trying to rig oil prices. But they should beware taking Mr Trump’s ability to mess with the markets too lightly. With bullish bets on oil prices near record highs, it would not take much to trigger a sharp reversal. Just ask metals traders: the 800-pound gorilla can trash prices as well as push them up.

0 comments:

Publicar un comentario