Sell the Swiss Franc if You Think the World Is a Better Place

Swiss franc proved slow to react to the brighter picture for the eurozone economy

By Richard Barley

SAFETY TRADE

How many euros one Swiss franc buys

For all of the controversy around aggressive monetary policy, there is little dispute that central bankers have succeeded in moving the values of stocks, bonds and currencies. The exception that proves the rule is the Swiss franc.

The Swiss National Bank has tried hard to battle the strength of its currency but where other central banks had big impacts, the Swiss franc has refused to fall. The central bank has gone deep into negative-interest-rate territory, taking its target rate to minus 0.75%. For four years it put an outright cap on appreciation against the euro, printing francs and buying foreign assets in a campaign that has taken its balance sheet to more than 100% of Switzerland’s gross domestic product.

The SNB’s cap did temporarily turn the Swiss franc around, but the chaos sparked by its January 2015 decision to abandon that policy still hasn’t fully reversed. On a trade-weighted basis and adjusted for inflation, the Swiss franc is still some 12% higher than its precrisis average, SNB data show. Against the euro, the franc has fallen 6% this year but is still stronger than the level the SNB targeted before January 2015.

The SNB’s efforts to weaken the franc have been overwhelmed by the actions of its much bigger neighbor, the European Central Bank. But now the ECB is gradually moving away from quantitative easing as the eurozone economy picks up.

On the Swiss side, extremely low inflation means the central bank has absolutely no reason to shift its policy. Annual inflation has only been above zero in 12 of the 67 months since the start of 2012 and has often been below that of Japan. The SNB forecasts inflation at 0.3% in 2018 and 1% in 2019.

The combination of weak inflation and loose monetary policy in Switzerland and stronger growth and less quantitative easing in Europe argues for the franc to weaken versus the euro.

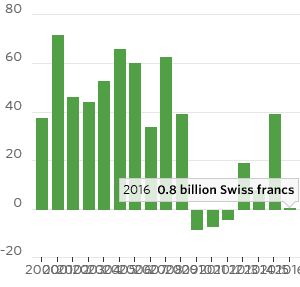

The other factor pushing for a weaker franc is the improving prospects for the eurozone. Fear of the currency bloc breaking up benefits the franc. Swiss outward investment flows, much of which traditionally landed in the eurozone, have collapsed since the crisis. As those fears fade, so should the franc. The first time the Swiss franc showed signs of weakening this year was in the wake of the French elections, won by the staunchly pro-Europe Emmanuel Macron. A resumption of Swiss investment flows—which means investors sell francs and buy euros—could be a key factor in the franc’s path.

INTERRUPTED

Swiss residents net investments in foreign securities

Change in consumer prices from a year earlier

The Swiss franc won’t stop being a haven. When risk aversion rises, investors seem hard-wired to embrace it. Italian elections next year could be a flashpoint. But unless there is a specific threat to eurozone cohesion, such reversals shouldn’t prove too disruptive.

Put together, that makes the Swiss franc a sell against the euro. Even if the franc falls from its current €0.875 to €0.83, a big move in currencies, it would only be at the highest level that the Swiss central bank allowed it to go in 2015. A further decline would make those bankers happier. Investors should go along for the ride.

0 comments:

Publicar un comentario