Economic Forecast: Theories Behind The Numbers

by: Dr. Bill Conerly

What's the theory behind my economic forecast? In simple language, it's complicated. My forecast is judgmental rather than coming from an econometric model. I begin with a "bottoms-up" prediction of major sectors, followed by a top-down reality-check. This article will explain my basic economic thought process.

The classical economists are in the back of my mind. They viewed the economy as self-regulating. The Pigou effect is one part of the process, but not the only one. I certainly believe we would have business cycles even in the absence of bad government policy, but I think the classicals were right that if the government took their hands off the levers of policy, the economy would come back to full employment. My judgment is that the speed of adjustment would be fairly rapid, but the slow-adjustment argument is worth considering.

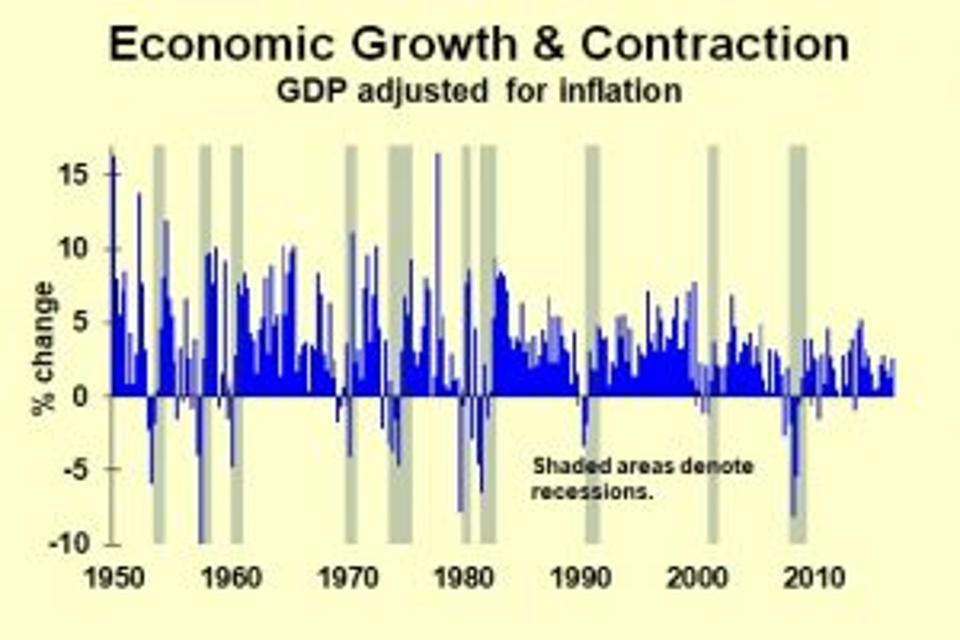

Dr. Bill Conerly with data from Bureau of Economic Analysis

Economic Growth and Contraction

I read John Maynard Keynes' General Theory as a skeptical undergraduate, but I really took to it after reading Axel Leijonhufvud's splendid On Keynesian Economics and the Economics of Keynes. He said that textbook Keynesian economics had become mechanical, losing some key points. I took away two lessons. The first is that the basis for many spending decisions is soft.

We can teach MBA students how to find the optimum capital expenditure, but the calculations are based on a host of unknowns: future prices and future costs and future interest rates. The second lesson is that in an environment of unknowns, decision-makers often take on a herd mentality, leading to swings of optimism and pessimism. When forecasting business decisions, I look at the fundamental factors that should be driving capital spending, but I also recognize the possibility of these mood swings.

The monetarism of Milton Friedman and others heavily influenced me early in my career. I'm less a monetarist now, partly because it's so hard to find a measure of money supply for which demand is fairly stable. Nonetheless, I take monetary policy to be powerful, but not completely determinative for the economy.

"Real business cycle" theory shows that swings in new technology development can trigger booms and busts. For their work on this, Finn Kydland and Edward Prescott were awarded the Nobel prize in economics. Read the prize description for more about their work at the layman's level. When the tech sector develops new business models, there can certainly be a boost to capital spending - so long as the technology does not reduce the need for capital in total. I keep this in mind, but most of my effort focuses on other areas.

The dominant macroeconomic theory today is "new Keynesian," which emphasizes the business cycle consequences of market imperfections, such as wages and prices that adjust to new circumstances only gradually. I take this seriously, though with the proviso that when it is profitable to change wages and prices more quickly, that will happen.

That idea brings us to rational expectations, the notion that people make decisions using all of the information available to them. The idea is frequently criticized, even to the point of being laughed at, but let's state it a different way: You can't fool all the people all the time. Robert Lucas argues that economic policy which depended on tricking people would not long work.

Think of government spending to stimulate the economy. The stimulus comes only if people do not boost their savings so that they can pay a future tax bill. As more and more people worry about the federal debt burden, I think that policy is less effective.

I'm often asked about Austrian business cycle theory, which I studied both as an undergraduate and in my Ph.D. program at Duke. The simplistic version of this theory is that easy money policy from the Federal Reserve (or other central bank) causes more capital spending and more roundabout production processes than is warranted by the underlying productivity of capital and consumer time preference. Eventually, the misallocation of resources is corrected, resulting in a recession or depression. The downturn is necessary to correct the errors of the past. Although there are many insights from the Austrian school that I use regularly, I find the specifics of the business cycle theory less useful.

I also find a good bit of overlap between the economics of Keynes, with its emphasis on decision-making under uncertainty, and the Austrian view. This seems odd to those who see Keynesians as proponents of activist government and Austrians as opponents. The two schools are united in their emphasis on decision-making under uncertainty. (Although Hayek and Keynes are sometimes portrayed as antagonists, they were cordial colleagues. During World War II they walked the streets of Cambridge together as air wardens, checking that blackout curtains were in place.)

My economic theory is a mongrel, using a variety of insights developed by different theorists.

The most important basis is old-fashioned supply and demand, applied to different sectors of the economy. For instance, when I look at consumer spending on durables goods such as cars, I examine incomes and whether there might be pent-up demand. When business spending is surging, I'm concerned about supply-chain limitations.

In practice, forecasting is heavily judgmental. Some folks have computer models that they let run on autopilot. But each model is based on judgements about what factors to include and what to ignore.

The world is too complicated - and data too limited - to utilize all possible explanatory factors, so economists pick and choose. Whether with a computer model or a purely judgmental process, the economist makes his best guess in an atmosphere of uncertainty.

0 comments:

Publicar un comentario