Buttonwood

Getting the most out of business taxes

Changing rates does not make a lot of difference

ONE of the hottest debates in economic policy at the moment is how to ensure companies are paying the optimal amount of tax. On the right, politicians think that a lower corporate-tax rate will lead to more business investment and thus faster economic growth. Hence the initial stockmarket enthusiasm after President Donald Trump was elected on a platform that included cuts in business taxes. On the left, the belief is that business is not paying its “fair share” of tax and that it can be further squeezed to pay for spending commitments. Hence the promise of the Labour Party in Britain’s recent election campaign to push the corporate-tax rate up to 26% (from 19%).

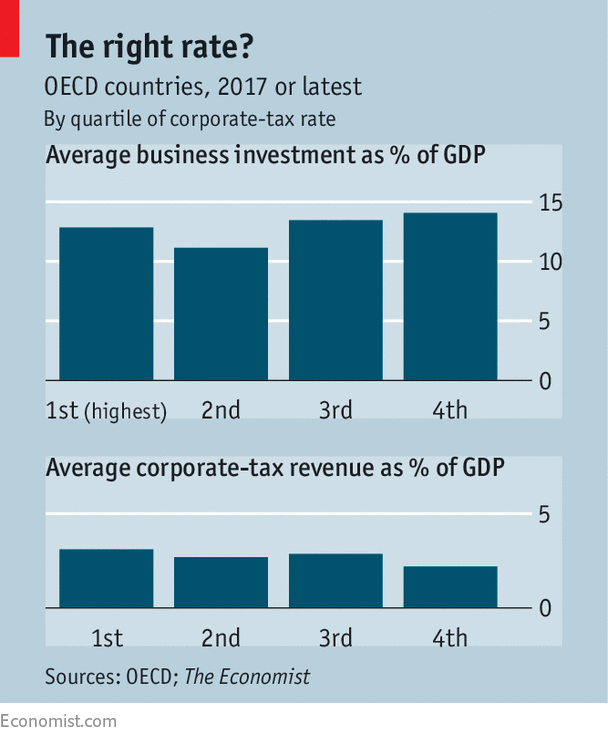

How do these theories translate into practice? To find out the effect on business investment, The Economist took the corporate-tax rates in OECD countries and divided them into quartiles from highest (1st) to lowest. Then we calculated the five-year average in each quartile for gross fixed capital formation as a share of GDP.

Independent of their tax rates, for example, South Korean and Turkish companies are investing a lot. Perhaps they are catching up with mature economies, perhaps they are over-investing.

What about the tax take? The picture is complicated here, too. Lower tax rates may just work by pinching revenues from other countries. For example, Ireland, with a 12.5% rate, earns a higher proportion of GDP in revenues than France, at 34.4%. And the headline tax rate may not be decisive.

Countries with high rates (like America) tend to offset them with allowances and deductions that bring down the effective rate that companies pay.

The idea of using tax levels to boost revenues does not get much support, either. Most countries sit within the 2-3%-of-GDP range (see bottom chart). The countries with the lowest corporate-tax rates receive a bit less in taxes. But the difference between the top and bottom quartiles is only 0.9% of GDP. Grabbing this extra chunk might be useful revenue, but when public spending is 40% of GDP or so, other sources of funding are a lot more important.

Two other things are worth remembering. The first is that companies are merely legal entities.

To the extent they pay more taxes, they must get the money to do so from elsewhere. Politicians on the left think the money comes from shareholders. But it is not as simple as that (and even if it were, those shareholders may represent the pension funds of citizens). For instance, a large company might not want to reduce the profits it pays out to shareholders for fear of becoming a takeover target. So it could move some of its operations to a lower-tax regime. Or it could recoup the loss by charging consumers more, or by paying workers less.

Second, countries do not just want to attract businesses for the taxes they pay but for the workers they employ and for the extra revenues they create for local suppliers. The effective tax take firms generate (on wages, sales and property taxes) is much higher than the tax on profits alone. So there are dangers in driving business away, something Britain needs to contemplate after the Brexit vote.

Some argue that the profits tax should be abolished. Governments should look through the corporate structure and tax shareholders directly. The problem is that many shareholders, such as pension funds and charities, are tax-exempt, and others are based in low-tax regimes.

That would also create incentives for individuals to incorporate to cut their tax bills. So such a move should await much more sweeping tax reform. In the meantime, governments will have to make do with what they currently get. There is no magic trick for collecting a lot more.

0 comments:

Publicar un comentario