Contemporary criticisms of central banks echo debates from times past

TWENTY years ago next month, the British government gave the Bank of England the freedom to set interest rates. That decision was part of a trend that made central bankers the most powerful financial actors on the planet, not only setting rates but also buying trillions of dollars’ worth of assets, targeting exchange rates and managing the economic cycle.

Although central banks have great independence now, the tide could turn again. Central bankers across the world have been criticised for overstepping their brief, having opined about broader issues (the Reserve Bank of India’s Raghuram Rajan on religious tolerance, the Bank of England’s Mark Carney on climate change). In some countries the fundamentals of monetary policy are under attack: Recep Tayyip Erdogan, the president of Turkey, has berated his central bank because of his belief that higher interest rates cause inflation. And central banks have been widely slated for propping up the financial sector, and denting savers’ incomes, in the wake of the financial crisis of 2007-08.

Such debate is almost as old as central banking itself. Over more than 300 years, the power of central banks has ebbed and flowed as governments have by turns enhanced and restricted their responsibilities in response to economic necessity and intellectual fashion. Governments have asked central banks to pursue several goals at once: stabilising currencies; fighting inflation; safeguarding the financial system; co-ordinating policy with other countries; and reviving economies.

These goals are complex and not always complementary; it makes sense to put experts in charge.

That said, the actions needed to attain them have political consequences, dragging central banks into the democratic debate. In the early decades after American independence, two central banks were founded and folded before the Federal Reserve was established in 1913. Central banks’ part in the Depression of the 1930s, the inflationary era of the 1960s and 1970s and the credit bubble in the early 2000s all came under attack.

Bankers to the government

The first central banks were created to enhance the financial power of governments. The pioneer was the Sveriges Riksbank, set up as a tool of Swedish financial management in 1668 (the celebration of its tercentenary included the creation of the Nobel prize in economics). But the template was set by the Bank of England, established in 1694 by William III, ruler of both Britain and the Netherlands, in the midst of a war against France. In return for a loan to the crown, the bank gained the right to issue banknotes. Monarchs had always been prone to default—and had the power to prevent creditors from enforcing their rights. But William depended on the support of Parliament, which reflected the interests of those who financed the central bank. The creation of the bank reassured creditors and made it easier and cheaper for the government to borrow.

No one at the time expected these central banks to evolve into the all-powerful institutions of today. But a hint of what was to come lay in the infamous schemes of John Law in France from 1716 to 1720. He persuaded the regent (the king, Louis XV, was an infant) to allow him to establish a national bank, and to decree that all taxes and revenues be paid in its notes. The idea was to relieve the pressure on the indebted monarchy. The bank then assumed the national debt; investors were persuaded to swap the bonds for shares in the Mississippi company, which would exploit France’s American possessions.

One of the earliest speculative manias ensued: the word “millionaire” was coined as the Mississippi shares soared in price. But there were no profits to be had from the colonies and when Law’s schemes collapsed, French citizens developed an enduring suspicion of high finance and paper money. Despite this failure, Law was on to something.

Paper money was a more useful medium of exchange than gold or silver, particularly for large amounts. Private banks might issue notes but they were less trustworthy than those printed by a national bank, backed by a government with tax-raising powers. Because paper money was a handier medium of exchange, people had more chance to trade; and as economic activity grew, government finances improved. Governments also noticed that issuing money for more than its intrinsic value was a nice little earner.

Alexander Hamilton, America’s first treasury secretary, admired Britain’s financial system.

Finances were chaotic in the aftermath of independence: America’s first currency, the Continental, was afflicted by hyperinflation. Hamilton believed that a reformed financial structure, including a central bank, would create a stable currency and a lower cost of debt, making it easier for the economy to flourish.

His opponents argued that the bank would be too powerful and would act on behalf of northern creditors. In “Hamilton”, a hit hip-hop musical, the Thomas Jefferson character declares: “But Hamilton forgets/His plan would have the government assume state’s debts/Now, place your bets as to who that benefits/The very seat of government where Hamilton sits.”

Central banking was one of the great controversies of the new republic’s first half-century.

Hamilton’s bank lasted 20 years, until its charter was allowed to lapse in 1811. A second bank was set up in 1816, but it too was resented by many. Andrew Jackson, a populist president, vetoed the renewal of its charter in 1836.

Good as gold

A suspicion that central banks were likely to favour creditors over debtors was not foolish.

Britain had moved onto the gold standard, by accident, after the Royal Mint set the value of gold, relative to silver, higher than it was abroad at around the turn of the 18th century, and silver flowed overseas. Since Bank of England notes could be exchanged on demand for gold, the bank was in effect committed to maintaining the value of its notes relative to the metal.

By extension, this meant the bank was committed to the stability of sterling as a currency. In turn, the real value of creditors’ assets (bonds and loans) was maintained; on the other side, borrowers had no prospect of seeing debts inflated away.

Gold convertibility was suspended during the Napoleonic wars: government debt and inflation soared. Parliament restored it in 1819, although only by forcing a period of deflation and recession. For the rest of the century, the bank maintained the gold standard with the result that prices barely budged over the long term. But the corollary was that the bank had to raise interest rates to attract foreign capital whenever its gold reserves started to fall. In effect, this loaded the burden of economic adjustment onto workers, through lower wages or higher unemployment. The order of priorities was hardly a surprise when voting was limited to men of property. It was a fine time to be a rentier.

The 19th century saw the emergence of another responsibility for central banks: managing crises.

Capitalism has always been plagued by financial panics in which lenders lose confidence in the creditworthiness of private banks. Trade suffered at these moments as merchants lacked the ability to fund their purchases. In the panic of 1825 the British economy was described as being “within twenty-four hours of a state of barter.” After this crisis, the convention was established that the Bank of England act as “lender of last resort”. Walter Bagehot, an editor of The Economist, defined this doctrine in his book “Lombard Street”, published in 1873: the central bank should lend freely to solvent banks, which could provide collateral, at high rates.

The idea was not universally accepted; a former governor of the Bank of England called it “the most mischievous doctrine ever breathed in the monetary or banking world”. It also involved a potential conflict with a central bank’s other roles. Lending in a crisis meant expanding the money supply. But what if that coincided with a need to restrict the money supply in order to safeguard the currency?

As other countries industrialised in the 19th century, they copied aspects of the British model, including a central bank and the gold standard. That was the pattern in Germany after its unification in 1871.

America was eventually tipped into accepting another central bank by the financial panic of 1907, which was resolved only by the financial acumen of John Pierpont Morgan, the country’s leading banker. It seemed rational to create a lender of last resort that did not depend on one man. Getting a central bank through Congress meant assuaging the old fears of the “eastern money power”. Hence the Fed’s unwieldy structure of regional, privately owned banks and a central, politically appointed board. Ironically, no sooner had the Fed been created than the global financial structure was shattered by the first world war. Before 1914 central banks had co-operated to keep exchange rates stable. But war placed domestic needs well ahead of any international commitments. No central bank was willing to see gold leave the country and end up in enemy vaults. The Bank of England suspended the right of individuals to convert their notes into bullion; it has never been fully reinstated. In most countries, the war was largely financed by borrowing: central banks resumed their original role as financing arms of governments, and drummed up investor demand for war debt. Monetary expansion and rapid inflation followed.

Interwar failure

Reconstructing an international financial system after the war was complicated by the reparations imposed on Germany and by the debts owed to America by the allies. It was hard to co-ordinate policy amid squabbling over repayment schedules. When France and Belgium occupied the Ruhr in 1923 after Germany failed to make payments, the German central bank, the Reichsbank, increased its money-printing, unleashing hyperinflation. Germans have been wary of inflation and central-bank activism ever since.

The mark eventually stabilised and central banks tried to put a version of the gold standard back together. But two things hampered them. First, gold reserves were unevenly distributed, with America and France owning the lion’s share. Britain and Germany, which were less well endowed, were very vulnerable.

Second, European countries had become mass democracies, which made the austere policies needed to stabilise a currency in a crisis harder to push through. The political costs were too great. In Britain the Labour government fell in 1931 when it refused to enact benefit cuts demanded by the Bank of England. Its successor left the gold standard. In Germany Heinrich Brüning, chancellor from 1930 to 1932, slashed spending to deal with the country’s foreign debts but the resulting slump only paved the way for Adolf Hitler.

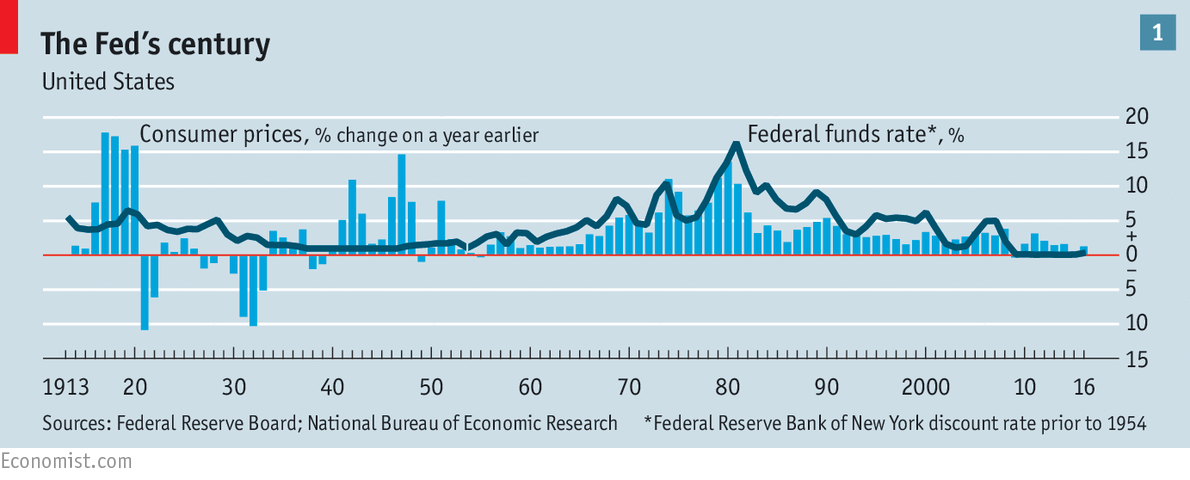

America was by then the most powerful economy, and the Fed the centrepiece of the interwar financial system (see chart 1). The central bank struggled to balance domestic and international duties. A rate cut in 1927 was designed to make life easier for the Bank of England, which was struggling to hold on to the gold peg it had readopted in 1925. But the cut was criticised for fuelling speculation on Wall Street. The Fed started tightening again in 1928 as the stockmarket kept booming. It may have overdone it.

If central banks struggled to cope in the 1920s, they did even worse in the 1930s. Fixated on exchange rates and inflation, they allowed the money supply to contract sharply. Between 1929 and 1933, 11,000 of America’s 25,000 banks disappeared, taking with them customers’ deposits and a source of lending for farms and firms. The Fed also tightened policy prematurely in 1937, creating another recession.

During the second world war central banks resumed their role from the first: keeping interest rates low and ensuring that governments could borrow to finance military spending. After the war, it became clear that politicians had no desire to see monetary policy tighten again. The result in America was a running battle between presidents and Fed chairmen. Harry Truman pressed William McChesney Martin, who ran the Fed from 1951 to 1970, to keep rates low despite the inflationary consequences of the Korean war. Martin refused. After Truman left office in 1953, he passed Martin in the street and uttered just one word: “Traitor.”

Lyndon Johnson was more forceful. He summoned Martin to his Texas ranch and bellowed: “Boys are dying in Vietnam and Bill Martin doesn’t care.” Typically, Richard Nixon took the bullying furthest, leaking a false story that Arthur Burns, Martin’s successor, was demanding a 50% pay rise. Attacked by the press, Burns retreated from his desire to raise interest rates.

In many other countries, finance ministries played the dominant role in deciding on interest rates, leaving central banks responsible for financial stability and maintaining exchange rates, which were fixed under the Bretton Woods regime. But like the gold standard, the system depended on governments’ willingness to subordinate domestic priorities to the exchange rate.

By 1971 Nixon was unwilling to bear this cost and the Bretton Woods system collapsed.

Currencies floated, inflation took off and worse still, many countries suffered high unemployment at the same time.

This crisis gave central banks the chance to develop the powers they hold today. Politicians had shown they could not be trusted with monetary discipline: they worried that tightening policy to head off inflation would alienate voters. Milton Friedman, a Chicago economist and Nobel laureate, led an intellectual shift in favour of free markets and controlling the growth of the money supply to keep inflation low. This “monetarist” approach was pursued by Paul Volcker, appointed to head the Fed in 1979. He raised interest rates so steeply that he prompted a recession and doomed Jimmy Carter’s presidential re-election bid in 1980. Farmers protested outside the Fed in Washington, DC; car dealers sent coffins containing the keys of unsold cars. But by the mid-1980s the inflationary spiral seemed to have been broken.

The rise to power

In the wake of Mr Volcker’s success, other countries moved towards making central banks more independent, starting with New Zealand in 1989. Britain and Japan followed suit. The European Central Bank (ECB) was independent from its birth in the 1990s, following the example of Germany’s Bundesbank. Many central bankers were asked to target inflation, and left to get on with the job. For a long while, this approach seemed to work perfectly. The period of low inflation and stable economies in the 1990s and early 2000s were known as the “Great Moderation”. Alan Greenspan, Mr Volcker’s successor, was dubbed the “maestro”. Rather than bully him, presidents sought his approbation for their policies.

Nevertheless, the seeds were being sown for today’s attacks on central banks. In the early 1980s financial markets began a long bull run as inflation fell. When markets wobbled, as they did on “Black Monday” in October 1987, the Fed was quick to slash rates. It was trying to avoid the mistakes of the 1930s, when it had been too slow to respond to financial distress. But over time the markets seemed to rely on the Fed stepping in to rescue them—a bet nicknamed the “Greenspan put”, after an option strategy that protects investors from losses. Critics said that central bankers were encouraging speculation.

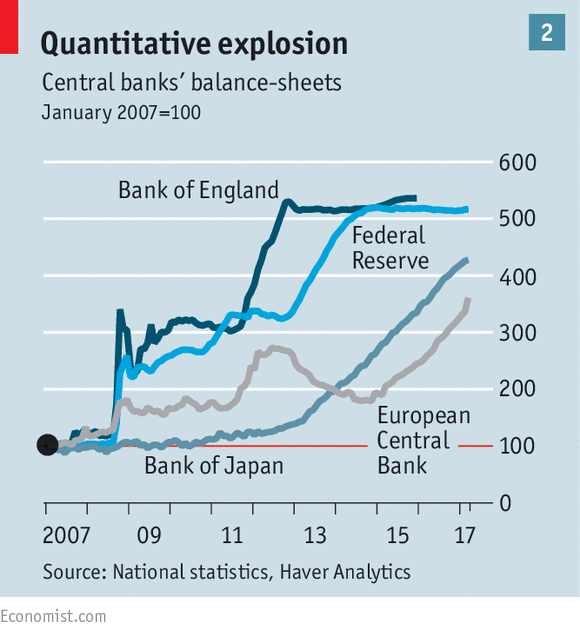

However, there was no sign that the rapid rise in asset prices was having an effect on consumer inflation. Raising interest rates to deter stockmarket speculation might inflict damage on the wider economy. And although central banks were supposed to ensure overall financial stability, supervision of individual banks was not always in their hands: the Fed shared responsibility with an alphabet soup of other agencies, for example. . When the credit bubble finally burst in 2007 and 2008, central banks were forced to take extraordinary measures: pushing rates down to zero (or even below) and creating money to buy bonds and crush long-term yields (quantitative easing, or QE: see chart 2). As governments tightened fiscal policy from 2010 onwards, it sometimes seemed that central banks were left to revive the global economy alone.

Their response to the crisis has called forth old criticisms. In an echo of Jefferson and Jackson, QE has been attacked for bailing out the banks rather than the heartland economy, for favouring Wall Street rather than Main Street. Some Republicans want the Fed to make policy by following set rules: they deem QE a form of printing money. The ECB has been criticised both for favouring northern European creditors over southern European debtors and for cosseting southern spendthrifts.

And central banks are still left struggling to cope with their many responsibilities. As watchdogs of financial stability, they want banks to have more capital. As guardians of the economy, many would like to see more lending. The two roles are not always easily reconciled.

Perhaps the most cutting criticism they face is that, despite their technocratic expertise, central banks have been repeatedly surprised. They failed to anticipate the collapse of 2007-08 or the euro zone’s debt crisis. The Bank of England’s forecasts of the economic impact of Brexit have so far been wrong. It is hard to justify handing power to unelected technocrats if they fall down on the job.

All of which leaves the future of central banks uncertain. The independence granted them by politicians is not guaranteed. Politicians rely on them in a crisis; when economies recover they chafe at the constraints central banks impose. If history teaches anything, it is that central banks cannot take their powers for granted.

0 comments:

Publicar un comentario