Oops: The Buyback Party Is Over

by: The Heisenberg

- Are you aware of just how important buybacks are for US equities?

- I certainly hope so, because if you look at net equity demand, there simply wouldn't be much (demand) if it weren't for repurchases.

- Here's Goldman's warning that details the extent to which this bid is "plunging".

- I certainly hope so, because if you look at net equity demand, there simply wouldn't be much (demand) if it weren't for repurchases.

- Here's Goldman's warning that details the extent to which this bid is "plunging".

I have seen (and participated in) all manner of schemes in my time.

The thing about schemes is that you don't want them to be too transparent. Because you know, if the scheme you're running is see-through, it's not much of a scheme, now is it?

Well, let me tell you something: the buyback scheme is just about as transparent as schemes get, and yet investors, presumably clinging to the same willful ignorance that keeps them from calling central bank market manipulation what it is, don't seem too inclined to recognize it.

Note that a scheme doesn't have to be nefarious. That's not (necessarily) what a scheme is. A scheme is just "a large-scale systematic plan or arrangement for attaining some particular object or putting a particular idea into effect," to quote the dictionary definition.

The buyback scheme fits that definition to a T. This is a really simple arrangement. Central banks drive down rates on safe haven assets, forcing investors down the quality ladder. The first place investors turn when government bonds are yielding nothing is corporate credit (NYSEARCA:LQD).

That demand drives down borrowing costs which incentivizes corporate debt issuance. The proceeds from that debt issuance are then used for buybacks. The buybacks artificially inflate corporate bottom lines. That, in turn, helps to buoy stock prices which, at the end of the day, is good for management's equity-linked compensation.

It really is just that simple.

Now a lot of people will say something like this: "don't let Heisenberg fool you, there's nothing wrong with this."

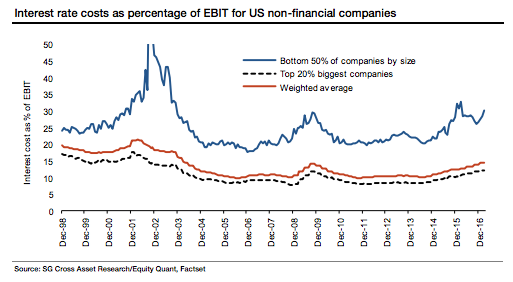

Under normal circumstances, that would be correct. But in today's world, the people who say that are wrong. Because the debt that funds these buybacks is being issued at artificially suppressed rates. So this is just balance sheet leveraging or financial engineering assisted by central banks. And it's creating a leverage problem that looks like this:

(SocGen)

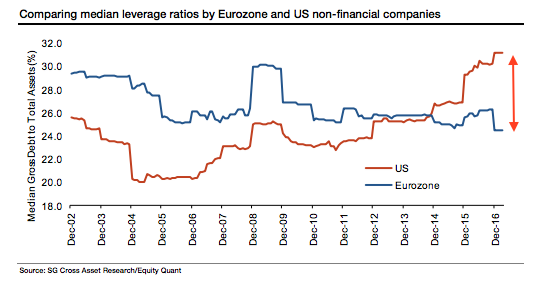

Or, if you want some international context, like this:

(SocGen)

But irrespective of whether you think all this leverage is likely to create a problem when the cycle turns (more on that here), equity investors (NYSEARCA:SPY) need to ask themselves what it means for stock prices if the heretofore insatiable corporate bid dries up.

And guess what? It just dried up.

On Friday evening, Goldman was out with a harshly worded note the gist of which is, to quote the title of the piece, "management and investor obsession with buybacks fades." Here are some key excerpts (full note here):

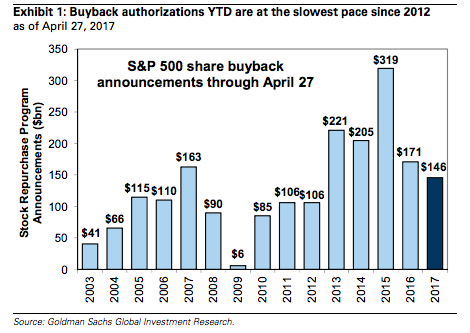

Following years of prioritizing repurchases as a use of cash, corporations actually cut annual spending on buybacks by 11% in 2016 and executions YTD have plunged by 20% vs. last year. Meanwhile, authorizations YTD for new programs are proceeding at the slowest pace in five years.

Experience shows that firms repurchasing shares at extremely high valuations regret those actions when the stock price inevitably de-rates. The median S&P 500 constituent currently trades at the 98th percentile of historical valuation across a variety of metrics.

The GS Securities Division reports that buyback executions YTD have plunged by more than 20% compared with the similar year-ago period.

Looking forward, repurchase authorizations also suggest that buyback growth will decelerate. S&P 500 firms have authorized $146 billion in share repurchases YTD, a 15% drop from the comparable point last year and the slowest pace since 2012 (see Exhibit 1).

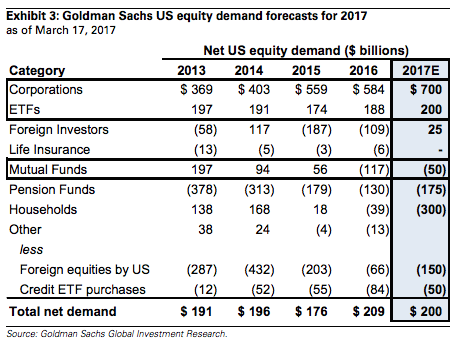

It should be obvious why that matters, but in case it's not, here's one of my favorite visuals:

(Goldman)

See where the bid for stocks has come from for the last half decade?

Make of the above what you will, but do note that this is apparently one scheme that looks like it's going to come and go without retail investors ever fully appreciating its impact.

Of course, you never know what you've got 'till it's gone.

0 comments:

Publicar un comentario