China’s Titanic Debt: Downgrade Carries a Bigger Warning About Growth

Ratings firm joins the choir telling Beijing its model isn’t working

By Mark Magnier and Carolyn Cui

BEIJING—China’s stepped-up efforts to attract more foreign capital to its financial markets could become more complicated after a downgrade from Moody’s Investors Service, its first of China’s government in 27 years.

Moody’s rating action on Wednesday also reinforced a widely held belief that China needs to do more to address its mounting debt levels and slowing economic growth.

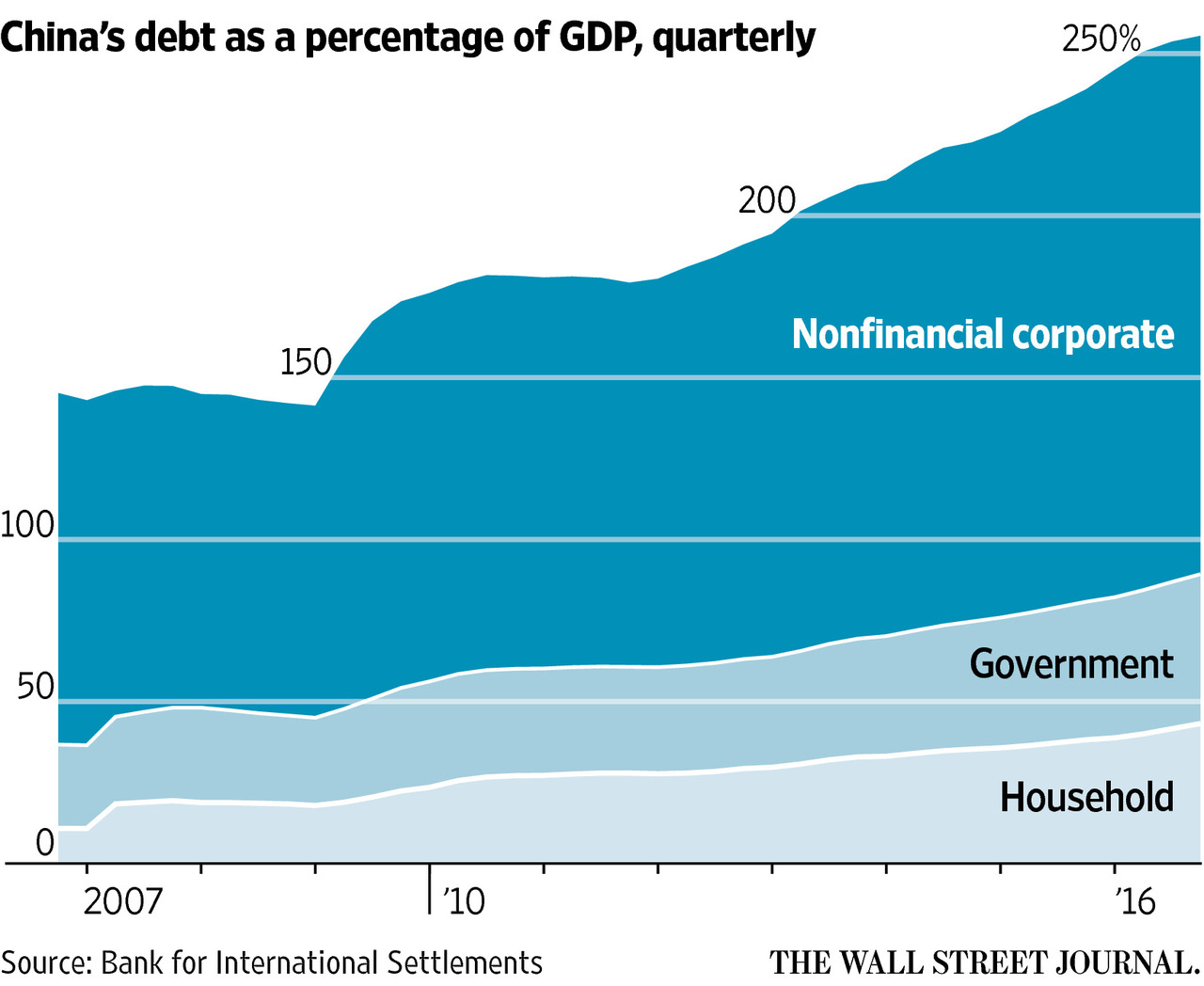

China has enjoyed a favorable credit rating for decades, thanks to its high level of foreign reserves and little external debt. But the rapid growth of domestic debt in recent years, especially in the corporate sector, has reached a level that is starting to erode China’s creditworthiness, analysts said—especially at a time when the economy is expected to grow at a slower pace.

Moody’s said in its downgrade that “we expect China’s growth potential to decline to close to 5% over the next five years,” a notable deceleration. China’s economy expanded 6.7% in 2016, and hit a recent peak of 10.6% in 2010.

Some investors said the downgrade was hardly a shock given China’s well-documented debt problem. Others noted that China’s new rating is still investment-grade, ranking it near the top of the developing world. Chinese officials also took issue with Moody’s methodology.

Yet some analysts said the downgrade could aggravate China’s attempts to lure more global investors to its $9.7-trillion bond market. The government is counting on foreign capital to offset some of the outflows from Chinese companies and investors. Rising foreign flows would also help support the yuan, China’s currency, which has come under pressure in recent years as Chinese stash more money abroad.

China’s central bank officials have met with investors around the world in recent months to generate interest for China’s financial markets. The government has been gradually opening its domestic bond market to foreigners, including central banks and sovereign-wealth funds. But a cumbersome application process has turned off many fund managers who would like to buy Chinese debt, some investors say.

Officials have also lobbied global index providers for China’s inclusion. Chinese representatives have tried for more than a year to win a place in J.P. Morgan Chase & Co.’s widely followed emerging markets bond index but have yet to succeed.

Moody’s lowered China’s government debt rating one notch to A1 from Aa3. S&P Global Ratings last downgraded China’s government debt in 1999, while Fitch Ratings most recently cut China’s debt in 2013.

The International Monetary Fund, World Bank and Bank for International Settlements, among others, have long expressed concern about China’s surging debt levels. Some analysts suggested that the downgrade would heighten concerns about investing in the country’s bond market.

“For portfolio managers, it will be even harder now to justify moving into the Chinese bond market given that most of the ratings seem to be headed downwards, suggesting higher risks,” said Eswar Prasad, a professor at Cornell University and former head of the IMF’s China division.

Others said that foreign investors were likely to demand higher yields to compensate for the lower credit rating.

The downgrade news triggered an early selloff in Chinese stocks on Wednesday, with shares in Shanghai falling more than 1% before recovering and largely shrugging off the move.

Reaction in China’s bond market was muted. Analysts said that is because an overwhelming portion of China’s debt is held domestically. Foreign investors owned about 1.5% of the Chinese local bond market at the end of March, according to the People’s Bank of China.

Local investors are unlikely to sell the debt due to rating changes, and the few foreign investors who are in the market are in there for the long run, analysts said. That makes China’s markets less vulnerable to others’ assessment of its credit risks. It also limited the impact of Wednesday’s downgrade on other emerging markets, where currency and bond market performance was mixed.

“This is not going to change the way how investors view the [China] story,” said Kevin Daly, a portfolio manager at Aberdeen Asset Management , which owns Chinese bonds in its Asian portfolios.

Mr. Daly said the sheer size of China’s bond market, along with its relatively high ratings, makes it a market that many foreign investors are looking to get involved eventually.

Carlyle Group co-founder David Rubenstein said the company, which has invested $1 billion a year in China on average over the past four years, is increasing its investment. “The U.S. was downgraded a few years ago as well, and that hasn’t stopped us from investing in the U.S.,” he said.

China’s Finance Ministry called the methodology behind Wednesday’s downgrade “inappropriate” and said Moody’s overestimated China’s economic difficulties.

In its credit analysis, Moody’s wrote that debt held by local Chinese governments and some state-owned enterprises represents an indirect sovereign liability because the government would likely backstop those loans. This debt accounts for 114% of China’s gross domestic product.

Chinese officials said that under Chinese law the central government isn’t responsible for debt issued by local governments or state-run enterprises.

The downgrade also reflects an assessment that China’s ability to service its surging debt burden is being eroded, said Moody’s sovereign-debt analyst Marie Diron.

Though Beijing disputes that view, it has unleashed a flurry of moves and regulations this year to slow the pace of borrowing, including an increase in short-term interest rates and restrictions on speculative property markets. Moody’s cited such moves as positives.

But market gyrations in reaction to those moves have underlined Beijing’s bind: Moving too rapidly to deleverage could create its own instability. “We’re hoping now to avoid risks that have resulted from the regulations to resolve risk,” said Xiao Yuanqi, a bank regulator, earlier this month.

The largest share of China’s debt, at around 164% of GDP, is issued by companies. The debt was built up after years of loose monetary policy and aggressive fiscal spending. It has fueled excess production capacity in industries from steel to glass and increased the number of “zombie” companies unable to meet their interest payments. Moody’s on Wednesday also downgraded the ratings of 26 state-owned companies.

—Lingling Wei, Liyan Qi and Grace Zhu contributed to this article.

0 comments:

Publicar un comentario