Why The Fed May Need To Begin Unwinding Its Balance Sheet

by: Long/Short Investments

Summary

- The Federal Reserve has increased rates twice in its past three meetings.

- However, despite boosting rates from a lower-bound yield of just 0.25%, this hasn’t provided any real boost to back-end yields.

- Accordingly, with demand staying steady for higher-duration fixed-yield securities, the Fed may run into an issue with excessive flattening of the yield curve.

- I run through one way to potentially alleviate this issue.

- I consider some of the basic benefits, weaknesses, and potential ramifications of the idea, including likely effects on the financial markets.

- However, despite boosting rates from a lower-bound yield of just 0.25%, this hasn’t provided any real boost to back-end yields.

- Accordingly, with demand staying steady for higher-duration fixed-yield securities, the Fed may run into an issue with excessive flattening of the yield curve.

- I run through one way to potentially alleviate this issue.

- I consider some of the basic benefits, weaknesses, and potential ramifications of the idea, including likely effects on the financial markets.

Argument

If the US Federal Reserve begins to prioritize running off the long-dated assets on its balance sheet, this will have the effect of boosting back-end yields on the yield curve. The effect of this could be twofold:

(1) It helps steepen the yield curve, which is essential for the sake of bank profitability and overall health of the economy

(2) It will assist the Fed in finding a way to wind down its balance sheet while accomplishing its current prerogative to tighten monetary policy at the same time

At the same time, there are drawbacks:

(1) Ratcheting up back-end yields will cause some level of capital flight out of stocks as bonds become comparatively more attractive from a risk-reward standpoint. This could, at least in the short-term, remove wealth from the economy as investors move into lower-yielding assets.

(2) This would affect the Fed's current plans of hiking short-term interest rates over the next 1-3 years. Tightening monetary policy using the overnight rate (also known as the federal funds rate) is the most common policy approach and its effects are the most predictable.

Running off long-dated balance sheet assets and raising the fed funds rate simultaneously (and on its currently anticipated schedule) may tighten financial conditions too quickly.

In terms of financial market ramifications this would benefit:

(1) Any news on this would benefit the US dollar (NYSEARCA:UUP) (NYSEARCA:UDN), as more capital migrates into US markets in anticipation of higher yields.

(2) US banks and lenders (NYSEARCA:KBE) (NYSEARCA:IYG), which rely on yield curve steepening to enhance their profits.

(3) Those involved in the "short Treasuries" trade (NYSEARCA:TBT).

Overview

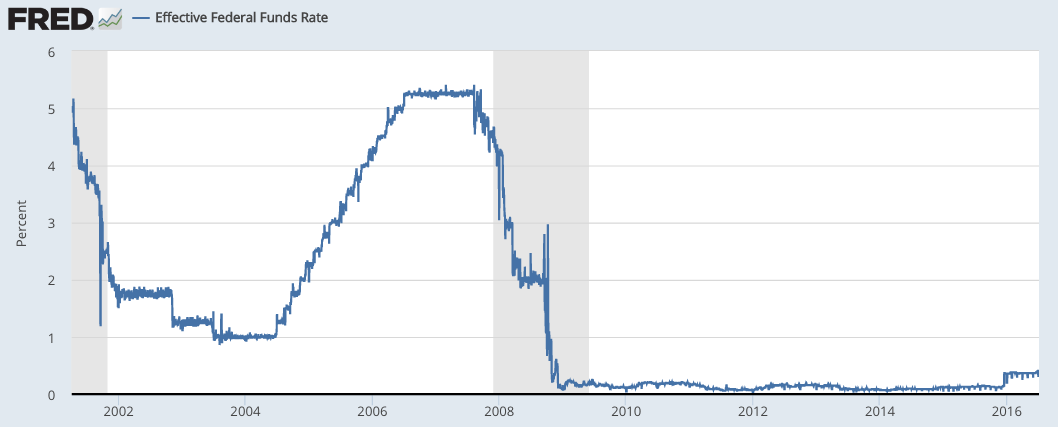

The Fed is in the midst of what is likely a somewhat short tightening cycle. I expect the Fed to boost overnight rates to somewhere in the 2.25%-3.00% range before it needs to begin cutting them again as risk builds in the system. This would be roughly half the peak of the previous tightening cycle undertaken from 2004-06, when the overnight rate hit 5.25%.

(Source: St. Louis Federal Reserve)

My belief is that global demand for liquid, safe securities and various domestic and global structural impediments to inflation will keep back-end yields lower. The Fed cannot raise to the point where it excessively flattens or inverts the yield curve. This strains bank profitability and precedes virtually every recession.

One way to alleviate this potential concern is to target back-end yields. Back in September, the Bank of Japan worked on steepening its yield curve by not only adjusting the front-end of the overnight rate, but by also pegging the 10-year yield to a point between 0-10 bps. The easiest way for the Fed to do this is not a peg, which can prove costly (i.e., not having the ability down the road to buy or sell enough assets to maintain it), but rather by unwinding a portion of its balance sheet.

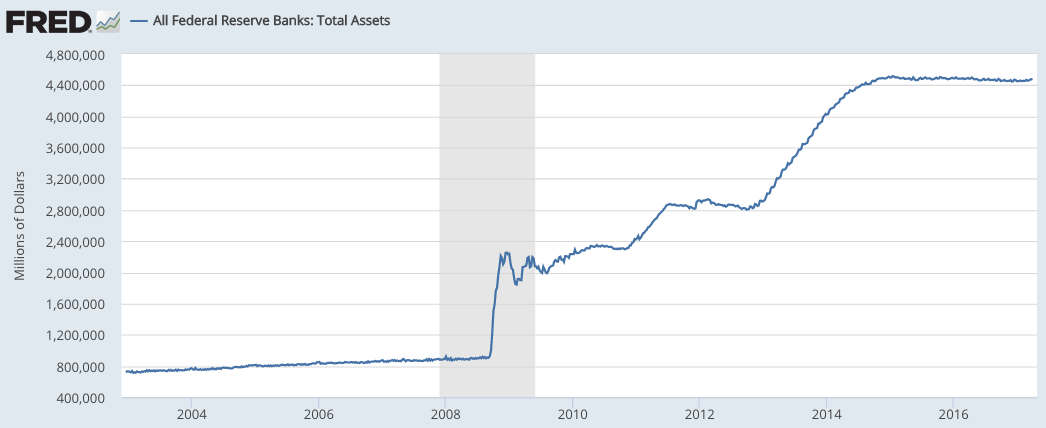

Back on September 3, 2008, just before the fall of Lehman Brothers, the Fed's balance sheet stood at $905 billion. By December 2014, it had roughly quintupled to $4,509 billion. This is currently around 24% of GDP.

(Source: St. Louis Federal Reserve)

Of these assets, they are categorically split as the following:

(Source: Federal Reserve)

By piling all these assets on the Fed's balance sheet, this has worked to drive up market demand for these instruments. Accordingly, prices on these have increased and yields have gone down. When these yields are no longer attractive, this has forced investors out over the risk curve into historically higher-yielding securities. Theoretically, this will help drive up economic wealth throughout the economy and produce more growth.

Given these are all fixed-income instruments, they have finite durations. When these securities expire, the Fed has reinvested the proceeds into new securities to keep this monetary accommodation tool in place at its current levels.

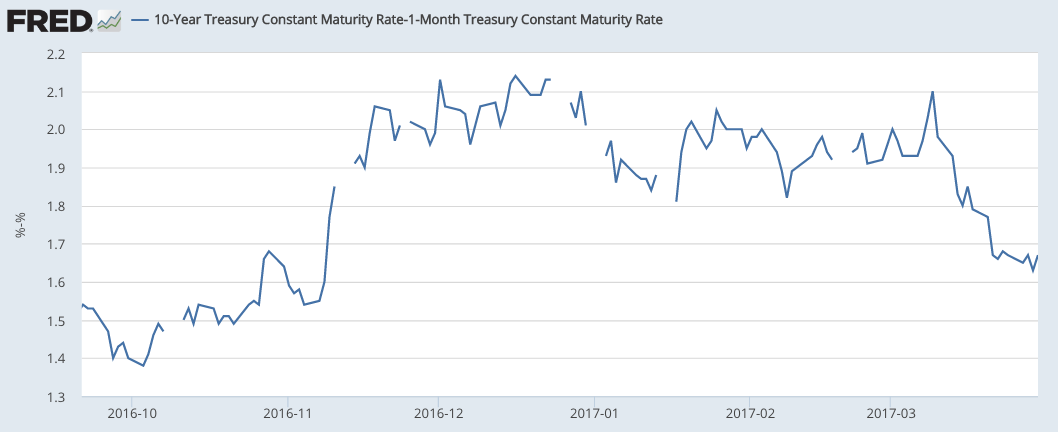

The Fed has already observed a 50-bp compression in the 1-month/10-year spread since it raised rates from a 0.25% lower-bound at its December meeting.

(Source: St. Louis Federal Reserve)

If the Fed continues to observe that raising the overnight rate is failing to provide sufficient levity to the midpoint and back-end yields as well (i.e., 5+ year yields), engineering a passive run-off with respect to longer-duration assets is one potential option.

Of its balance sheet assets, 12% have a remaining maturity of 0-90 days, 4% from 91 days to 1 year, 26% from 1 year to 5 years, 8% from 5 years to 10 years, and 50% from over 10 years.

Therefore, with half its balance sheet at a 10-year or greater remaining maturity and 58% at a 5-year or greater remaining maturity, passive run-off of these longer-duration assets provides one way to augment yields on the back-end without any strictly active policy approach, per se.

This could have the benefit of steepening the yield curve by opening up more supply of long-dated US fixed-yield securities. This would also boost lenders profits, who control the flow of credit in the economy.

However, if the Fed tightens too quickly, this can create a host of issues such as:

(1) An excessive hike in corporate capital costs, which could undermine business confidence, and result in wider corporate bond yields and higher fixed-income yields generally.

(2) An overly strong US dollar. After the dollar passes a certain level of strength, the marginal benefit to consumption may not outweigh the marginal hit to exporters, and produce a drag on growth.

(3) Pressure on equity valuations, which could in turn wipe out a material level of wealth from the economy. As yields rise, returns expectations with respect to stocks will increase in conjunction.

Without improvements in business fundamentals (or the expectations of such), equity values could decrease.

What it would mean for financial markets

(1) As mentioned, any tightening measure generally is bullish for the US dollar with other central banks in developed markets - ECB, BOJ, SNB, BOE - in accommodation mode.

(2) "Long US banks," another popular trade up there with "short Treasuries" and "long the USD," would benefit as it would allow these institutions to fulfill their fundamental role of borrowing on the short-end (still relatively cheaply) and lending more expensively on the long-end. With respect to the remainder of the equities market - and risk assets more generally - the effect is less clear.

(3) "Short treasuries" benefits. I've written before that I believe it's more attractive to short the front end of the yield curve rather than the back-end. Demand for safe, liquid securities remains high and there are various domestic and foreign structural obstacles to rising inflation going ahead. I believe that core inflation will remain in the 1.7%-2.0% range to end the year.

Conclusion

Unwinding the balance sheet isn't necessarily a priority for the Fed, but if the back end of the curve isn't showing adequate sensitivity to increases in the overnight rate (as is the case based on the last two hikes), it provides a tool by which it can use for this purpose.

If the Fed hikes twice more and finds that back-end yields are holding fairly steady (as I expect them to) and it's merely flattening out the curve rather than pushing it upward in mostly parallel fashion, it may need to rethink its approach. Running off the longer-duration securities can provide some level of buoyancy to back-end yields to allow the curve to remain upward-slanting. Flattening or inverting the curve saps bank profitability and is usually an indication that the current business cycle is running on its last fumes.

The weaknesses of this proposal include the lack of clarity in how markets would react. It would also interfere with the Fed's current tightening plans (using the well-trodden path of adjusting the overnight rate) given it would add another layer of tightening. It may excessively strengthen the dollar, which can produce a drag on growth should it too significantly impair the export sector.

Capital costs would also rise across the spectrum, which expands discount rates at which cash flows are valued and can compress valuations without a concomitant rise in earnings or expected improvement in business fundamentals beyond what is already priced in. This would pressure risk asset valuations as liquidity is removed from the system and increase risk more broadly.

Potential winners in the financial markets would include those involved in probably the three most crowded trades in the market today:

1. Long USD

2. Long Banks

3. Short US Treasuries

The Fed is likely several months off from needing to know whether or not it needs to act on unwinding its balance sheet. It also needs to understand how its current strategy is working and whether the economy is sufficiently healthy to make such a move, such as meeting real growth and inflation targets roughly at least 2% apiece.

Letting long-duration securities run off the balance sheet will give the Fed a "curve steepening" tool as well as a means by which it can more effectively use the balance sheet in the future to stimulate the economy in the future. Central banks such as the ECB and BOJ have run into issues of running out of bonds to buy to sufficiently stimulate their own economies - and perhaps call into question the efficacy of quantitative easing itself. By carefully removing some of this liquidity from the system, the Fed can effectively provide more "ammo" for itself when it needs to use monetary policy tools in the future to kickstart the economy from its end.

0 comments:

Publicar un comentario