The Fake Recovery May Be Ending

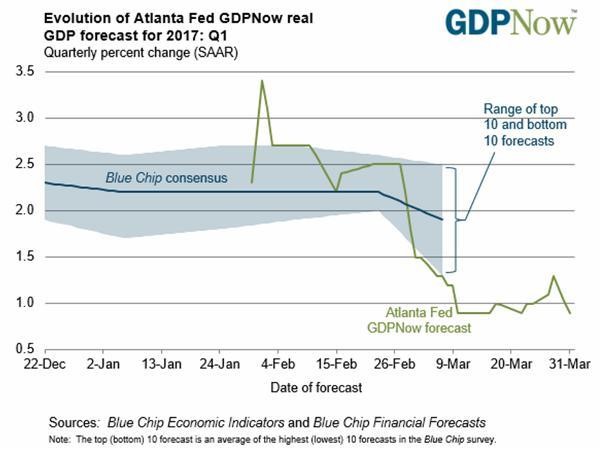

The “real” Atlanta Fed’s reading of Q1 GDP went off a cliff to less than 1%:

No one has the slightest idea of what is happening as insane levels of debt distort the model’s which economists use to forecast the future economic trends. From here on out, there will be unpleasant surprises all the way around. According to shadow stats, the GDP is in contraction at the rate of -2%.

The New Normal & Disconnect:

The FED and other agencies have taken on new responsibilities for managing systemic risk since the financial crisis of 2007.

What grade have they earned? The impact of implemented low-interest rates for savers has made them poorer. All pension plans, college endowments, and state retirement plans have been diminished and devastated by low-interest rates. Savers have suffered and will continue to do so because of ‘financial repression’.

Furthermore, because low-interest rates make savers poorer, the contracting economy has limped along with anemic growth rates. Low-interest rates have had a negative impact for almost everyone.

Preparing For The Big Crunch!

The FED will respond with even more aggressive money printing — which will then cause the entire monetary system to implode some day. Money is not wealth, but rather it is merely a claim on wealth. Debt is a claim on future money. The only way to have faith in our current monetary policies is if one believes that we can grow our economy and GDP out of this massive debt that we have created. The U.S. is already insolvent, meaning liabilities exceed assets. The U.S. has been spending, far beyond its’ means, for multiple decades while amassing tremendous amounts of public debt, private debt and entitlement liabilities.

The Austrian economist Ludwig von Mises said, “There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.”

U.S. economic growth began slowing down due to its’ acceleration of ‘too much debt’. Instead of allowing natural market forces to clear out the excessive debts, the Federal Reserve chose to go into overdrive to ‘remedy’ the problem. Its’ remedy? Drive interest rates to 0% to reduce the service burden of those debts and print trillions of fresh dollars which, in turn, would fund new borrowing.

Of course, no true ‘solution’ for resolving debt involves piling up even more of it. The only path that history has shown that works involves fiscal austerity and reducing debt. The only real solution is “a voluntary abandonment of the credit expansion”.

The only possible solution for recovery, today, is if the economy suddenly returns to an extremely rapid economic growth over an extended period of time. If during such a period of rapid growth does occur, we must use that windfall to pay down the outstanding debts! The intent of the FED treading into the never-before-tried ZIRP and NIRP waters was to ignite more borrowing, not more spending!

Pension plans have been ultimately decimated by these monetary policies!

Pension funds across the U.S. are desperate to overcome low interest rates and return to the time when future retirees were entitled to and could receive their full benefits. Pension funds which so many depend upon for their retirement security will lose trillions of dollars which will result in the depletion of receiving their benefits!

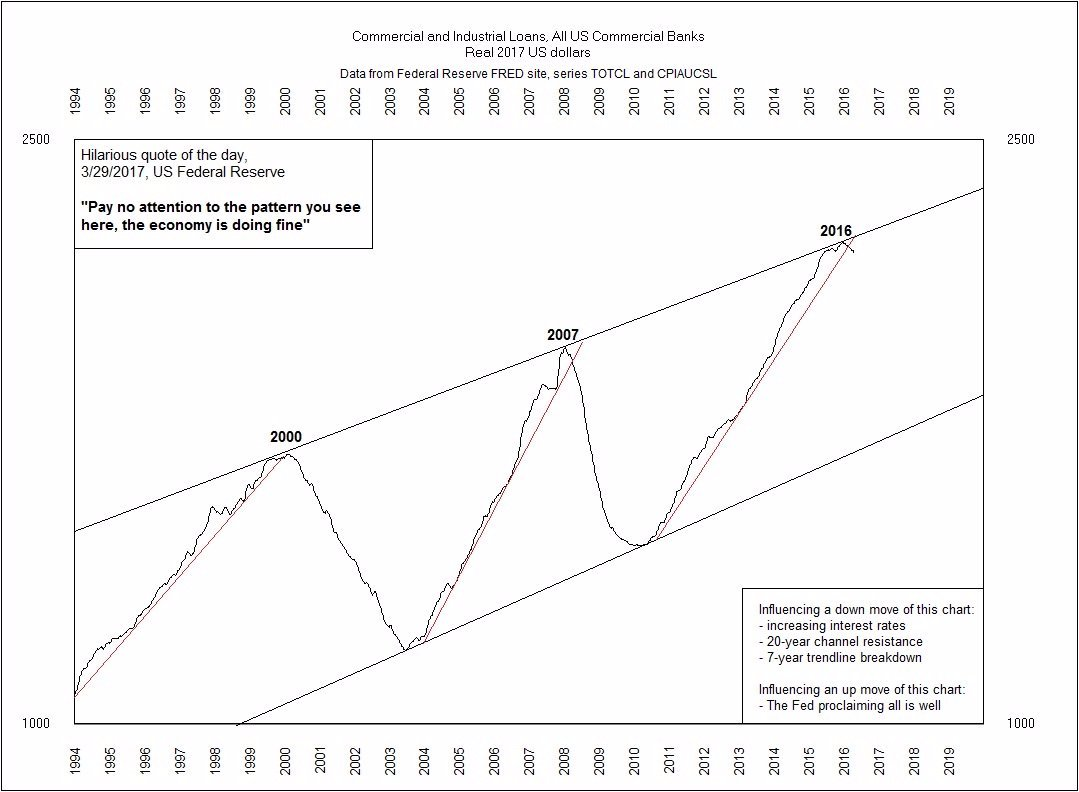

The chart below reflects the last two times that industrial and commercial loan contracts crashed which were in 1999 and 2007!{25 year chart} of all American Bank Commercial and Industrial Loans.The last 2 times loans contracted and broke down was 1999 & 2007

0 comments:

Publicar un comentario