US Treasuries: On the cusp of a reversal

Some see the end of the bond bull run amid signs of growth, inflation and a rate

by: Joe Rennison and John Authers

.

One of the longest and most important trends in world finance may be on the cusp of a reversal.

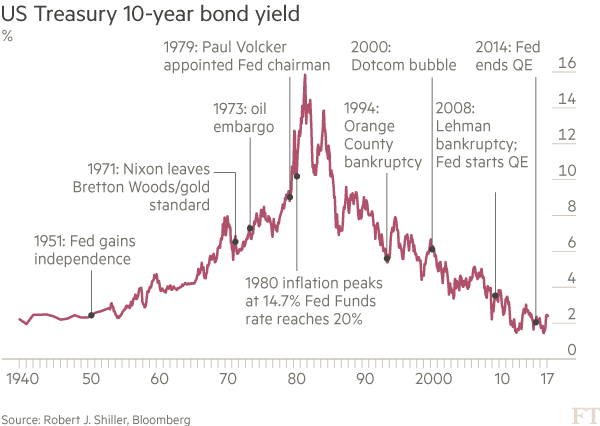

US 10-year Treasury bond yields, used as a benchmark in transactions the world over, have been in decline since inflation came under control in the early 1980s.

But in the past week, yields have risen to their highest in almost three years, while the US jobs market has grown its fastest in more than a decade. With equity markets suggesting that growth and inflation are in store under President Donald Trump, and with the Federal Reserve committed to raising its base rates this week for the third time in a decade, some bond market luminaries are convinced that the great “bull market” is over. From now, they expect interest rates to rise steadily.

“I believe the secular decline in yields is over,” says Henry Kaufman, the Wall Street economist known in the 1970s as Doctor Doom for his accurate forecasts of higher inflation and interest rates. “It will not come back.” His latest book carries the ominous title Tectonic Shifts in Financial Markets.

Bill Gross, co-founder of Pimco and the best known bond investor of recent decades, warned in January that if the level of 2.6 per cent on 10-year yields was breached then “a secular bear bond market has begun”. As that level was touched last week, the Janus Capital bond manager warned the US economy was like a “truckload of nitroglycerine on a bumpy road”, where a mistake could “set off a credit implosion”.

The Treasury market moves in three-decade cycles

Bond yields rose after a period of wartime financial repression and peaked as inflation approached 15 per cent. Then the Federal Reserve under Paul Volcker raised rates, convinced markets inflation was beaten and pushed yields down. After the 2008 financial crisis the Fed held yields down

But there have been many false alarms when the bond market appeared to turn, only for yields to fall again. Last summer they dropped to an all-time low of 1.36 per cent after Britain’s referendum on EU membership. Even now, bond market participants remain unconvinced by the signs of economic growth that have driven US stocks to records, while the overwhelming belief is that rises will be gradual. Out of 56 market analysts polled by Bloomberg, only 13 believe that the 10-year yield will rise even as far as 3 per cent by the end of this year. This would be no higher than it was three years ago, when there was still a widespread fear of deflation.“

We are certainly well off the bottom,” says Tod Nasser, senior vice-president for investment management at Pacific Life. “But it is not a game changer.”

Much is at stake. Higher bond yields would bring relief to pension funds by making it easier for them to finance their payment obligations. But higher yields would make it harder for indebted companies to roll over their debt and inflict losses on bond and credit investors.

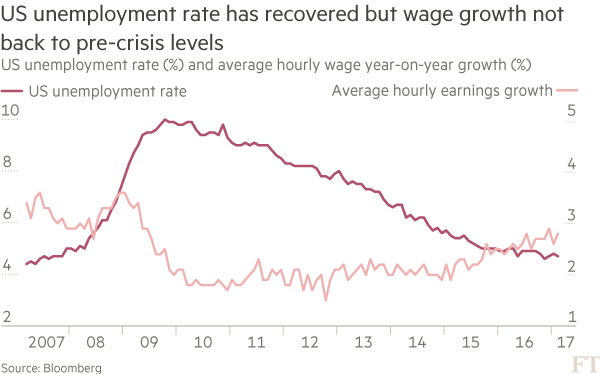

The economic case for US rates to rise is clear. Employment is growing. The jobless rate, at 4.7 per cent, has completed its recovery from the crisis (although this has been helped by an increase in the numbers not seeking employment). Wage inflation, at 2.7 per cent, is recovering, although it remains painfully weak compared with the pre-crisis period. Surveys show the confidence of consumers, small businesses and investors at levels not seen since before the crisis.

Fed governors, led by the chair Janet Yellen, have made clear their intent to raise rates this week, and markets now regard this as a certainty. Most significantly, Lael Brainard, the Fed governor most known for her reluctance to raise rates, says the US economy is “at a transition”. This was perceived as a watershed moment. After years when traders refused to believe the Fed’s threats to raise rates, futures markets now suggest that three rate rises this year are probable, while the chance of four rate rises — unthinkable three months ago — is about one in four.

The labour market awaits higher rates

Despite long-term unemployment, the jobs market has more or less recovered from the 2008 crisis and wages have started to rise. This has helped convince the Fed to raise short-term interest rates, which should push up long-term bond yields

But despite all this, 10-year Treasury yields are barely even positive in real terms, as inflation is accelerating. They remain just below Mr Gross’ threshold of 2.6 per cent and do not yet put a brake on growth, or on speculation.

A tension in markets persists. While equity markets are positioned for growth and interest rate increases, bond investors largely remain convinced that interest rates will not go up much, and that any rises will be steady.

Why? First, growth is in question, says Mike Lillard, chief investment officer at Prudential and member of the Treasury Borrowing Advisory Committee that advises the US government on debt management issues. “We remain in a low-growth world,” he says. “And we do not think the Trump administration can change that.”

More broadly, many argue that there has been a shift in the US economy. With productivity low and the economy less exposed to oil shocks, long-term rates as high as 16 per cent, which occurred during the 1970s and 1980s, are unlikely to be repeated. “We will not come back to that,” says Mr Kaufman.

Other structural factors also weigh on rates. The percentage of the US population aged 65 and over rose to 15 per cent in 2015 from 9 per cent in 1960. This will increase further, crimping growth and potentially raising the demand for bonds. (As people retire, they tend to sell equities and buy bonds.) “Society is ageing,” says William Irving, a bond manager at Fidelity Asset Management. “The proportion of old people is at an all-time extreme and that has contributed to slow growth and lower rates.”

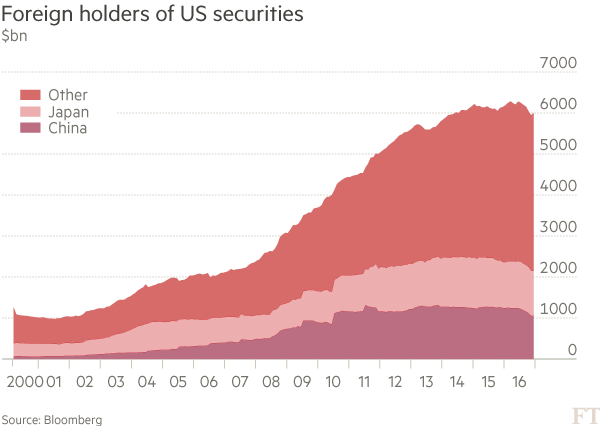

Foreign buying declines

Meanwhile, foreigners’ purchases of Treasuries appear to be tailing off as foreign central banks worry that US bonds have become too expensive. China and Japan, the biggest foreign holders of US government debt, have reduced their holdings

Meanwhile, those of working age are producing less. Growth can be described as the sum of a rising workforce and higher productivity. While jobs have increased to the point where the Fed can claim the US is at full employment, productivity has stagnated. Year-on-year growth in output per hour worked remains at 1 per cent, according to data from the Bureau of Labor Statistics.

“The only way rates could be sustainably higher is to overcome secular stagnation and that requires a recovery in productivity,” says Dominic Konstam, global head of interest rates research at Deutsche Bank.

A further problem comes from the overhang of US debt. Prolonged low interest rates have prompted companies to issue debt and made it easier for junk-rated borrowers to persuade yield-hungry investors to offer them financing. Outstanding corporate bond levels have risen from $5.4tn to $8.5tn since 2008, according to the Securities Industry and Financial Markets Association.

This poses a risk for the future. If interest rates rose markedly, companies would lose access to financing, while an increase in the risk of default would damage the returns for their investors. Scott Mather, chief investment officer for US core strategies at Pimco, says: “The concept of a debt overhang is a real one and is one of the reasons we find it difficult to believe we will get back to old levels of growth.”

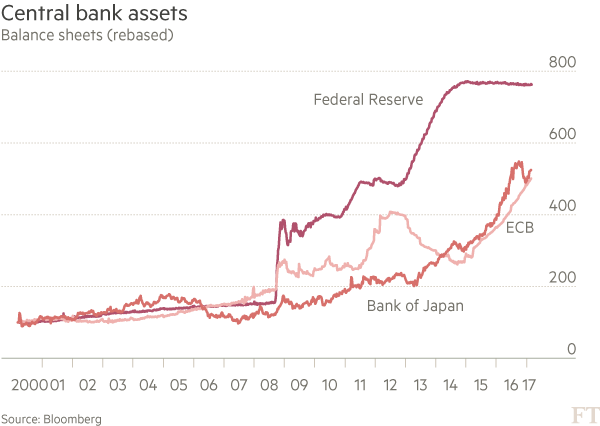

Quantitative easing — the large asset purchases pursued by central banks since the crisis — is also an issue. Although the Fed is no longer buying bonds, which pushes prices up and yields down, it still has a sizeable portfolio under management and is reinvesting the coupon payments it receives.

The Fed was the first central bank to halt QE

The Fed has stopped increasing its portfolio of US bonds, which should decrease downward pressure on yields. But it has not yet started to sell them — a move that could send up rates sharply — while other big central banks are still expanding their balance sheets

Many believe that the Fed could start to sell its bonds, but Mr Kaufman questions its ability to do this on any great scale. “I don’t think the Fed can do this in massive ways. At best it can do it gingerly. We would have to enter a period of significant increases in inflation for the Fed to consider doing it.”

The European Central Bank and Bank of Japan are still deep into their asset purchase schemes, although Mario Draghi, the president of the ECB, hinted on Thursday that the programme may not last beyond this year as he declared victory in the battle against deflation.

“You still have a massive amount of QE going on from the Bank of Japan and ECB,” says Mr Mather. “That certainly pulls down the equilibrium level of global yields.”

For now, QE in Europe intensifies foreign demand for US debt, where yields are higher for bonds of equivalent maturities. The gap in the yield Treasuries offer compared with German Bunds is the largest it has been since 1989, before German reunification, while the spread over UK gilt yields is its widest in history. This gives foreign investors a huge incentive to buy US Treasuries.

This may not last. China’s central bank has begun to sell off its inventory of more than $1tn in Treasury bonds. Japan, the biggest holder of Treasuries, has also been selling. But political risks, such as a populist victory in one of this year’s parliamentary elections in Germany, France or the Netherlands, could prompt investors to seek a haven in the US.

Higher US yields attract buyers from abroad

The extra yield on US bonds compared with other developed countries’ bonds is at a record. This creates an incentive for foreigners, especially in Germany and Japan where rates are negligible, to buy Treasuries. This keeps yields lower while raising the dollar

And in the US, equities rallied on the assumption Mr Trump could win a significant corporate tax cut this year, followed by a big infrastructure package. These moves would push up bond yields. But with the administration entering what could be a drawn-out process to replace former President Barack Obama’s Affordable Care Act before it can start on tax reform, doubts have begun to surface.

“Intentions are worth something but activity is worth more,” says Mr Nasser.

Investors say political doubts kept 10-year yields moving sideways for the first two months of 2017. “Bond markets have accommodated a good deal of what we can anticipate and now we need to see detail,” says David Ader, chief macro strategist of Informa. “We just don’t know yet. And in the past few years, realisation has proved disappointing.”

With so many factors pushing down on longer dated yields, it is easy to understand the cosy consensus that rises in rates will be very gradual. To rise significantly above 3 per cent, which would put pressure on the stock market’s gains, the market will need to be surprised.

That could happen if, for instance, the Fed moves quicker than expected or if global central banks start to reverse QE. In 1994, Fed governor Alan Greenspan was widely expected to raise rates. But when the pace of the rate increases was faster than expected, a disorderly spike in yields ensued. That pushed up the value of the dollar and the price of corporate credit, leading to the bankruptcy of Orange County and the Mexican peso crisis.

Even Albert Edwards, the bearish strategist for Société Générale in London, sees parallels to 1994, though ultimately he thinks that bond yields will be driven lower because of continuing deflation. In 1994, “it was excess leverage that broke the market”, he says. The same is true now, and yields could easily spike as the Fed tightens. “Despite remaining a secular bond bull, I think we are in for a rough ride, especially with equity markets at record highs.”

A final danger is complacency. William O’Donnell, fixed-income strategist at Citigroup, says the problems of demographics and productivity are not new and “have not sneaked up on anyone”. He points to a speech Ben Bernanke, the former Fed chairman, made in 2012, explaining how QE kept yields down. QE is now ending.

“It is simple logic. If what Bernanke said was true then, you have to assume the reverse is true now,” Mr O’Donnell says. “It increases the risk that we are stepping closer to a ‘sell everything’ market after nine years of a ‘buy everything’ market. I think there is a lot of dry tinder out there.”

0 comments:

Publicar un comentario