Gold And Silver's Drop Has Hit Precious Metals Investors Hard - Is It Time To Buy?

by: Hebba Investments

- Gold and silver prices dropped hard last week primarily on the realization that the Fed will hike interest rates during its upcoming meeting.

- Speculators sold off gold positions with the price drop but we still remain fairly high compared to historical net long positions at this price level.

- Silver speculators barely sold their speculative positions despite the silver drop and thus we remain very wary of silver.

- Asian premiums are rising with the recent drop in gold and that provides investors with some green shoots as we move forward.

- We are moving our outlook for gold from short-term bearish to neutral.

- Speculators sold off gold positions with the price drop but we still remain fairly high compared to historical net long positions at this price level.

- Silver speculators barely sold their speculative positions despite the silver drop and thus we remain very wary of silver.

- Asian premiums are rising with the recent drop in gold and that provides investors with some green shoots as we move forward.

- We are moving our outlook for gold from short-term bearish to neutral.

The latest Commitment of Traders (COT) report showed a predictable fall in speculative long positions and a rise in speculative short positions - which pretty much tracked the gold price.

We were surprised that we didn't see a larger drop in the speculative long position as gold dropped over 3% during the COT week (Tuesday to Tuesday).

But there were some green shoots for gold bulls as evidently physical demand in China and India both started to pick up signified by rising premiums in the physical gold market. While it didn't make up for the drop in both the speculative and ETF bullion sales, it is an important factor we look at as it can change the short-term bias of gold traders and obviously soaks up gold inventories.

We will get more into some of these details but before that let us give investors a quick overview into the COT report for those who are not familiar with it.

About the COT Report

The COT report is issued by the CFTC every Friday, to provide market participants a breakdown of each Tuesday's open interest for markets in which 20 or more traders hold positions equal to or above the reporting levels established by the CFTC. In plain English, this is a report that shows what positions major traders are taking in a number of financial and commodity markets.

Though there is never one report or tool that can give you certainty about where prices are headed in the future, the COT report does allow the small investors a way to see what larger traders are doing and to possibly position their positions accordingly. For example, if there is a large managed money short interest in gold, that is often an indicator that a rally may be coming because the market is overly pessimistic and saturated with shorts - so you may want to take a long position.

The big disadvantage to the COT report is that it is issued on Friday but only contains Tuesday's data - so there is a three-day lag between the report and the actual positioning of traders. This is an eternity by short-term investing standards, and by the time the new report is issued it has already missed a large amount of trading activity.

There are many ways to read the COT report, and there are many analysts that focus specifically on this report (we are not one of them) so we won't claim to be the exports on it.

What we focus on in this report is the "Managed Money" positions and total open interest as it gives us an idea of how much interest there is in the gold market and how the short-term players are positioned.

This Week's Gold COT Report

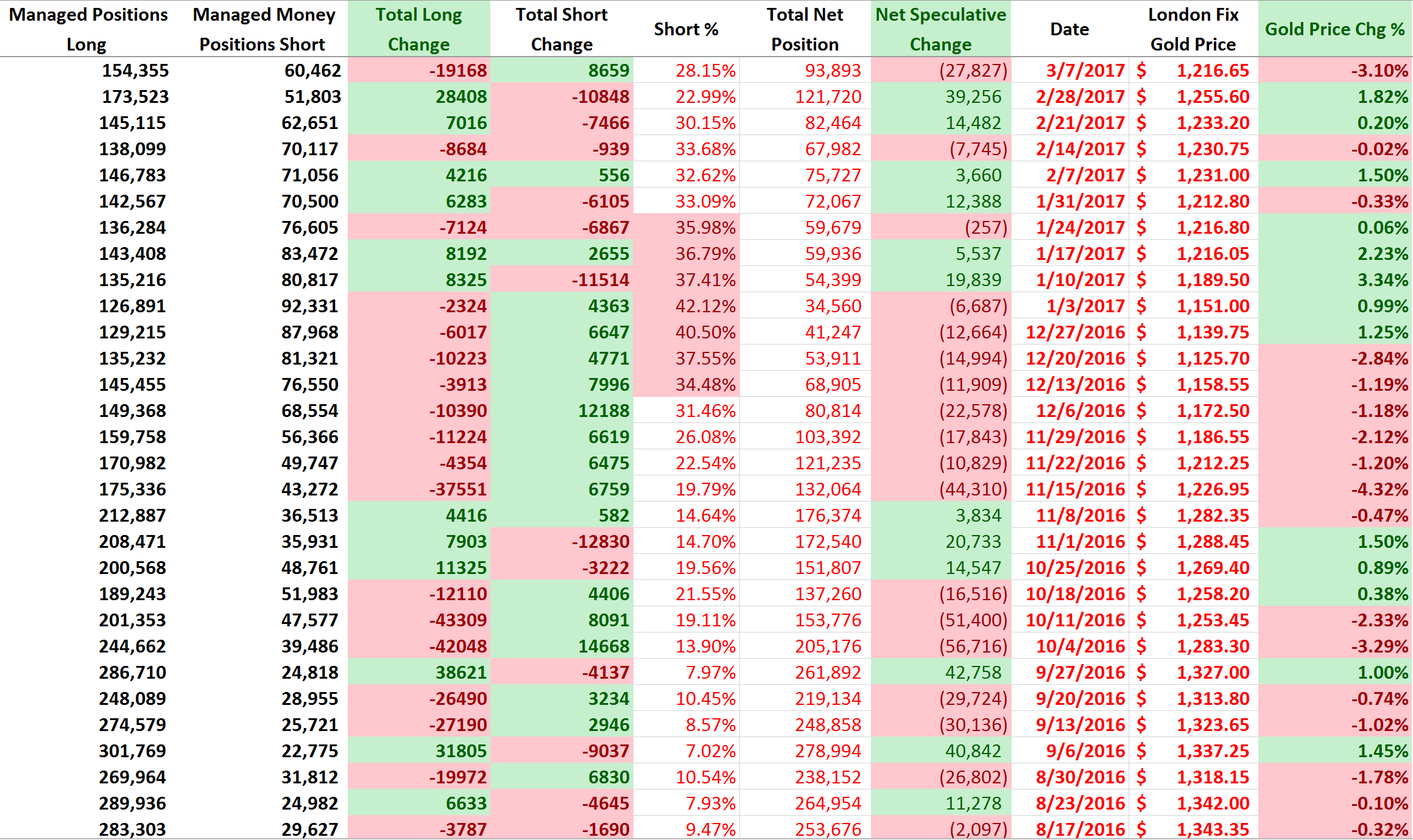

This week's report showed a decrease in speculative gold positions as longs shed 19,148 contracts during the COT week while shorts added 8,659 contracts to the gross speculative short position.

While it is good for the bulls that some weak hands sell their positions, we still point out that the net long position of 93,893 contracts is higher than the previous net long position of around 59,000 net long contracts from January where we hovered at the same $1216 levels. That shows we still have many more bulls than we had previously at the same price levels, and that is still a bit bearish from a contrarian view.

On the positive side, we do note that the net short position of 28.15% is still well above the average level (around 10%) that we see during short-term gold market upswings. There is plenty of shorts that can abandon positions and correspondingly push gold higher.

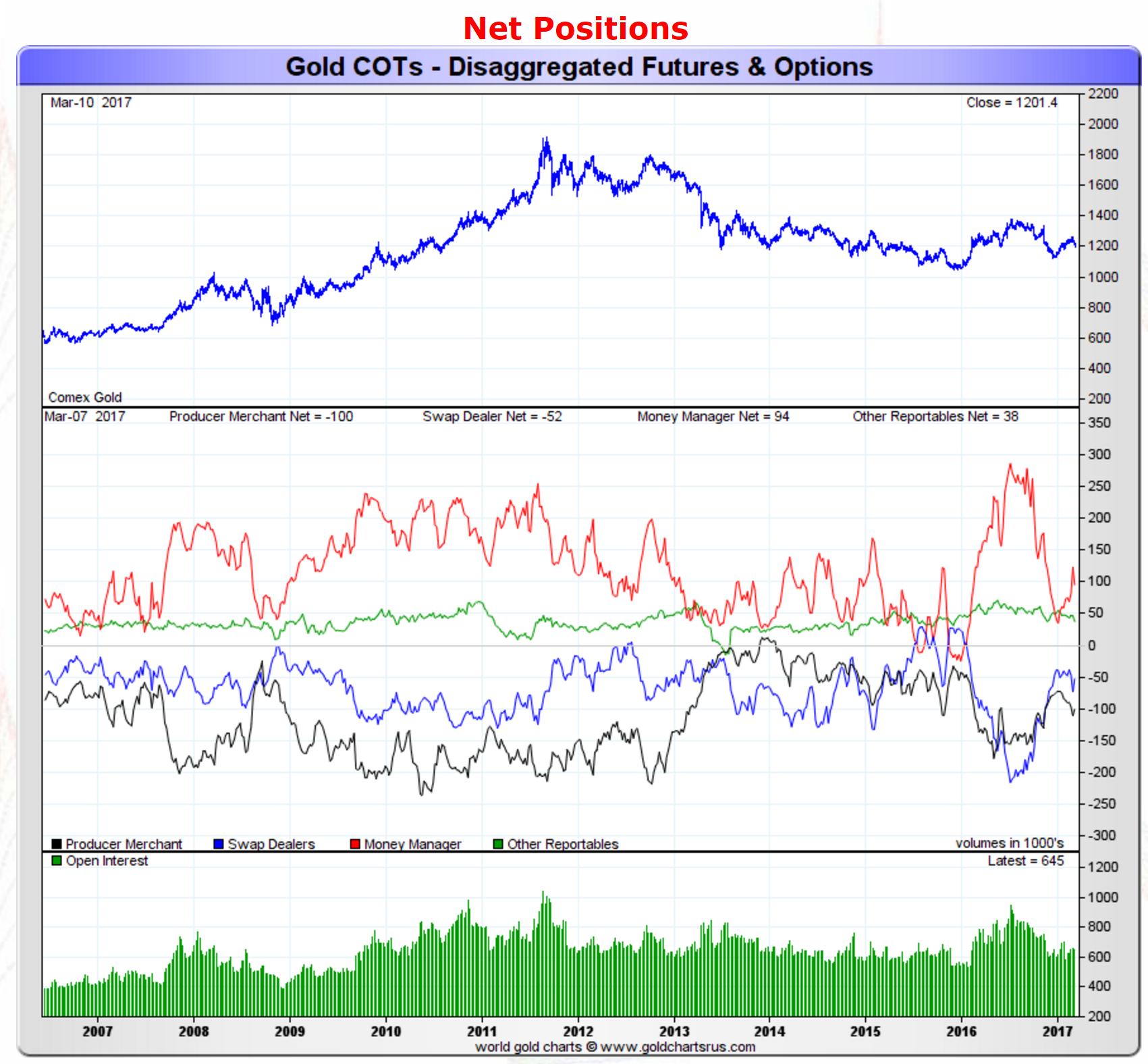

Moving on, the net position of all gold traders can be seen below:

Source: GoldChartsRUS

The red-line represents the net speculative gold positions of money managers (the biggest category of speculative trader), and as investors can see, we saw the net position of speculative traders decrease by 28,000 contracts to 94,000 net speculative long contracts.

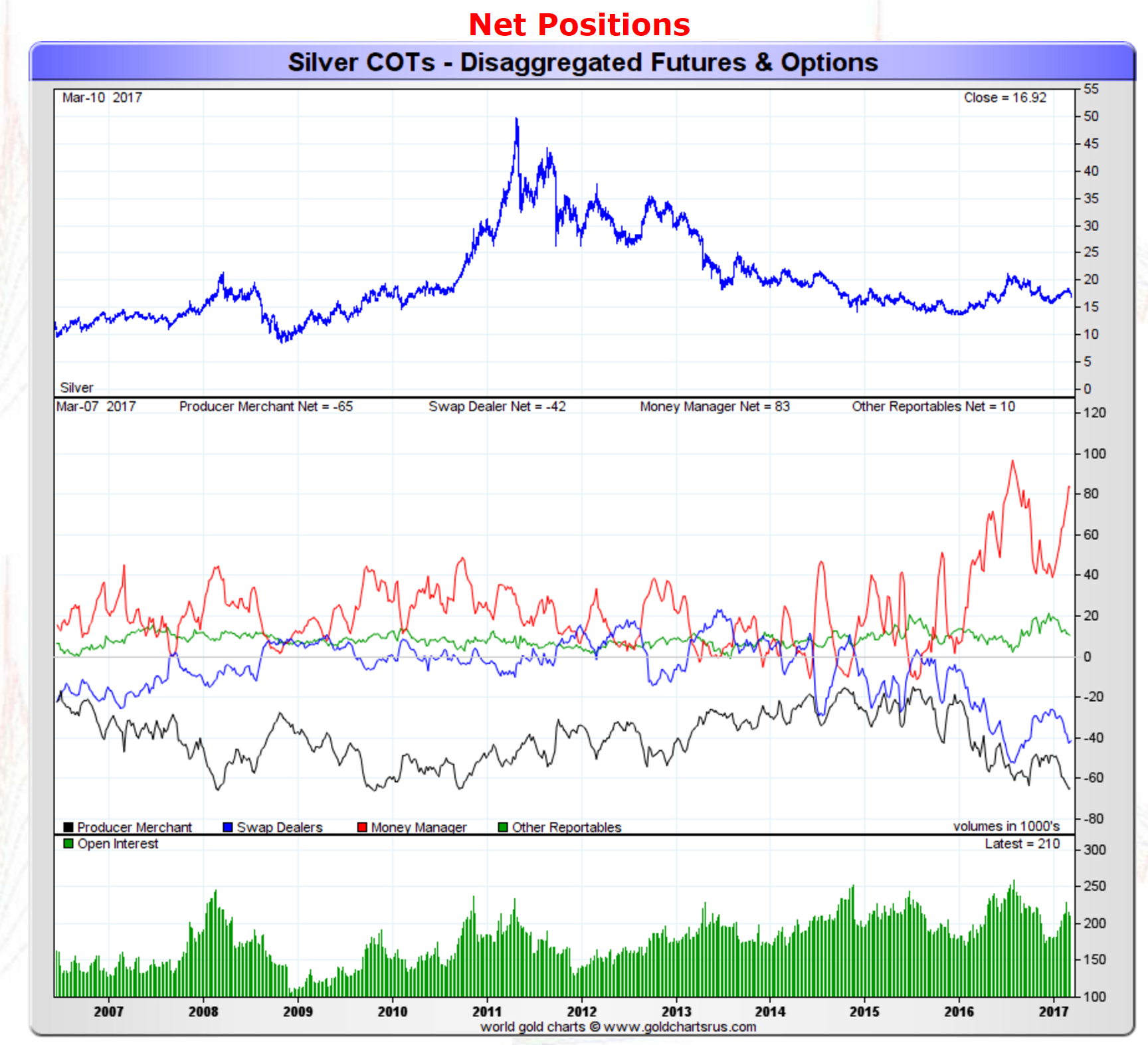

As for silver, the action week's action looked like the following:

Source: GoldChartsRUS

The red line which represents the net speculative positions of money managers, showed essentially no move in the net positions as speculative longs decreased their position by around 500 contracts and speculative shorts increased their own positions by less than 100 contracts on the COT week. Silver Producers/Merchants decreased their own positions on both the short and long side by around 2,000 contracts for the week, which is a neutral move on their part as they simply decreased silver exposure on both sides.

The speculative change in silver was a bit surprising as the metal fell during the COT week by a little under 3%, thus we would have expected to see a much larger drop in the net speculative bullish position than we did. Silver continued to fall after the COT report closed to end the week close to 5% lower than the price it closed this report at so COT positions are certainly lower, but still it looks like speculators are holding tight to their silver positions - which is bearish from a contrarian point-of-view.

Asian Gold Premiums Jump

As we mentioned earlier one thing we do look for as a bullish indicator is Asian gold premiums as they signal important physical gold buying. Investors need to remember that while speculators can easily push around the gold market with billion-dollar paper gold trades, the physical market is what underlies the paper market and it is many degrees smaller.

That means moves in the paper market eventually catch up to the physical market, so in our view physical premiums represent a future indicator for the gold price, thus we pay attention to them and give them a lot of weight when making short-term gold trading decisions.

Evidently, gold demand picked up slightly across Asia this week, fueled by a drop in international prices as the dollar gained on expectations of a near-certain increase in U.S. interest rates, traders and market participants said:

In top consumer China, physical demand for gold has been strong, traders said, with premiums quoted between $15 and $17 an ounce over international spot prices, as against the $9-$12 levels seen last week. "We are starting to hear clients coming and enquiring about inventories, so we expect physical demand to increase," said Brian Lan, managing director at Singapore-based gold dealer GoldSilver Central.

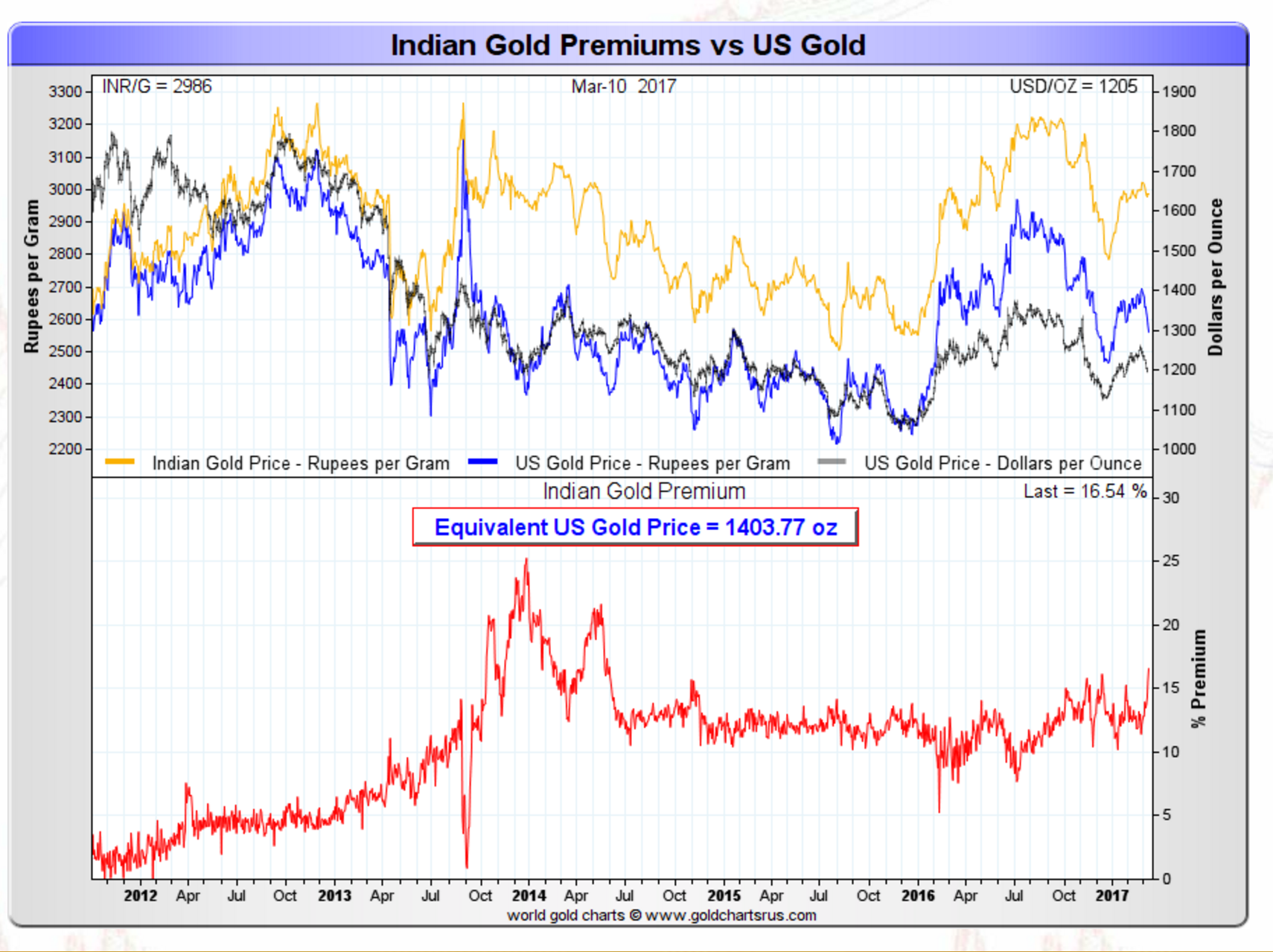

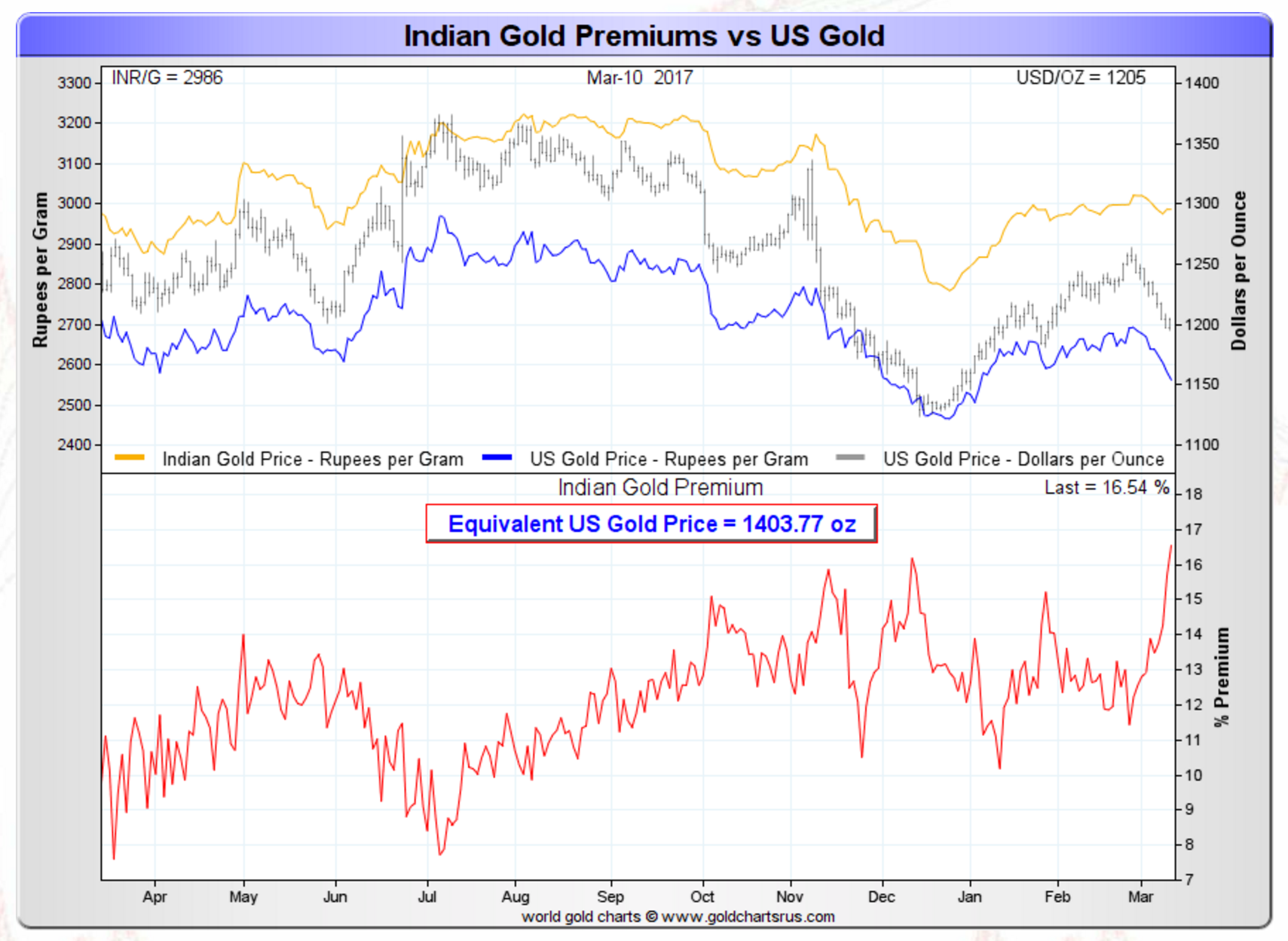

Indian premiums also surged to some of the highest levels we have seen in the past few years, as can be seen in the long-term and short-term gold premium charts below.

Source: GoldChartsRUS

This is good news for gold bulls as this physical buying can absorb some of the ETF and speculative selling that we have seen and certainly can affect the short-term psyche of gold traders to reverse some of that bearish sentiment.

Our Take and What This Means for Investors

Now that a March rate hike is priced in by pretty much all market participants and should be no surprise when the Fed meets next week, our short-term view on gold is getting a bit more bullish as some speculative traders sell out and the potential negative consequences of the Fed move start to dawn on participants. Rising physical market premiums also mean that we have a margin of error when dipping our toes back into the gold market with short-term trades.

Our short-term position of gold is shifting from a bearish position that we have had over the past few weeks to a more neutral short-term position. Since we are still very bullish on gold for the medium to long-term, we are now buying back some of our previously sold gold positions with the expectations that we could see further selling in gold.

As for silver, we remain on the sidelines for the short-term as we still believe the speculative and ETF positions are too high for our comfort levels. With a rise in gold, silver may rise as well but the risk-reward here is less comfortable for us than in gold, we will sacrifice some of the potentially superior returns in silver to focus on more conservative gold. But we do note that with a further decline in silver to the lower $16 levels, it may become much more attractive to start building back positions.

In summary, we are starting to buy back some of our previously sold gold positions with this recent drop but we are keeping some powder ready for further drops in gold especially with a bearish knee-jerk reaction to Wednesday's Fed meeting statement. Thus we think investors should considering increasing their positions in the miners and gold ETFs, like the SPDR Gold Trust ETF (NYSEARCA:GLD), and ETFS Physical Swiss Gold Trust ETF (NYSEARCA:SGOL). For silver, we are still not ready to really begin aggressively adding to our positions in the ETF's like the iShares Silver Trust (NYSEARCA:SLV), ETFS Silver Trust (NYSEARCA:SIVR), and Sprott Physical Silver Trust (NYSEARCA:PSLV), as gold simply has a better risk-reward profile at the current time but with a further drop in silver we may consider buying back some of our previously sold positions.

0 comments:

Publicar un comentario