Global reflation continues into 2017

by: Gavyn Davies

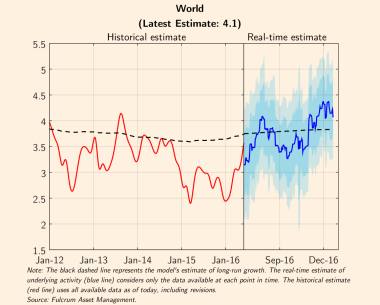

As the global economy enters 2017, economic growth is running at stronger rates than at any time since 2010, according to Fulcrum’s nowcast models. The latest monthly estimates (attached here) show that growth has recovered markedly from the low points reached in March 2016, when fears of global recession were mounting.

The financial markets have, of course, responded powerfully to the change in global growth, which was first picked up by the nowcast models in mid year. As the FT’s John Authers points out in his entertaining article on Hindsight Capital, the winning trades in the second half of the year were all linked to the theme of global recovery and reflation.

Equities outperformed bonds, cyclicals outperformed defensives in the equity markets, industrial metals rose relative to precious metals, Japanese equities surged and German bunds fell back. In all cases, these trades started to perform well in July, and they enjoyed a powerful acceleration in November and December, presumably driven by Donald Trump’s election victory as well as stronger economic data, notably in business and consumer surveys.

The big questions at the start of 2017 are whether the markets have now fully responded to the reflationary trends in global economic data, and to expectations of a policy bias towards stronger growth from the Trump administration.

Policy and Growth

The key upcoming event on economic policy is, of course, the incoming US president’s inauguration address on 20 January, when the likely balance between “good Trump” (tax cuts, infrastructure spending and deregulation) and “bad Trump” (protection and increased geopolitical risks, especially with regard to China) will be reassessed.

Markets certainly seem to be priced for a very favourable outcome on the US policy mix — perhaps too favourable. The possibility that Mr Trump will label China as a “currency manipulator” early in his administration looms as a serious risk to buoyant financial markets in coming weeks.

On global growth, however, there has been no sign yet of any impending slowdown. Consensus forecasts for global GDP growth were revised downwards early in 2016, with the largest downgrades coming in the US, where business investment once again disappointed the optimists. After February 2016, however, the pattern of downgrades was broken, and growth forecasts stabilised for the first time in several years.

In assessing the future of the “reflation trade”, it is important to watch two factors: whether activity nowcasts are beginning to lose momentum, as they have done repeatedly during the faltering global economic recovery after 2009; and whether asset prices cease responding to good news on activity, suggesting that investors’ expectations have run ahead of themselves.

We have not seen either of these danger signals yet. The GDP forecasts produced by the nowcast models suggest that the most likely outcome for the 2017 calendar year is that consensus GDP forecasts will need to be upgraded, for the first time in many years. Although we would not place too much weight on these statistical predictions for more than a few months ahead, they are just as valid as mainstream forecasts produced by large-scale econometric models, or by expert opinion in the financial sector, if not more so.

Economists have always found it very difficult indeed to predict major cyclical turning points in activity, which is why the markets are so sensitive to changes in incoming data. These are best tracked through the nowcasts.

Growth running above trend, especially in the advanced economies

The growth rate in global economic activity is currently running at 4.1 per cent, compared with an estimated trend rate of 3.8 per cent. This represents a vast improvement on the growth rates recorded in 2015 and early 2016, when growth dipped to below 2.5 per cent at times. As noted in last month’s report, the global rebound since early 2016 has been broadly based, with all the main regions contributing to the improvement. The breadth of the acceleration is encouraging, compared with previous episodes since 2010, when improvements have been more narrowly based, and have quickly petered out.

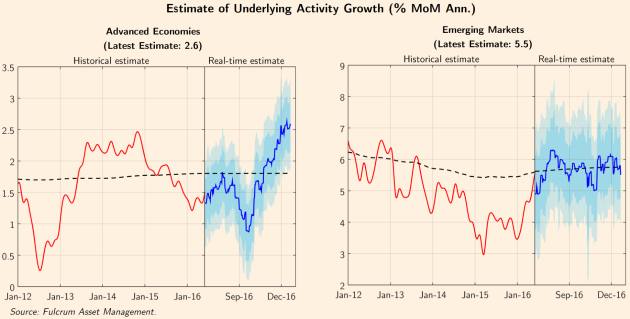

In recent months, activity in the advanced economies has continued to improve markedly, while activity in the emerging markets has been steady at around trend rates. The latest estimate for the AEs shows activity growth running at 2.5 per cent, a rate achieved only rarely during the post-crash economic expansion.

Meanwhile, the EMs are growing steadily at close to their 6 per cent trend rate. Recent growth rates have been about 2 percentage points higher than achieved in 2015. The EMs have therefore ceased to be a drag on the global expansion, thanks to stabilisation in Russia and Brazil, and to above-trend growth following the policy stimulus in China.

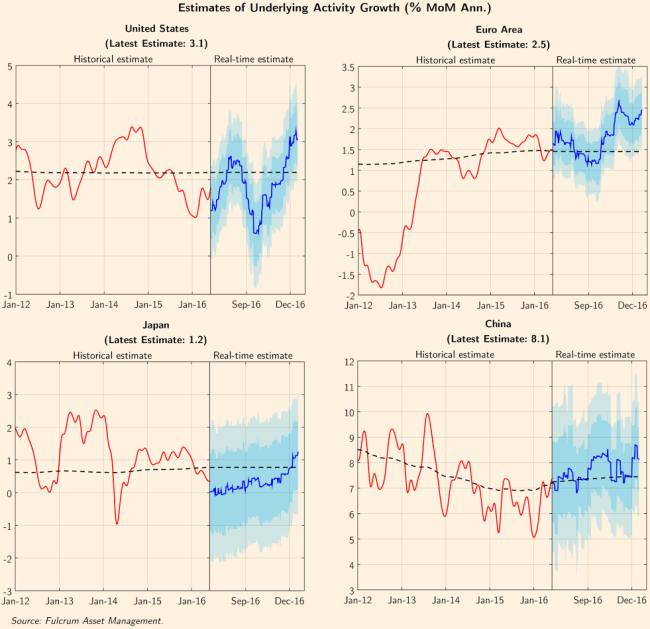

The US leads among the major advanced economies…

Within the AE block, the rise in activity growth in the US late in 2016 has been particularly impressive. Although this has been evident more in survey data than in “hard” economic data, the nowcast models have found that surveys have been reliable early indicators of changes in the activity growth rates in the past.

Furthermore, according to Jan Hatzius at Goldman Sachs, financial conditions in the US will remain positive for growth at least until mid 2017, despite impending tightening by the Federal Reserve. After that, the likely fiscal stimulus by the Republicans will begin to support the economy.

In the eurozone, expansionary monetary policy by the European Central Bank is set to continue for most of 2017, and fiscal policy has turned modestly expansionary. In China, policymakers may rein back the 2016 stimulus to credit and fiscal policy, but there is unlikely to be any major reversal of policy ahead of the 19th Communist Party Congress in the autumn.

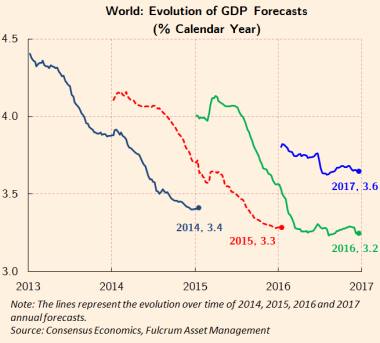

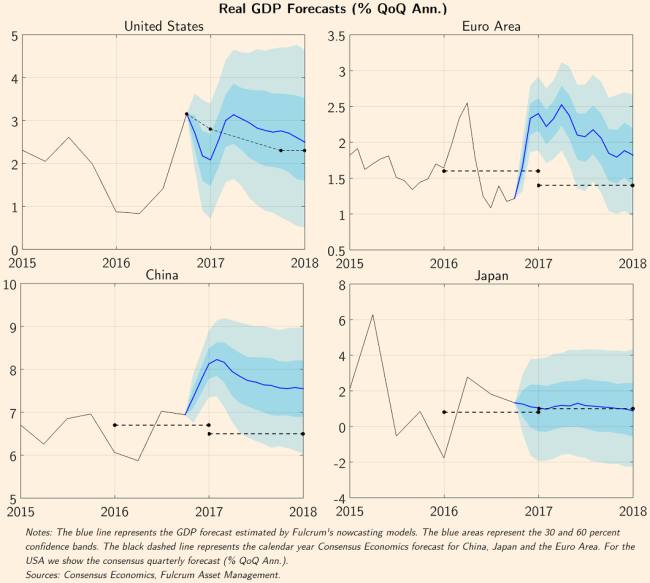

Forecasts for 2017 from the nowcast models

Finally, the latest set of forecasts derived from the nowcast models for 2017 are shown below.

As noted above, these are “statistical” predictions that are not derived from fully specified macroeconomic models (and therefore make no attempt to allow for policy changes and other economic events exogenous to the nowcasts), but they can be useful in providing a guide to likely revisions to consensus GDP growth forecasts in the months ahead.

On this occasion, they seem to suggest fairly clearly that upgrades are more likely than downgrades in the US, the eurozone and China during the first half of 2017.

If this occurs, there may be further room for the reflation trades in the financial markets to perform well for a while longer — unless a protectionist American president upsets the apple cart.

0 comments:

Publicar un comentario