2017 Outlook - Unbreakable

by: Eric Parnell, CFA

Summary

- Is the U.S. stock market a superhero? Is it unbreakable?

- The Superman II dilemma.

- Implications for 2017.

- The Superman II dilemma.

- Implications for 2017.

"Are you ready for the truth?"

- Elijah Price, Unbreakable, 2000

Is the U.S. stock market a superhero? It sure seems like it given its remarkable performance throughout the post financial crisis period. For no matter what challenges has confronted it along the way, the U.S. stock market has overcome to advance to new highs. But with each passing year, both the market valuations and the risk stakes become increasingly higher. Will the U.S. stock market prove itself to be truly unbreakable in 2017? Or will it eventually drown under a flood of pressures that finally become too insurmountable to overcome?

A Legendary Tale

Upon reflection, the journey of the U.S. stock market over the past several years has been truly remarkable. For it was not all that long ago from the summer of 2007 through March 2009 when a banking car wreck nearly collapsed the global financial system. One might have reasonably expected emerging from a near death experience that those participating in the U.S. stock market might require deeply discounted valuations for years after the trauma of watching the value of their investments evaporate so quickly before their eyes.

But not so for the U.S. stock market. Not only did it quickly become comfortable with returning to premium valuations, but it has hardly skipped a beat in moving to the upside in the eight years that followed. From Latvia to Dubai to Greece to Italy and Spain to Crimea to Greece to Brexit to Trump to Italy just to name a few headline grabbers along the way, each and every time U.S. stocks paused, shrugged momentarily, and subsequently surged to the upside.

"Do you know what the scariest thing is? To not know your place in this world. To not know why you're here."

- Elijah Price, Unbreakable, 2000

The S&P 500 Index (NYSEARCA:SPY) is the proverbial David Dunn of global capital markets. If it took human form and loaded onto a train with 131 other passengers, it would emerge completely unscathed from the tragic accident that follows. In fact, it would likely use the occasion to rally further to the upside.

But what has become increasingly scary when looking forward for capital markets is the following. Exactly why do U.S. stocks find themselves here today? Is it truly immortal? Or does it find itself where it is today for reasons much like the technology and housing bubble that are a total fantasy and may ultimately prove unsustainable in the end?

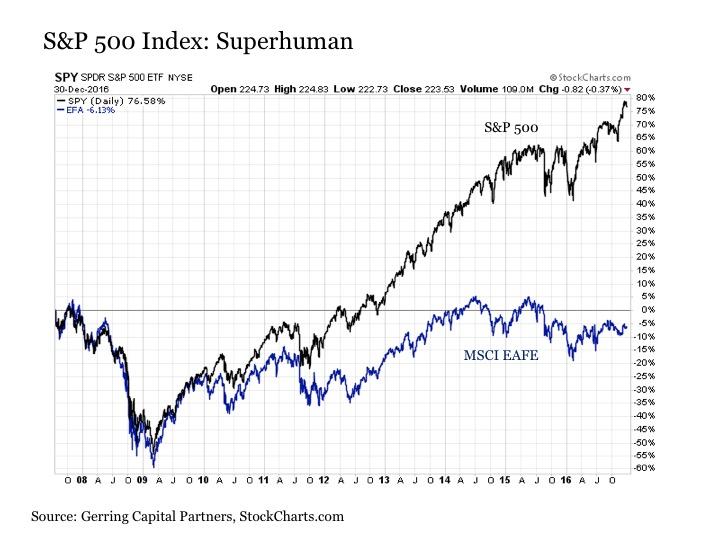

What makes the U.S. stock market including the S&P 500 Index truly stand out as superhero is how it has performed during the post crisis period versus the rest of the world. From the moment when the financial crisis started to seep into capital markets on July 19, 2007 through today at the end of 2016, the S&P 500 Index is now more than +75% above its pre-crisis highs.

The mere mortal developed international stock market as measured by the MSCI EAFE Index (NYSEARCA:EFA), however, is still lower on a nominal basis by a cumulative -6%.

The dampening effects of the U.S. dollar on international stock market returns, you might proclaim!

Even if you accounted for the recent strengthening of the U.S. dollar (NYSEARCA:UUP), which is easy to forget was marginally weaker on net during the post crisis period through the summer of 2014, the EFA is only marginally higher on a cumulative basis. In short, not much of a difference.

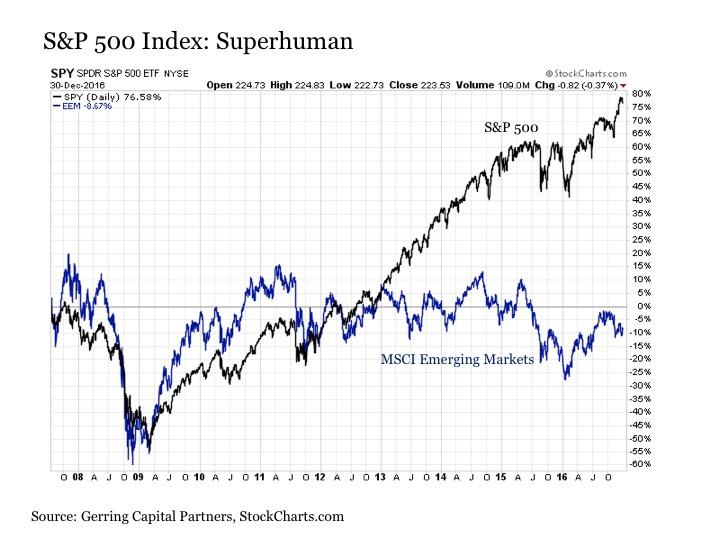

What about emerging markets and their higher economic growth rates. Mere mortals once again. For not only is the MSCI Emerging Market Index (NYSEARCA:EEM) still cumulatively lower by nearly -10% relative to where it was at the start of the financial crisis, but it has gone effectively nowhere for the past seven years and counting.

But what about the fundamentals? Isn't the superior performance of the S&P 500 Index being driven by the remarkable earnings recovery seen since the calming of the financial crisis?

Simple facts. In the third quarter of 2007, the S&P 500 Index generated as reported earnings of $84.92 per share. For the most recently completed quarter where final data is available in the second quarter of 2016, the S&P 500 Index generated as reported earnings of $86.92 per share.

In short, earnings are effectively no higher today then they were nine years ago. And these are nominal earnings readings that are not adjusted for inflation. When accounting for inflation, as reported earnings today are actually more than -10% below where they were in 2007 Q3.

Companies are effectively still paying investors less today in earnings than they were nearly a decade ago. But how much are investors willing to pay for these earnings? Back in 2007 Q3, the S&P 500 Index peaked at 1,576 and sported a price-to-earnings ratio of 18.5 times earnings, which is fairly expensive in its own right. Today, the S&P 500 Index just wrapped up 2016 at 2,238, which has its price-to-earnings ratio at a much more remarkable 25.8 times earnings, which is among the highest levels in the recorded history of the U.S. stock market.

Put simply, the superhuman rally in U.S. stocks throughout the post crisis period has had much less to do with fundamentals. In fact, fundamentals are arguably worse today. Instead, what is more true is that stocks across the rest of the world are reflecting the broader economic reality of a tough slog these last many years, while U.S. stocks find themselves magically floating through the stratosphere despite the lackluster fundamentals. As a result, U.S. stocks find themselves second only to Denmark as the most expensive stocks in the world on both a 10-year cyclically adjusted price to earnings (CAPE) and price-to-book value basis.

But don't the historically low bond yields help explain why U.S. stocks can sport such premium valuations today? Perhaps, but historical precedent tells a different story. For bond yields were just as low throughout the 1940s and 1950s, yet stock price-to-earnings ratios remained consistently in the high single digits to low double digits. And this was during a time period of consistently strong economic growth unlike today.

"Can I tell you a secret? I'm going to be very, very sad if this doesn't work out the way I think."

- Elijah Price, Unbreakable, 2000

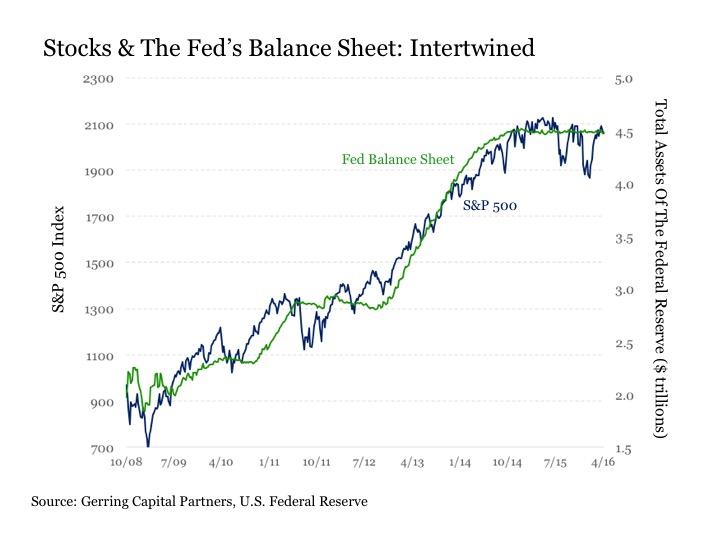

Of course, it is no secret that the yellow sun that has shined on U.S. stocks throughout the post financial crisis period has been the steady flow of stimulus from global central banks.

Up until the end of 2014, it was the U.S. Federal Reserve that was doing the stimulus pumping.

And in the years since, it has been the Bank of Japan and the European Central Bank that has been providing the power.

The plan all along? Artificially inflate asset prices so that wealthy investors would realize the gains and trickle it down through the rest of the economy through increased consumer spending and capital investment. You know, because the artificially inflated asset prices from the tech bubble worked so well, and inflating a housing bubble in order to support the global economy emerging from the bursting of the tech bust also turned out swimmingly. Third time apparently is a charm. Except it hasn't been, as the wealthy have hoarded their stock market gains through recycling their gains back through the markets through increased dividends and share buyback activity, neither of which are productive activities that are doing anything to revive the global economy.

The Superman II Dilemma

All of this brings us to today. The U.S. stock market looks like a superhero. But its powers have been sustained all along by the steady flow of monetary stimulus from global central banks around the world. And as we enter 2017, the powers that have sent the U.S. stock market flying high into the sky are set to start going away.

The U.S. Federal Reserve finished adding stimulus more than two years ago now and is now tightening policy. According to the pundits, the Fed is expected to add two to three more rate hikes in 2017. The People's Bank of China is also out of the stimulus game, having already drained $700 billion from its own balance sheet since mid 2015. While still pumping, the European Central Bank has started tapering its asset purchase plan. And the Bank of Japan is showing increasing signs of standing down as well.

Clark Kent: "Looks like from now on you'll have to have a bodyguard with you."

Lois Lane: "I don't want a bodyguard. I want the man I fell in love with."

Clark Kent: "I know, Lois. I wish he was here."

- Superman II, 1980

Unfortunately for many participants in the U.S. stock market, they have become so filled with the hubris that comes with the market being seemingly invincible that they now believe they can simply carry on without the super powers that have delivered U.S. stocks to such great heights.

Monetary stimulus is going away? No matter, as the baton will simply be passed from monetary policy to fiscal stimulus that will start on January 20 with the installation of a new administration in Washington DC. It is time for the markets to shed its super powers, as fiscal policy love is all that we need to save the day from here.

If only it were that easy. Remember, it was less than two months ago that capital markets considered a Trump presidency unthinkable given the policy unknowns that would come with such an outspoken individual that is previously untested in the political realm. But in the weeks that followed the election, this sentiment completely changed. All of the sudden, the new administration would be giving every investor everything it ever wanted almost immediately.

Such is the euphoria of new found love. Unfortunately for U.S. stock market investors, such love also brings with it complete delusions about reality. For thinking fiscal policy love will be enough to replace your monetary policy super powers is a good recipe for finding your once seemingly invincible portfolio suddenly bruised and bloodied in a diner in the middle of nowhere and the policy you thought you would love so much buried to death by unanticipated earthquakes both within and between Capitol Hill and the White House.

Such is the dilemma for policy makers and markets today. Before Superman took the leap and switched to mere mortal, the possibility always lingered out there that he could make a success of being "normal". But it didn't take long after taking the leap after an ill fated visit to an average diner to realize that it just wasn't going to work out. The U.S. economy and stock market are now attempting a similar leap as we head into 2017. Monetary policy makers around the world are now standing down and the U.S. stock market is now working to shed its super powers and looking to fiscal policy in trying to transition to being "normal".

Unfortunately, history offers us no past precedent of an economy that has been able to successfully make this switch, much less do so seamlessly and without a lot of problems along the way.

But unlike Superman that could simply reclaim his super powers and turn back the clock once he quickly realized the switch was just not going to work out as planned, the U.S. stock market will not have the same luxury going forward. For global monetary policy makers have already gone to this "trying to be normal" well several times in the past with jarring results. But this time around they are seemingly coming to the conclusion that supporting a U.S. stock market superhero is not only a recipe for future growth, but it is also having the negative spillover effect of helping to foster increasing income inequality and social unrest. In short, after so many stops already and more than $12 trillion in assets already added to major central bank balance sheets along the way, the Fortress of Solitude crystals well is essentially dried up for monetary policy makers at this point.

Implications For 2017

"It's all right to be afraid, David, because this part won't be like a comic book. Real life doesn't fit into little boxes that were drawn for it."

- Elijah Price, Unbreakable, 2000

As we enter 2017, the U.S. stock market super powers are quickly fading. We are now entering a juncture after so many years where it is time for the U.S. stock market to return to the real life that nearly every other asset class across capital markets have been living for so many years now. And this return to reality could not be coming at a worse time for the U.S. stock market.

For the coming year will be nowhere close to the comic book that investors have been drawing for it to close out 2016. Instead, it is bound to be increasingly messy and sometimes unruly as the year presses on.

First, we have a new administration entering the White House at the end of January that will be bringing an entirely new and untested approach to communications. While this may work out stupendously, it also runs the daily risk that a selected tweet on any given day could result in unintended consequences that could spillover into capital markets including stocks.

Moreover, no matter how much optimism some may have about the new leadership coming to Washington, it is still completely unknown how the execution of these policies will play out due to the lack of a historical track record for the President-elect. They may all go extremely smoothly and turn out even better than expected. Then again, they may turn out entirely differently and potentially negatively.

Second, we have a slate of major political elections across Europe (BATS:EZU) that, depending on how they play out in the coming months, could increasingly point to the eventual unraveling of the European Union. The Dutch (NYSEARCA:EWN) are up first in March followed by the French (NYSEARCA:EWQ) in April and May and then by the Germans (NYSEARCA:EWG) anytime between August and October. And the Italians (NYSEARCA:EWI) may also end up holding an election of their own in the coming year as well with a banking system (NASDAQ:EUFN) in the country that is teetering on the brink of contagion sparking crisis.

While superhuman U.S. stocks may have shown the power to shake off these tremors up to this point, a more mortal U.S. stock market may prove less resilient in the coming year depending on how these elections play out.

Then there is the United Kingdom (NYSEARCA:EWU), which will be initiating the process of making their exit from the European Union in the first half of 2017. While many investors proclaimed 'Brexit' a non-event for the U.S. stock market given the way it was able to shake off the outcome of the vote, the market response may be much different when the actual effects of the vote start to be felt.

Next is arguably the biggest and most important wild card of them all in China (NYSEARCA:GXC). The world's second largest economy is chock full of bubbles and distortions from debt to real estate to bond yield volatility to capital pouring out of the country.

The risk of a major policy accident coming out of China is rising dramatically, and any such impacts would not be limited to the U.S. stock market but would likely be felt negatively across various asset classes around the world including bonds (NYSEARCA:BND) such as U.S. Treasuries (NYSEARCA:TLT) and commodities (NYSEARCA:DJP) such as gold (NYSEARCA:GLD) and oil (NYSEARCA:OIL).

Another is the impact on U.S. corporate earnings from all of the uncertainty spreading across the globe coupled with the persistently strengthening U.S. dollar. For while domestic fiscal policy may be set to become more supportive at some point down the road, if global economic conditions have become more uncertain at the same time that earnings are being dampened by currency effects, such a combination is typically not a recipe for higher stock prices.

These are just a few of the many known risks confronting U.S. stock market investors as they enter 2017. And these do not account for the various unknown risks that may bubble to the surface in the coming year.

Unbreakable?

"They call me Mr. Glass."

- Elijah Price, Unbreakable, 2000

Before going any further, it is important to emphasize the following point. The U.S. stock market has saved the investing world for the past eight years since the financial crisis. It has truly been superhuman to this point. And this fact must be respected going forward. It is still a superhero until proven otherwise. For just when you're ready to count a superhero out, they overcome again and again. Thus, counting the U.S. stock market out today is in many ways just as risky as sticking with it. Investors have been well served by staying long U.S. stocks, and they should continue to do so with the appropriate portion of their investment portfolios until such time when the U.S. stock market finally shows signs of being finally defeated. In other words, now is not the time to be all in on stocks, nor has it been for some time from a risk management perspective.

But despite its persistent superhuman strength, the U.S. stock market is in a fragile state as it enters the New Year. Earnings remain lackluster despite optimistic forecasts that may or may not come to pass. Valuations remain at historical highs that are well in excess of the rest of the world. Monetary policy is quickly fading away at the same time that the fiscal policy outlook remains uncertain despite the flood of recent optimism. The geopolitical market environment is filled with risks that may become increasingly difficult to successfully navigate. And even if everything turns out better than expected, it stands to reason how much longer the U.S. stock market can maintain its relative outperformance versus the rest of the world, which is already running notably long at nine years and counting.

The number of risks for the U.S. stock market are sufficiently large and the magnitude of these risks sufficiently meaningful that attempting to predict where stocks will be 12 months from now is folly. Instead, a reasonable forecast strategy for the U.S. stock market given where we are heading into the coming year is to break the calendar into quarters, for the world may look very different come the end of March versus what it looks like today given all of the variables at work today.

And when looking out over the next three months from where we sit today, probability supports the following outcomes:

U.S. stocks over international stocks and emerging stocks (still despite the U.S. valuation premium)

Large caps over small caps (NYSEARCA:IWM)

Defensive stocks (NYSEARCA:XLP) (NYSEARCA:XLU) (NYSEARCA:XLV) over cyclical (NYSEARCA:XLI) and interest rate sensitive stocks (NYSEARCA:XLF)

Gold over stocks

Bonds (NYSEARCA:AGG) over stocks

U.S. Treasuries (NYSEARCA:IEF) over spread product

Municipal bonds (NYSEARCA:MUB) over U.S. Treasuries

Of course, given all of the outside variables coming into play in the next few months, the range of outcomes surrounding these various scenarios is much wider than normal. Just like any superhero story, unexpected events could arise at any point along the way that could upend these probabilities and lead us to entirely different outcomes. As a result, investors should be much more prepared in the coming year in particular to adjust as needed to changing market conditions than they have been in the recent past.

This leads to a key final point. Regardless of how things play out over the coming year, investors should anticipate much greater volatility (NYSEARCA:VXX) versus what we have seen to this point in the post crisis period. For when a hero is finally forced to cast off its super powers, the air of invincibility can increasingly give way to a feeling of uncertainty and unease.

And it is possible that we could begin to see these forces start to unfold as quickly as the first trading week of the New Year.

All of this highlights the particular importance of true diversification in an investment portfolio as we enter 2017 to protect against such risks. Instead of wringing one's hands the next time trouble strikes in hoping that a superhero will return to save the day, an investor can empower and protect themselves from trouble today by continuing to own stocks while also diversifying into other asset classes that can hold their own when it otherwise looks like the world may be coming to an end. This more than anything else, is the best strategy heading into what may be an eventful and exciting year in 2017.

0 comments:

Publicar un comentario