What Happens If The Euro Collapses?

by: Jesse Moore

- Economic struggles and political divides are largely due to ECB policy.

- If the Euro were to dissolve in a way that left much of the EU structure intact, the whole continent would be for the better.

- If the Euro were to dissolve in a way that left much of the EU structure intact, the whole continent would be for the better.

Earlier this week, I penned an article that discussed the implications of negative yielding corporate bonds to European unity (NYSEARCA:VGK). Despite the issuance of negative yielding debt by both a German and a French company, the answer is not quite clear why.

Sure, the ECB is purchasing large chunks of corporate bonds which will inevitably push down rates, but they are also not the only game in town (for now).

What is more likely is that investors, not including the ECB, are betting on the safety of French and Germany currency conversions in the event of a stage left exit of the euro. In this article, I will explore what the disbanding of the euro might look like.

..

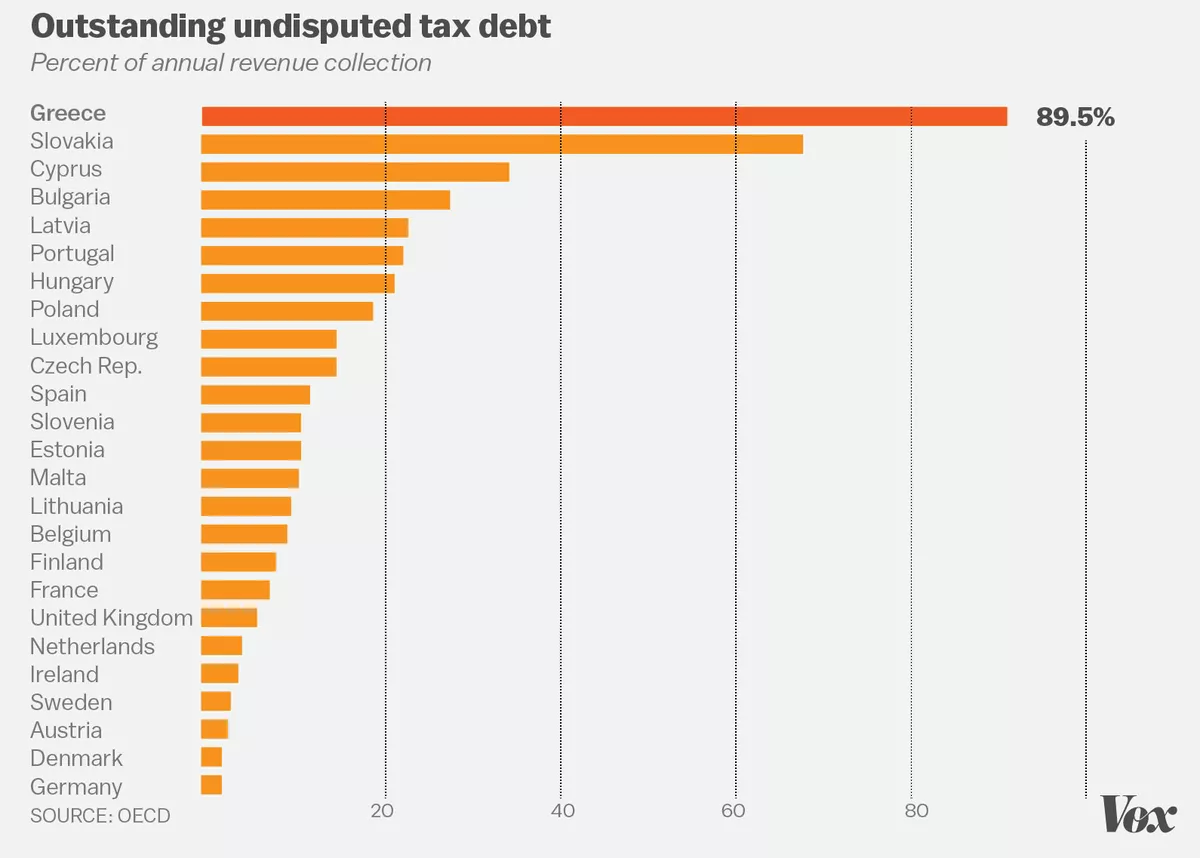

It's charts like these (via Vox) that make the frustrations painfully obvious

If the Euro Is Replaced

If the EU breaks the euro, it is unclear what the next steps would be, but it would almost certainly result in the replacement of euro deposits with national currencies. To be sure, this isn't to say that the Eurozone would collapse, an unlikely short and medium-term event; but the removal of the Euro is a very real possibility. Despite being a likely long-term positive, redenomination to national currencies would cause severe pain for EU members and influence both foreign countries, and foreign exchange markets.

Countries will attempt to redenominate their currencies in a way that best benefits their debt/account surplus. Political pressure would mount against the EU. However, disabling the Schengen zone would not be required (or practical). If the euro were to dissolve in a way that left much of the EU structure intact, the whole continent would be for the better.

The Divisiveness of the Euro

Much of the immediate European issues could be softened with a replacement of the single currency.

In the long run, the problems could be solved entirely. I have long discussed the issues with a monetary union without fiscal union, and the inevitable division of states that vastly disagree with economic policy. I view a redenomination as a very real possibility, and one that provides very real benefits.

As a simple example, Greece could devalue its currency to encourage growth and tourism, while Germany's currency would appreciate sharply against a basket of foreign currencies and boost spending while taming a large current account surplus due to artificially cheapened exports.

In The Days Following The Announcement

Since so many countries either utilize the euro or are pegged to the euro, there is going to need to be a stabilizing currency peg in the aftermath. Initially, currencies will need to free float to reach some quasi-equilibrium. In the long run, the most likely candidate for pegging will be Deutsche Marks. Volatility would rip through the financial markets as uncertainty explodes.

Weak European economies would see massive sell-offs in both stock and bond markets, while strong economies would likely see powerful moves upwards. The result would be an immediate money flow effect whereby wealth is transferred away from weak countries towards stable countries. German bonds would rapidly appreciate, giving them profoundly negative rates on speculation of Deutsche Mark appreciation, while Greek bonds would plummet.

Growth would certainly struggle in the short run. A sudden rise of trade barriers would occur in some countries. But, assuming that the free trade area maintains some part of its current form, this could be prevented. The hard part is doing it in a way that is politically acceptable and prevents nationalistic parties from using the volatility to make a power grab.

In the end, and assuming that a redenomination can occur without a breakup of the Eurozone and Schengen area, the whole continent could see dramatic benefits. By wrestling monetary policy, individual countries could adapt their policies to their problems. Germany and Greece sharing a monetary policy despite the macroeconomic picture is difficult - to say the least.

Wrap-Up

An EU without a euro is possible. Many countries interact in the free trade of goods without having accepted the euro. It is plausible that the EU could survive, and even thrive without the euro. The political divide between right and left, the economic gap between poor and rich, and the economic divide between stable and volatile are hampering European growth. As a result of economic struggles in Europe, much of the rest of the world will struggle as well.

I am a huge proponent of the EU; I believe the long-term benefits far outweigh the cons. I have also seen firsthand the positive effects it has on Eastern Europe. Together, Europe is stronger and more capable. However, the euro links these countries together in a way that causes division. A unified central bank can only act one way for a variety of economic situations.

The result is unintended consequences and poor performance on its actions. I hope that the issues for the euro can be solved, but I increasingly doubt that it can. Many people in this world are better off because of the EU, but the lack of unified fiscal and monetary policy will always divide the continent.

Thus, the euro deserves a good, long look in the face before citizens force a hasty decision on reluctant politicians.

0 comments:

Publicar un comentario