Has The Great Unwind Begun?

by: Lawrence Fuller

- Financial markets are reeling over fear of an interest rate increase.

- Excess reserves and weak economic data say no rate hike is in the offing.

- Today is a taste of what will happen on a much larger scale when rate hikes eventually do occur.

- Excess reserves and weak economic data say no rate hike is in the offing.

- Today is a taste of what will happen on a much larger scale when rate hikes eventually do occur.

Markets are reeling today in response to the mere suggestion by one Fed governor that a rate hike might be in the offing when the Fed meets next week. Boston Fed President Eric Rosengren said that there is a "reasonable case" for a rate hike. Stocks, bonds and commodities are all getting bludgeoned in response.

There is nowhere for investors to hide. The hunt for yield has abruptly turned into a panic for cash.

Now this is just one day, and it may reverse course in short order, but it is a reminder of how vicious the market decline was in January following the Fed's initial rate increase. Can you imagine how much turmoil two interest rate hikes might cause?

The reasons for the market decline are obvious. Investors begin to take profits in longer-term debt securities (NYSEARCA:TLT) where the greatest capital gains can be realized. Higher interest rates will erode these gains.

What begins as a ripple grows into a wave. Investors sell closed-end funds, fixed-income ETFs and other individual fixed-income securities in concert over fear of loss of principal.

Understand that in many cases fixed-income securities are losing as much value just today in percentage terms as they provide in income for an entire year.

Understand that in many cases fixed-income securities are losing as much value just today in percentage terms as they provide in income for an entire year.

The selling in the bond market bleeds into the stock market (NYSEARCA:SPY), as high-yielding dividend stocks suddenly look more expensive in a rising interest rate environment. The selling begets more selling and spreads to other areas of the stocks market, and eventually to the commodities markets.

Strategic asset allocation loses its effectiveness in this environment, because all assets are highly correlated. The only constructive aspect of today's trading is that investors can get some idea of how much risk is involved in the securities they own, for when interest rates do rise significantly, they will see far more blood in the streets than what is being seen today.

This is the ugly underbelly of the markets that central bankers have created, and it is what they fear most. For this reason, I do not think the Federal Reserve will raise interest rates next week.

Perhaps Mr. Rosengren was throwing out a feeler, as instructed by Janet Yellen, to see how markets would respond to an actual increase in interest rates. Clearly, markets would not like it. There are other reasons why a rate hike is not in the offing.

Perhaps Mr. Rosengren was throwing out a feeler, as instructed by Janet Yellen, to see how markets would respond to an actual increase in interest rates. Clearly, markets would not like it. There are other reasons why a rate hike is not in the offing.

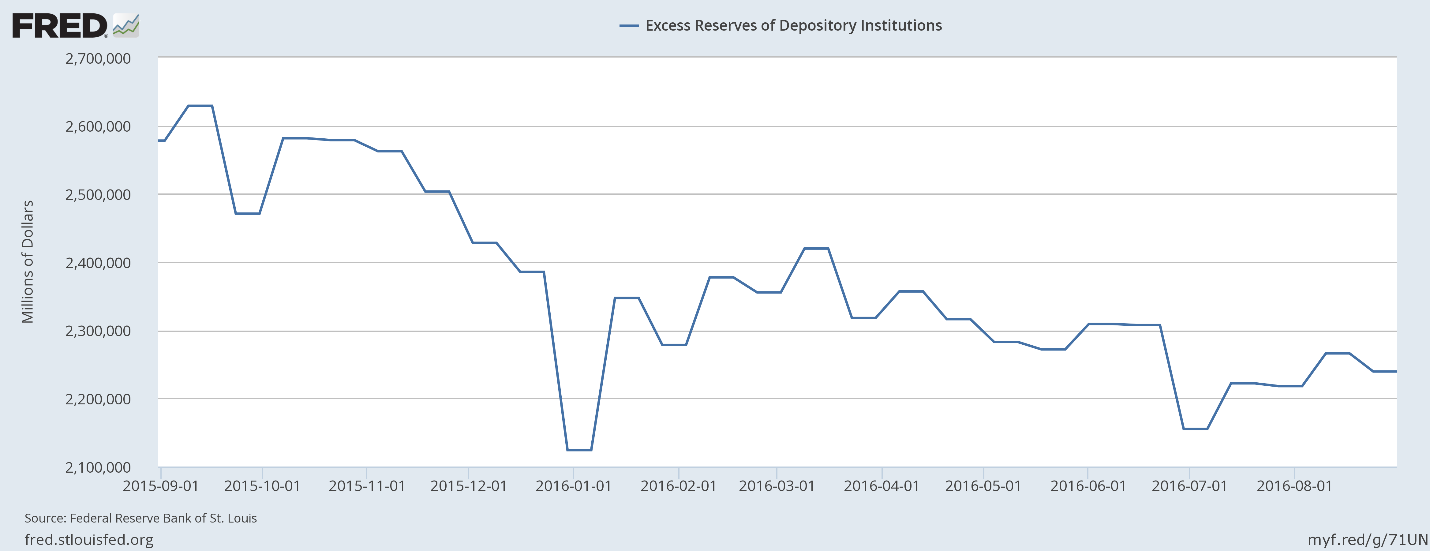

In the weeks before the first rate increase last December, the Fed significantly drained the excess reserves in the banking system, as can be seen below. Excess reserves have remained relatively stable since, and have actually increased over the past two months. This is not indicative of a rate increase.

.

Additionally, the economic data has been abysmal over the past week. The jobs report may have looked reasonably good based on the headline number, but average hourly earnings declined on a year-over-year basis to 2.4% from what was 2.7% in the month prior. We also saw the length of the workweek shrink, as hours worked fell from 34.5 to 34.3, which more than negates the supposed 151,000 jobs created.

Auto sales were very disappointing in August, falling an overall 4% on a year-over-year basis. Considering autos account for nearly 20% of retail sales, this does not bode well for the upcoming retail sales report or the overall trend in consumer spending.

Lastly, the Institute for Supply Management's non-manufacturing index was a stunner, falling to 51.4 in August from 55.5 in the previous month. This was the weakest pace of expansion for the service sector in six years! It is the service sector, led by consumer spending, that we are depending on to drive the rate of economic growth.

It is hard to believe that the Fed will ignore this extremely disappointing data. Therefore, I think Janet Yellen will come up with yet another excuse not to raise interest rates that avoids acknowledging the downturn in economic activity. This means that what is going down today will probably go back up at some point after the Fed meeting, provided there is no rate increase.

If the Fed does increase interest rates, then I think today is just the beginning of what will be a great unwind in risk assets. In that case, cash will be king, as all financial assets bear significantly more risk today than they have in a very long time.

0 comments:

Publicar un comentario