Buttonwood

Vanishing workers

Can the debt-fuelled model of growth cope with ageing populations?

THE world is about to experience something not seen since the Black Death in the 14th century—lots of countries with shrinking populations. Already, there are around 25 countries with falling headcounts; by the last quarter of this century, projections by the United Nations suggests there may be more than 100.

Such a shift seems certain to have a big economic impact, but there is plenty of debate about what that impact might be. After the Black Death a shortage of labour eventually led to a sustained rise in real wages. If that trend were repeated, it would come as a big shift after a prolonged period of sluggish wage growth, something that has fuelled political discontent across the rich world.

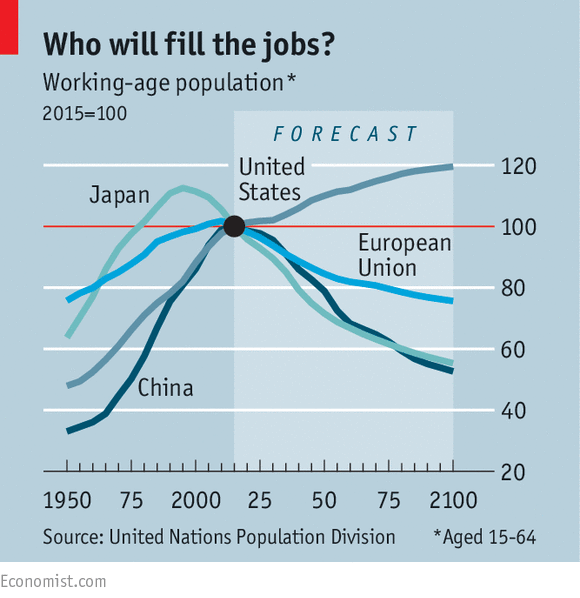

A new report on the demographic outlook by Berenberg, a German bank, focuses on one important measure: the dependency ratio. This compares the number of children and the elderly with people of working age (those aged 15-64). The higher the dependency ratio, the greater the burden on the workforce. In the world’s biggest economies, America apart, the workforce is set to shrink significantly (see chart).

.

In many developed countries, the dependency ratio rose after the second world war (thanks to the baby boom), fell in the late 1960s and 1970s as the boomers entered the workforce, and has recently started rising again. That history makes it possible to analyse how economies performed during periods of both falling and rising ratios. Berenberg based its analysis on ten rich countries: America, Australia, Britain, France, Germany, Italy, Japan, Spain, Sweden and Switzerland.

The housing market seems an obvious place to start. You would expect a growing workforce to push house prices higher, as wage-earners seek more space for their families. Sure enough, the authors find that, since 1960, the median increase in real house prices when the dependency ratio was decreasing (ie, when there were relatively more workers) was 2.7% a year. However, when the dependency ratio was increasing (ie, relatively fewer workers), real house prices fell by 0.2% a year.

Similarly, as you might expect, real GDP per person tends to grow faster (2.6%) in years when the dependency ratio is falling than in years when it is rising (1.9%). Having more workers makes it easier for the economy to grow. Inflation also tends to be higher (4.1%) in years when the dependency ratio is falling and lower (2.7%) when the ratio is increasing.

That points to a problem. In recent decades, the developed world has seen a big surge in total debt-to-GDP ratios in both the private and public sectors. People tend to take on debt for two reasons: to maintain their consumption or to buy an asset (for individuals, often a home). This requires a belief on the part of the debtor (and the lender) that, at a minimum, their future incomes and asset prices will not both fall by a lot, so the money can be paid back.

In a world of sluggish growth, low inflation and stagnant house prices, debts become much harder to pay off. Indeed, that has pretty much been the picture since the financial crisis in 2008: debt has been shuffled around a bit (from the private sector to the government) but total debt-to-GDP ratios have not fallen.

The show has been kept on the road by big reductions in interest rates, which have enabled most borrowers to keep servicing their debts. And demography suggests that the era of low interest rates is set to continue. Berenberg finds that, since 1960, real interest rates have tended to rise when the dependency ratio is decreasing and fall when the ratio is rising (as it is now forecast to do).

Low rates are in part a deliberate policy by central banks to stimulate the economy by encouraging people and companies to borrow. But as workers age, they are less likely to want to take on debt. And if an ageing workforce means slower growth, companies won’t want to borrow to invest. So the policy may not work. Indeed, the Berenberg study found that since 1960, private-sector debt rose almost three times as fast, relative to GDP, in years when the dependency ratio was decreasing than when it was increasing.

The big question is whether economic growth and rising debt levels go hand-in-hand, or whether the former can continue without the latter. If it can’t, the future could be very challenging indeed. To generate growth in our ageing world may require a big improvement in productivity, or a sharp jump in labour-force participation among older workers. To date, the signs on productivity are not encouraging and elderly employment ratios have a lot further to go.

Such a shift seems certain to have a big economic impact, but there is plenty of debate about what that impact might be. After the Black Death a shortage of labour eventually led to a sustained rise in real wages. If that trend were repeated, it would come as a big shift after a prolonged period of sluggish wage growth, something that has fuelled political discontent across the rich world.

A new report on the demographic outlook by Berenberg, a German bank, focuses on one important measure: the dependency ratio. This compares the number of children and the elderly with people of working age (those aged 15-64). The higher the dependency ratio, the greater the burden on the workforce. In the world’s biggest economies, America apart, the workforce is set to shrink significantly (see chart).

.

In many developed countries, the dependency ratio rose after the second world war (thanks to the baby boom), fell in the late 1960s and 1970s as the boomers entered the workforce, and has recently started rising again. That history makes it possible to analyse how economies performed during periods of both falling and rising ratios. Berenberg based its analysis on ten rich countries: America, Australia, Britain, France, Germany, Italy, Japan, Spain, Sweden and Switzerland.

The housing market seems an obvious place to start. You would expect a growing workforce to push house prices higher, as wage-earners seek more space for their families. Sure enough, the authors find that, since 1960, the median increase in real house prices when the dependency ratio was decreasing (ie, when there were relatively more workers) was 2.7% a year. However, when the dependency ratio was increasing (ie, relatively fewer workers), real house prices fell by 0.2% a year.

Similarly, as you might expect, real GDP per person tends to grow faster (2.6%) in years when the dependency ratio is falling than in years when it is rising (1.9%). Having more workers makes it easier for the economy to grow. Inflation also tends to be higher (4.1%) in years when the dependency ratio is falling and lower (2.7%) when the ratio is increasing.

That points to a problem. In recent decades, the developed world has seen a big surge in total debt-to-GDP ratios in both the private and public sectors. People tend to take on debt for two reasons: to maintain their consumption or to buy an asset (for individuals, often a home). This requires a belief on the part of the debtor (and the lender) that, at a minimum, their future incomes and asset prices will not both fall by a lot, so the money can be paid back.

In a world of sluggish growth, low inflation and stagnant house prices, debts become much harder to pay off. Indeed, that has pretty much been the picture since the financial crisis in 2008: debt has been shuffled around a bit (from the private sector to the government) but total debt-to-GDP ratios have not fallen.

The show has been kept on the road by big reductions in interest rates, which have enabled most borrowers to keep servicing their debts. And demography suggests that the era of low interest rates is set to continue. Berenberg finds that, since 1960, real interest rates have tended to rise when the dependency ratio is decreasing and fall when the ratio is rising (as it is now forecast to do).

Low rates are in part a deliberate policy by central banks to stimulate the economy by encouraging people and companies to borrow. But as workers age, they are less likely to want to take on debt. And if an ageing workforce means slower growth, companies won’t want to borrow to invest. So the policy may not work. Indeed, the Berenberg study found that since 1960, private-sector debt rose almost three times as fast, relative to GDP, in years when the dependency ratio was decreasing than when it was increasing.

The big question is whether economic growth and rising debt levels go hand-in-hand, or whether the former can continue without the latter. If it can’t, the future could be very challenging indeed. To generate growth in our ageing world may require a big improvement in productivity, or a sharp jump in labour-force participation among older workers. To date, the signs on productivity are not encouraging and elderly employment ratios have a lot further to go.

0 comments:

Publicar un comentario