Gold Shows Resilience Despite A Hawkish Fed - Is It Time To Abandon Our Sub-$1300 Gold Call?

by: Hebba Investments

Summary

- The latest COT data shows gold speculators pulling back modestly while silver speculators increased their bullish positions.

- None of the COT data includes the precious metals rise at the end of the week as the report is based on Tuesday's gold market close.

- Some of the reason for gold's resilience is due to paper traders questioning if the Fed has any ability to raise rates.

- None of the COT data includes the precious metals rise at the end of the week as the report is based on Tuesday's gold market close.

- Some of the reason for gold's resilience is due to paper traders questioning if the Fed has any ability to raise rates.

The latest COT report was a bit dated as it contained positions as of Tuesday afternoon, so it doesn't include any of the Federal Reserve boost that gold experienced on Wednesday or Friday's poor GDP gold price increase. Having said that, it still gives us a good feel of the trends of what speculators are doing.

We will get a little more into some of these details but before that let us give investors a quick overview into the COT report for those who are not familiar with it.

About the COT Report

The COT report is issued by the CFTC every Friday, to provide market participants a breakdown of each Tuesday's open interest for markets in which 20 or more traders hold positions equal to or above the reporting levels established by the CFTC. In plain English, this is a report that shows what positions major traders are taking in a number of financial and commodity markets.

Though there is never one report or tool that can give you certainty about where prices are headed in the future, the COT report does allow the small investors a way to see what larger traders are doing and to possibly position their positions accordingly. For example, if there is a large managed money short interest in gold, that is often an indicator that a rally may be coming because the market is overly pessimistic and saturated with shorts - so you may want to take a long position.

The big disadvantage to the COT report is that it is issued on Friday but only contains Tuesday's data - so there is a three day lag between the report and the actual positioning of traders. This is an eternity by short-term investing standards, and by the time the new report is issued it has already missed a large amount of trading activity.

There are many different ways to read the COT report, and there are many analysts that focus specifically on this report (we are not one of them) so we won't claim to be the exports on it.

What we focus on in this report is the "Managed Money" positions and total open interest as it gives us an idea of how much interest there is in the gold market and how the short-term players are positioned.

This Week's Gold COT Report

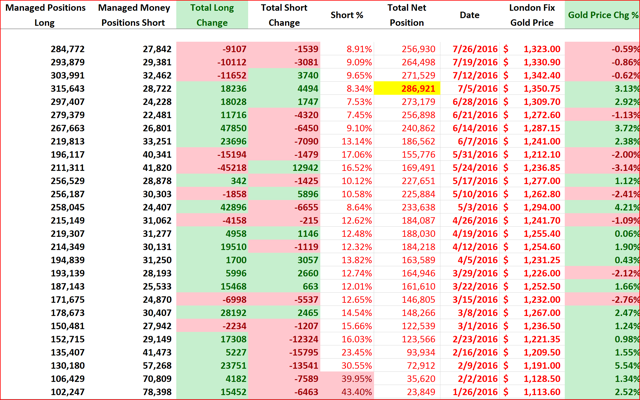

This week's report showed speculative gold longs decreased their positions for the third week in a row, while shorts decreased their own positions for the second week in a row.

It looks like a bit of the speculative froth is being taken out from the long side of things, but we do note that despite the consecutive weekly declines of around 10,000 long contracts, gold has only dropped by minute price terms when looking at it on a percentage basis - each weekly drop was less than one percent. At this point it doesn't seem that shorts are interested in going short gold as despite the drop in longs we are not seeing shorts increase their own positions.

Additionally, since none of this includes the price jumps in gold later on in the week, we probably have higher long and lower short positions as of Friday's close.

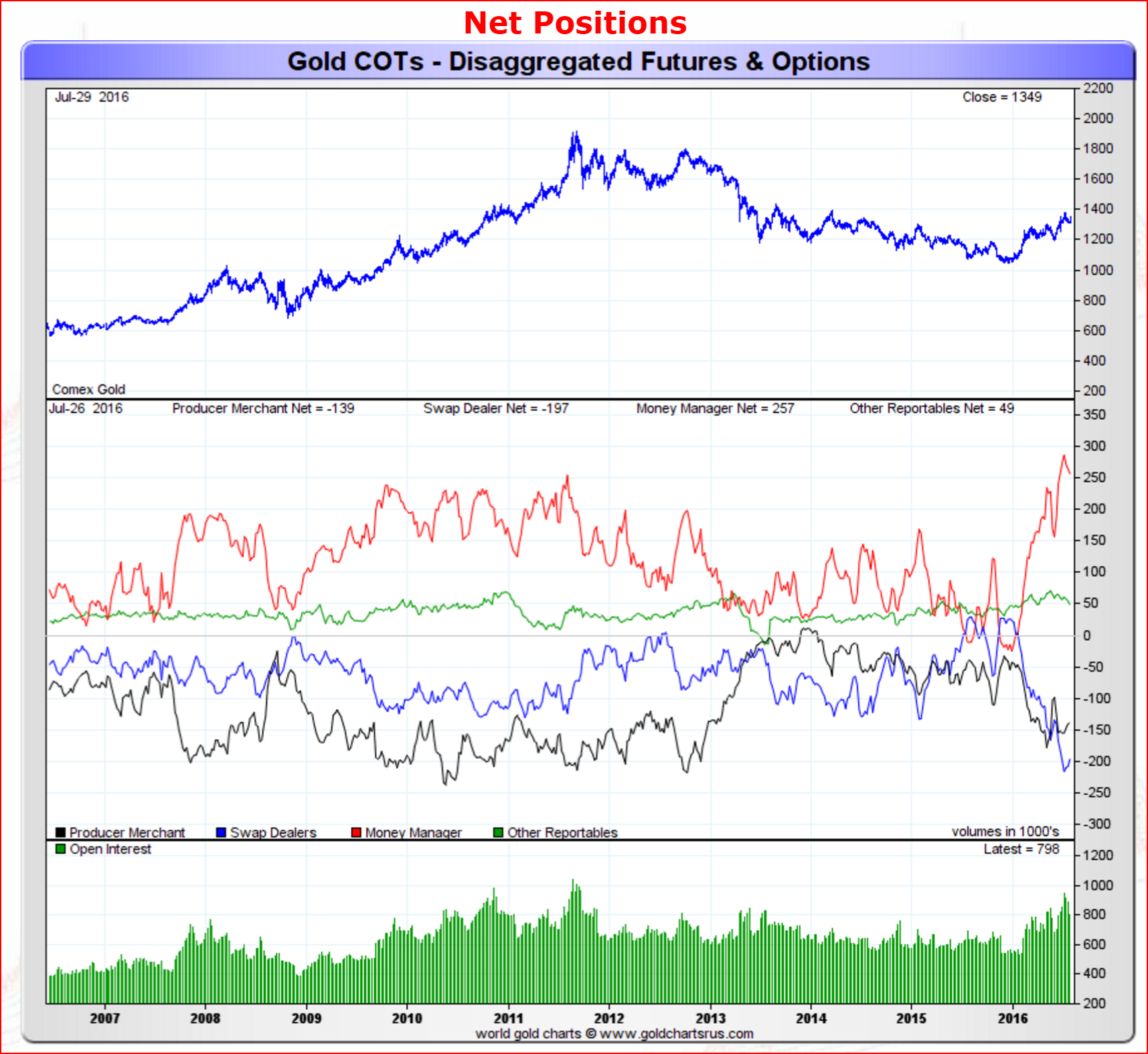

Moving on, the net position of all gold traders can be seen below:

Source: Sharelynx Gold Charts

Source: Sharelynx Gold Charts

The red-line represents the net speculative gold positions of money managers (the biggest category of speculative trader), and as investors can see, speculative traders have taken a break from their parabolic rise and sit at a net long position of 257,000 contracts.

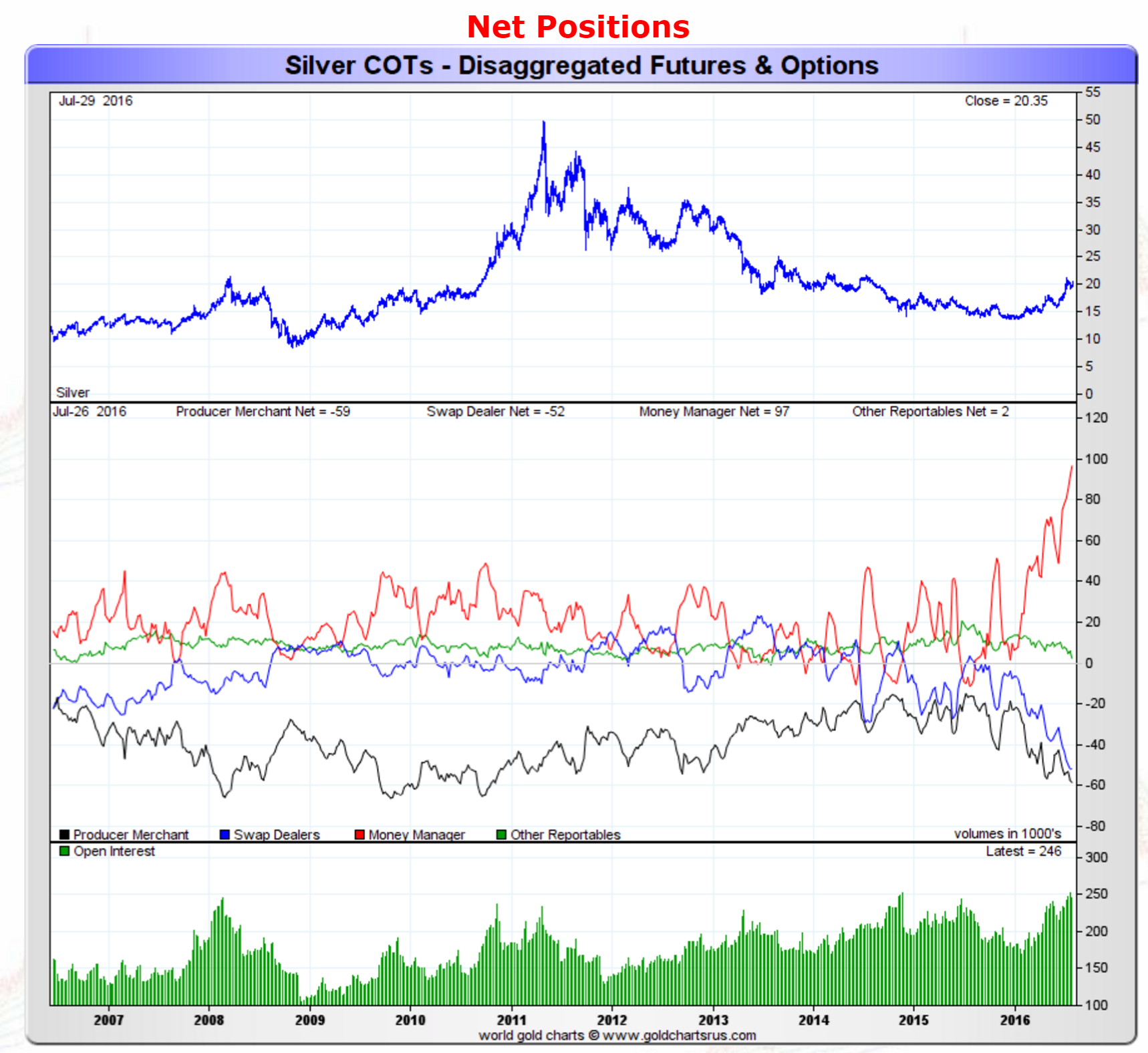

As for silver, the action week's action looked like the following:

Source: Sharelynx Gold Charts

Source: Sharelynx Gold Charts

The red line which represents the net speculative positions of money managers, increased by a little more than 5,000 contracts while shorts increased by a mere 470 contracts. Another week and another increase in the net speculative silver long positions.

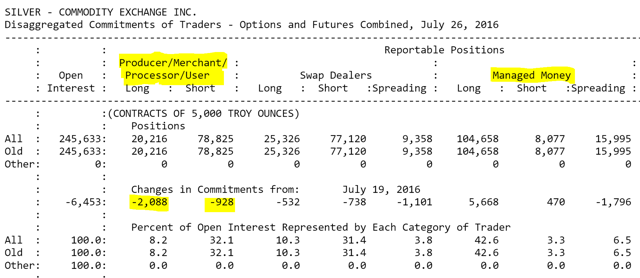

What is interesting though is that we didn't see commercials short this week's increase in speculative longs.

Source: CFTC

Source: CFTC

What is interesting about this is that usually we see Producer/Commercial short positions increase into speculative rallies - this week we didn't see that. It may be nothing or it may show that producers are reluctant to sell forward at these prices and are expecting a higher silver price, which of course would be very bullish.

Our Take and What This Means for Investors

Both gold and silver seem to show extraordinary resilience despite the extremely high speculative positions. As we mentioned last week, we are looking for a sizable pullback in gold as everyone seems to be on one side of the trade here. But after the Fed meeting, which was arguably a slight bit hawkish, it looks like gold is rising to a different tune and doesn't seem to want to pull-back.

We think what's going on here is that gold is calling the Fed's bluff and is now reacting to a Fed that it doesn't think is able to raise rates. That may explain the divergence between the physical and paper markets as paper market traders are well informed with the Fed and track it religiously (and trade accordingly), while physical buyers don't buy gold on a .25% rise or fall in interest rates. They buy because it's a secure way to store wealth and insurance for financial calamities.

Since it's obviously paper traders that are currently driving the gold price higher (evidenced by the massive net long position in the COT report), they have essentially turned gold into a proxy for the Fed's ineptitude. The Fed's weak position is driving gold higher and higher as the market no longer believe the Fed has the wherewithal or courage to raise interest rates - or at least that's what paper gold traders currently believe.

So is it time to abandon our wait for a gold pullback?

That's the important question because we are long-term gold bulls and we believe in a much higher gold price for the future. Every day is one day closer to that reality for us - and more money we leave off the table by not being fully allocated to gold and gold miners.

Currently the answer is "no" we are not ready to abandon our call for a pullback in gold that would take it below the psychological $1300 level. We are not convinced yet that the paper markets can drive gold higher without the physical markets participating, and the reported $100 gold discounts in India are not reassuring us that physical markets are hungry for gold.

We aren't stubborn though, and if we see gold continue to rise while physical demand in India and China pickup then we'll be much more open to abandoning this call. But at this point buying some of our gold-bullish trading positions with such a large amount of bulls in the trade seems very reckless and we simply don't think it would be disciplined investing.

Thus while we can't ignore gold's strength, we still do not yet think it's the time to re-initiate some of the gold positions we have sold. Thus we think investors should hold off or lighten up on gold positions in the ETFs and miners such as the SPDR Gold Trust ETF (NYSEARCA:GLD), ETFS Pxxhysical Swiss Gold Trust ETF (NYSEARCA:SGOL), and miners such as Randgold (GOLD) and Barrick Gold (NYSE:ABX).

0 comments:

Publicar un comentario