Apocalypse Never

by: Eric Parnell, CFA

- It is a question that is often raised about the second longest bull market in history.

- What exactly will be the catalyst event that will finally bring it to its end?

- Maybe it will be absolutely nothing.

- What exactly will be the catalyst event that will finally bring it to its end?

- Maybe it will be absolutely nothing.

It is a question that is often raised about the second longest bull market in history: What exactly will be the catalyst event that will finally bring it to its end? Some will even take comfort in the sustainability of the bull market by claiming they cannot envision a convergence of events that would end the rise of this relentless bull market. But when it comes to stocks, a bull typically does not meet its demise following some dramatic event. Instead, they almost always quietly pass away one trading day with little notice or fanfare at the time.

A Reflection On Past Major Market Tops

So how do major bull markets typically come to an end? What have been the apocalyptic events that have brought past roaring bulls to their knees and heralded the arrival of a new bear market phase?

A look back on market history is revealing not for the legendary incidents that have marked the end of major bull markets, but the general lack thereof.

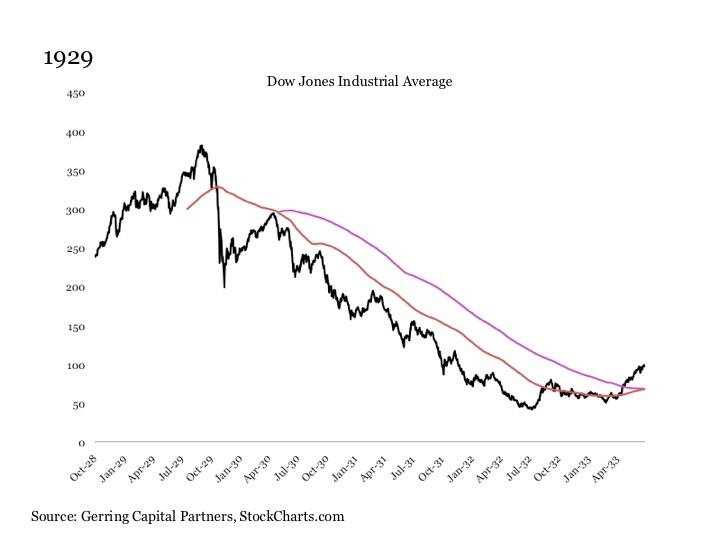

September 3, 1929

Let's begin with the granddaddy of all bull market peaks in 1929. Indeed, the bellwether event at the time was Black Monday and Black Tuesday on October 28-29, 1929, a two-day period in which the Dow Jones Industrial Average lost -23.7%, nearly a quarter of its value.

A notable event indeed. But two key points are often overlooked when reflecting on this landmark event. First, the prior Friday, October 24, 1929, did not represent the stock market peak at the time. In other words, it is not as though the stock market had surged to an all-time high the Friday before the weekend only to end up down by a quarter by Tuesday the following week. Instead, the stock market had already been rolling downhill for a fair amount of time by the time the bottom fell out.

In fact, the market peak in 1929 came nearly two months earlier, on September 3. The market moved in a reasonably tight range throughout the month of September amid what at first looked like a garden variety short-term correction in the -3% to -5% range, seemingly nothing more than consolidation of its latest strong move to the upside.

But then the momentum started to gradually pick up to the downside into October. By mid-October, the pullback from its early September highs had increased sustainably beyond the -10% range. And by Friday, October 24, 1929, the final trading day before Black Monday and Black Tuesday, the correction had just crossed over the -20% threshold. Put simply, this was a crash that was two months in the making by the time it finally erupted.

So what were the headline events that took place on September 3, 1929, that served as the catalyst for the dramatic and prolonged bear market that followed? Virtually nothing of note from a financial market standpoint. A typhoon struck the Philippines and a small plane crashed in New Mexico, but that was about it.

On September 5, 1929, two days after what would ultimately be the final peak, business theorist Roger Babson gave a speech during which he now prophetically stated "More people are borrowing and speculating today than ever in our history. Sooner or later, a crash is coming, and it may be terrific." But if I had a nickel for every time someone (including myself) made statements like this during a bull market, only to have stocks soar to new highs, I wouldn't need to bother with investing anymore, because I would be floating on a vast and growing ocean of nickels.

It wasn't until the London Stock Exchange crashed, more than two weeks after the market peak on September 20, 1929, that the situation started to unravel. But once again, how many times have we seen such supposed market traumas during bull markets, including the recent Brexit episode, only to see stocks brush it off and explode to new highs. And even after this 1929 LSE crash, stocks had recovered nearly all of any related losses associated with the event by October 10, 1929.

So what was the apocalyptic event that came to pass at the stock market peak on September 3, 1929, that ignited the relentless bear market that followed? Nothing, as the bull simply passed quietly into the night that evening.

One final point that is also often overlooked about the 1929 market peak and subsequent crash. Sure, the stock market crash of 1929 was dramatic, but markets quickly bottomed on November 13, 1929.

And over the next five months, stocks steadily rallied from these lows, posting a +50% rebound in the process. By April 17, 1930, stocks had made back virtually all of the losses suffered starting with the Black Monday and Black Tuesday crashes in late October 1929. In many ways, it looked a lot like what came after the 1987 stock market crash to that point. And along the way, bulls regained their swagger with calls that the worst was over, which of course has a similar ring to March 2008 following the demise of Bear Stearns.

It was not until April 1930, more than seven months after the bull market peak, that the lights finally went out on the market. What notable event took place then that finally took the market to its knees?

Once again, nothing.

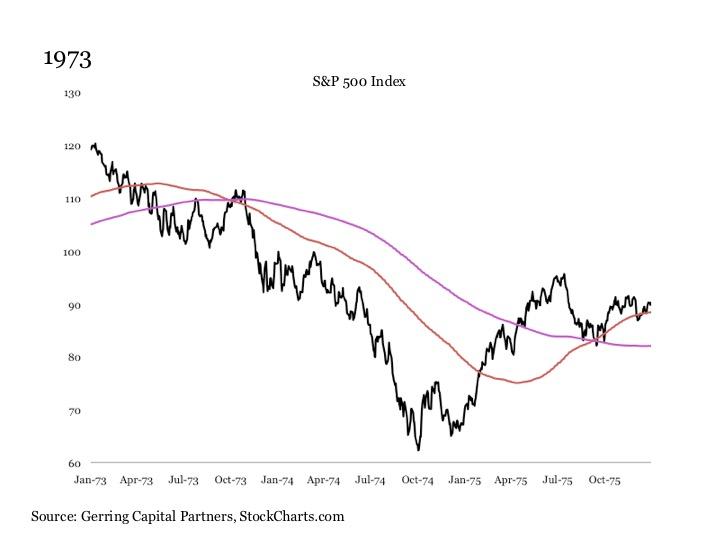

January 11, 1973

While a number of notable market peaks came between 1929 and 1973, it is worthwhile to stick with the big ones to highlight that no matter how big the bear market that follows, the peaks are not marked by any major market catalyst.

The stock market as measured by the S&P 500 Index (NYSEARCA:SPY) reached a new all-time high on a nominal basis on January 11, 1973. Notably from a historical perspective, the stock market at that point was in the seventh year of what many now refer to as a secular bear market period from 1966 to 1982, yet it reached a fresh all-time high effectively right in the middle of this phase that was roughly +30% higher than its 1966 nominal peak (does any of this sound familiar?).

So what exactly happened on January 11, 1973, that sent the stock market reeling into a near -50% correction over the subsequent two years? Once again, virtually nothing. Australia pulled out of the fight in Vietnam, but that was about it. Instead, Time magazine released an article dated three days earlier proclaiming that 1973 was set to be "a gilt edged year for the stock market". The article humorously included the following:

Most Wall Street analysts are convinced that the market will continue to climb smartly in 1973. Brokers looking for a marked increase in trading volume see signs that small investors are beginning to overcome fears instilled by the Wall Street slide of 1970 and return to the market.

Once again, does any of this sound familiar? Analysts "convinced" that stocks will continue to climb?

Cash on the sidelines with fearful investors just waiting to come back into the market?

Sometimes history rhymes. Other times, it just blatantly repeats over and over again.

But wasn't the bear market in 1973 and 1974 sparked by the OPEC oil embargo? It certainly played a part, but it was not the catalyst, as the oil crisis did not fully get underway until mid-October 1973, more than nine months after the stock market had peaked.

Once again, the market peak that came and went in mid-January 1973 was not accompanied by any notable event, much less anything that was apocalyptic.

March 24, 2000

The tech bubble had been relentlessly inflating for five years by the time the March 2000 peak arrived. Stocks had survived and thrived past the Asian debt crisis, the Russian ruble crisis, the near collapse of Long Term Capital Management and Y2K all along the way. So what were the headlines that finally inserted the pin into the massive technology bubble? Absolutely nothing.

The NASDAQ (NASDAQ:QQQ) had peaked at its all-time high exactly two weeks earlier on March 10, 2000, but the broader market as measured by the S&P 500 Index used this occasion to rally by +10% into its final peak. Simply sector rotation out of overvalued technology (NYSEARCA:XLK), media and telecom stocks into a more reasonably valued broader market, right? Not so much, it turns out.

Didn't the markets go over a cliff once the bubble burst in March 2000? Once again, no. In fact, stocks traded sideways for the next five months, supposedly a healthy consolidation of the robust gains that had come during the second half of the 1990s. And by September 1, 2000, stocks were effectively back at all-time highs. Even the tech heavy NASDAQ had bounced by an impressive +40% from its May 2000 lows and seemed poised to break out once again to the upside.

So what then happened on September 1, 2000, that finally opened the door for the bear market onslaught that followed? Nothing.

October 9, 2007

The last of our stops on our bull market peak tour brings us to October 9, 2007. The financial crisis that followed over the subsequent 18 months was arguably the most traumatic market episode since the onset of the Great Depression. But what exactly was the bell that rang at the market top in October 2007 that suggested the apocalypse was upon us? Yet again, nothing. Instead, the bull quietly expired on an intraday basis just two days after reaching its final closing peak, and the rest from there was history.

But wasn't the market starting to break apart with the onset of the financial crisis? Sure, but this was already unfolding for months ahead of the October 2007, with many market analysts proclaiming that this was nothing more than a manageable problem isolated to the housing sector and its related financing institutions. After all, noteworthy lenders such as New Century Financial had already gone under at the start of April 2007, and the two structured credit hedge funds at Bear Stearns had halted redemptions in June 2007. Yet, those investors that assumed a bearish stance in response to these early warning signs looked like idiots many months later with stocks surging to new all-time highs by early October.

And even after the market finally peaked, many were declaring the worst to be over by March 2008 as mentioned above following the coordinated transfer of Bear Stearns to JPMorgan Chase (NYSE:JPM). This supposedly signaled to the market that the policy maker backstops and bazookas would keep the market humming along. Turns out, not so much in the end.

Indeed, the collapse of Lehman Brothers is widely cited as the catalyst that heralded the financial crisis, but what is often overlooked in its aftermath is that it came in mid-September 2008, nearly a year after the market had peaked. And it did not occur in isolation, as it was accompanied by the near collapse of AIG (NYSE:AIG) and the surrender of both Washington Mutual to JPMorgan Chase and Wachovia to Wells Fargo (NYSE:WFC) in the days that followed. And even with all of this turmoil and amid a bear market that was already running at nearly a year and counting, it took more than two weeks before the markets finally responded to these shock events.

???

So here we are today, nearly a decade later. The stock market is roughly a third above its previous all-time highs despite the fact that many of the problems that sparked the financial crisis not only remain unresolved, but also in many ways have spread from the private sector to the public sector and compounded to boot. And there have been no lack of New Century Financial and Bear Stearns caliber events to the nth degree that have surfaced in the years since, yet the bull market continues to stride higher largely unfazed.

What then is likely to be the catalyst that finally brings today's bull market, the second longest in history, to its knees? It's not going to be the PIIGS, a "Brexit" announcement, or the latest tragic geopolitical terrorist event. In the end, there is likely to be no catalyst whatsoever.

Instead, today's bull market will likely quietly expire into the night just as it has in nearly every other instance in its history. And it will likely only be well into the aftermath and after so many of the losses have already been sustained before investors will be able to look back and pinpoint the true causes of what finally sent the market over the edge. Of course, for those that are watching closely along the way, it will be no mystery as to why the market has turned to the downside.

Investment Implications

It is not a question of if, but when. We know for a fact that another bear market will come in the future. The key questions are exactly when and from what price level? It could have quietly started on August 1, 2016 (highly unlikely), it could start a month from now, early next year, sometime in 2017 or perhaps three years or more down the road. There is no telling in today's liquidity fueled, policy managed markets.

But what we do know is that the risks underlying today's market are widespread and meaningful. This is not the 1950s into the 1960s or the 1980s and 1990s for that matter. These are markets that are awash with debt overseen by central bankers whose balance sheet flexibility is all but exhausted in a global economic backdrop marked by sluggish growth at best and persistent deflationary pressures. Such an environment has resulted in an increasingly restless general population worldwide that is looking toward more extreme populist and nationalist leaders to enact change on an already fragile financial system that many believe has risen at their expense and failed them as a result. In short, these are unsettled and turbulent times like the 1910s, the 1930s, the 1970s and the 2000s.

So what is an investor to do in such an environment? Sell everything and run for the bunker nestled away in the hills? Absolutely not.

The stock market is still rising. So too is the bond market (NYSEARCA:AGG). And while the commodities (NYSEARCA:DJP) market remains stuck in the dumps, the precious metals market including gold (NYSEARCA:GLD) and silver (NYSEARCA:SLV) is showing new signs of life. And until any of these markets peak, they will continue to rise and it makes sense to participate.

But just because these markets are rising does not mean that an investor should throw all caution to the wind. Participate in the ongoing gains, but do so with a relentless eye toward risk control.

Own stocks, but don't do so with 100% of your portfolio or with leverage. Instead, make it a sensible part of a broader, more diversified asset allocation. And given that we are in the second longest bull market in history, focus on stocks that have demonstrated the ability to hold up well during the early stages of a new bear market if one evening today's bull market finally expires quietly into the night.

Also own bonds. They don't need to be the boring type, but instead can include those that have some price movement in their own right. Just make sure that they move in a price path that is different than that of stocks so that you can get the true diversification benefit. In short, if you're going to own bonds in the current environment to go with your stocks, lean away from high-yield bonds (NYSEARCA:HYG) and toward Treasuries (NYSEARCA:TLT).

Also consider other asset classes. This includes precious metals, commodities, currencies and other portfolio hedges. Use these selectively and in much smaller portions relative to stocks and bonds (unless you really know what you are doing or you have an ultra-high conviction on a specific specialized theme), but use them nonetheless. For while many of these alternatives may be risky in isolation, they can actually meaningfully lower the risk of your overall portfolio when blended into a more diversified asset allocation strategy that includes stocks and bonds given the fact that they also travel on their own unique returns path.

Lastly, remain open to the idea of holding a meaningful allocation to cash at any given point in time if market conditions warrant. After all, if that older fellow from Nebraska that has seemed to do pretty well with his stock investments over the past few decades touts the mountains of cash he is holding at any given point in time, it can't be that bad of an idea. While a +0.01% return may not feel so rewarding when the market is going up +10%, it is much more so when stocks are down -20%.

And it is truly gratifying from an investment perspective than having cash at the ready to deploy after markets have gone through a healthy correction in the names that you would like to buy. After all, who doesn't like a clearance sale.

Bottom Line

Nobody knows when the bull market will finally end. But the final peak is not likely to be marked by a major catalyst event. Instead, it is likely to come and go quietly into the night one trading day.

So stay invested and participate. But also recognize where we are in the current market environment. These remain highly risky times, with pressures building with each passing day.

Stay invested, but use the powers of portfolio diversification to manage against the profound risks that could ultimately turn the market tides in a meaningful way.

0 comments:

Publicar un comentario