by: The Heisenberg

- I despise articles with titles like the one I chose here.

- But this is actually worth your attention.

- Your stocks are a slave to The People's Bank of China.

- But this is actually worth your attention.

- Your stocks are a slave to The People's Bank of China.

- I'm going to show you the most important chart in the world.

Just to be clear, I despise titles like the one that is proudly displayed at the top of this piece.

Articles that carry headlines like "Chart Of The Day" or "The Only Chart You Need If You Want To Understand…" are a lot like car accidents. You've been sitting in a long line of traffic.

You finally get close enough to the bottleneck to see the blue flashing lights. You know it's a wreck. The disabled cars are still sitting there. You drive by. You tell yourself not to look at it, but you can't help yourself. You just have to see the damage.

Articles that carry headlines like "Chart Of The Day" or "The Only Chart You Need If You Want To Understand…" are a lot like car accidents. You've been sitting in a long line of traffic.

You finally get close enough to the bottleneck to see the blue flashing lights. You know it's a wreck. The disabled cars are still sitting there. You drive by. You tell yourself not to look at it, but you can't help yourself. You just have to see the damage.

Same thing with chart posts. You read "The One Chart You Just Have To See…" in a title and you click on it. You look at the wreck. You just can't help yourself.

So that's why you're here. Well, that and you trust Heisenberg. As you should (maybe). I'm going to make it worth your time.

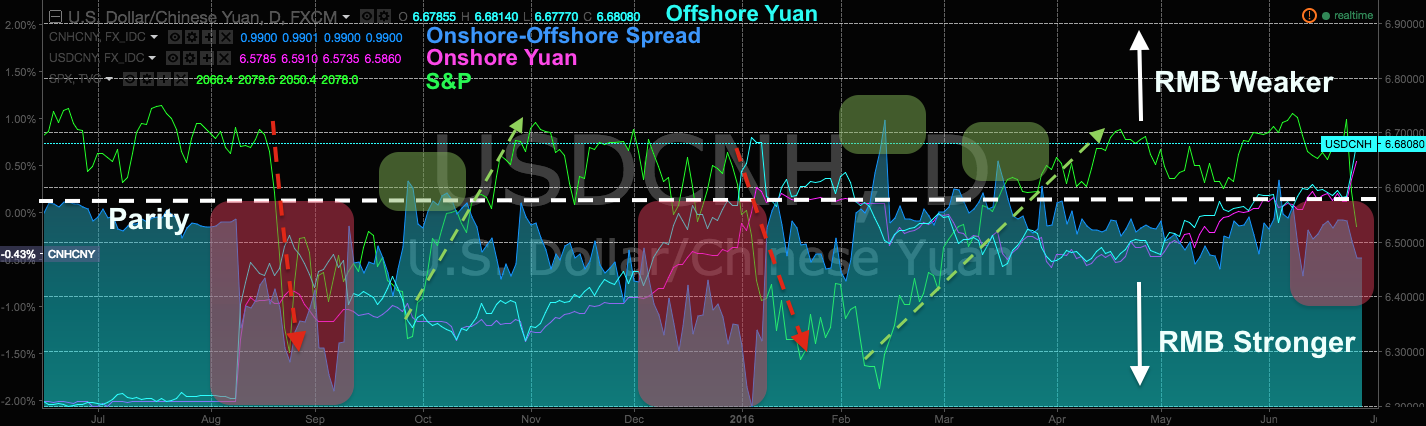

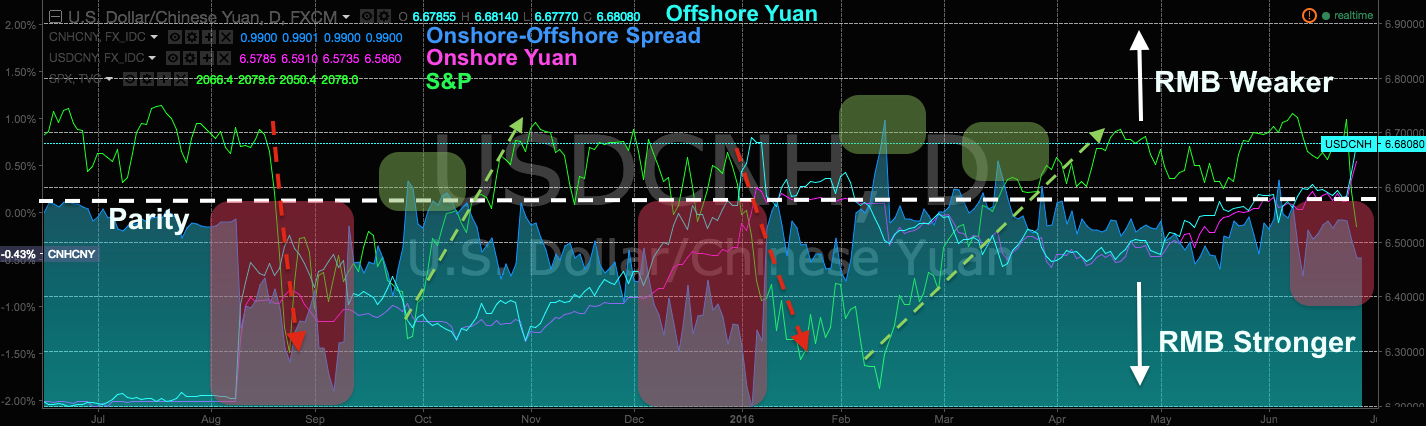

The other night I posted a chart depicting equity (NYSEARCA:SPY) futures plotted along with the onshore and offshore yuan (NYSEARCA:CYB). Now admittedly, it was kind of cryptic for anyone who doesn't spend their days and nights knee deep in markets, a lifestyle I suggest you don't try as it will quite literally drive you into the loony bin. Nevertheless, you need to understand it. So I tweaked the chart to try and show why it's so important. Here's the new, improved version:

Ok, so that looks absurdly convoluted, right? Well, it's not. I'm going to explain this in the most straightforward way possible so the next time you read about the yuan, outflows from China, US stocks, the dollar, the onshore-offshore spread, etc., you can confidently say "yeah, I get it." In the process, I'm going to skip over some of the nuance in the interest of making this accessible to everyone. I'm sure the FX traders out there will forgive me.

The yuan is pegged to the dollar. China is an export-driven economy. When the dollar rises, the peg drags the yuan higher against the currencies of China's other trading partners. That sucks if you're China (to put it colloquially). Your exports become more expensive. You don't want to completely drop the dollar peg, but you have to do something because you're still clinging to the patently ridiculous contention that your economy is growing at a 7% clip. With the Fed looking to hike (i.e. the people who print the currency you're pegged to are about to embark on a tightening cycle when your other trading partners are still easing), you have to act. And fast.

So you devalue in August ahead of the Fed meeting in September.

You devalue a little at first, and then a lot over time with some sleight of hand (e.g. adopting a trade-weighted basket as a reference and using the forwards market) in the interim, to make the transition easier.

As I'm fond of reminding investors, China didn't give the market more of a role in determining the exchange rate. They gave it less. They used to manipulate the fix to control the spot. Now they manipulate the spot to control the fix. That requires more, not less intervention. Hence the liquidation of reserves.

The market has a greater role in determining the exchange rate of the offshore yuan than it does in determining the onshore rate. That's not to say that China doesn't intervene in the offshore market (they do), it's just to say that CNH (offshore) trades more freely than CNY (onshore).

Given that, ask yourself the following question: which would you look at if you wanted to get an accurate picture of the market's outlook for China's currency? Well, you'd look at the offshore spot obviously, because it's more freely traded.

Got that? Ok, good. Now consider that markets don't really like the idea of massive capital outflows from China, a giant yuan devaluation, exported deflation, etc. etc. That's why risk sells off every time it looks like the outflows are picking up again.

Pressure on the RMB (i.e. outflows) is more accurately expressed in the offshore yuan. So, when you see the gap between the onshore and offshore yuan widen with the latter being weaker, you should read that as the market telling you the offshore rate is pricing more yuan weakness than is reflected in the manipulated onshore rate. And that's bad for risk. And stocks are a risk asset.

So having read that, look at the chart again:

See what's going on there? Let me simplify. Think of the teal shaded area as the difference between the onshore and offshore yuan. When the shaded area is below the parity line (in bold white), the offshore yuan is weaker than the onshore spot. In other words, the market is saying this: "the yuan isn't depreciating enough." Maybe conceptualize it this way: the gaps highlighted in red represent the extent to which the onshore yuan doesn't represent reality.

Now notice what happens to risk (e.g. stocks) when that gap grows. You get huge selloffs. Then notice what happens when the gap narrows and even reverses as the offshore yuan trades stronger than the onshore (highlighted in green). You get big rallies.

Knowing all of that, can you look at the chart and discern why the S&P has essentially been stable and the waters have been largely calm since the bounce off the February lows? Look at the teal shaded area from March until now. See how it's far more stable than it was last year and into the start of 2016? And note how the S&P (bright green line) has remained largely stable too.

Yeah, that's no accident.

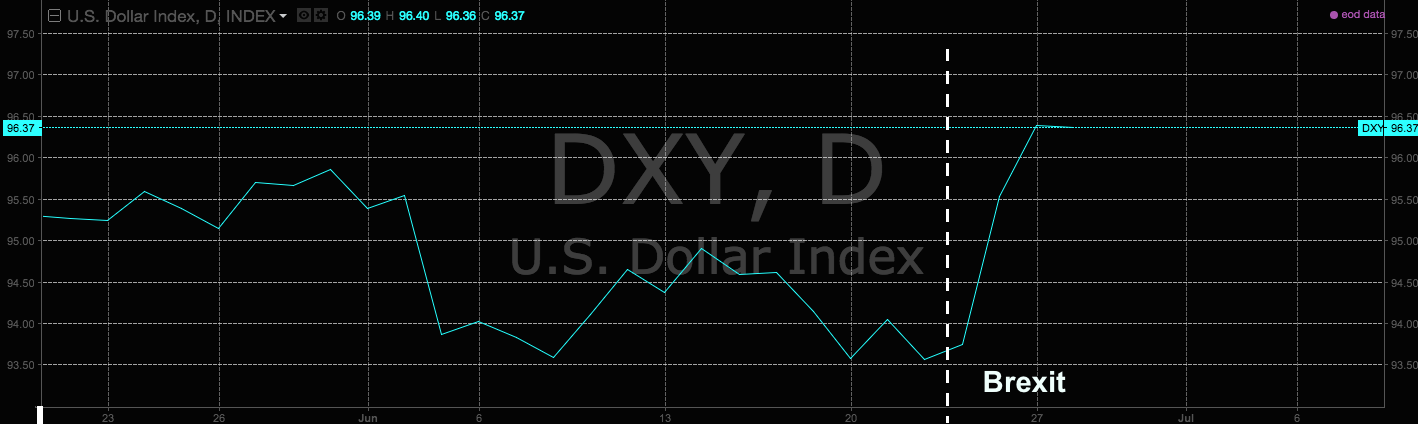

Here's a bit of color from Bloomberg on recent market action:

China weakened its currency fixing [on Monday] by the most since last August as global market turmoil spurred by Britain's vote to leave the European Union sent the dollar surging.

The resurgence in the dollar is threatening to upend China's dual strategy of allowing limited gains versus the greenback to combat capital outflows, and guiding depreciation against the currencies of trading partners, which helps exporters. The yuan has dropped almost 10 percent versus a basket of peers since its August peak.

"There is increased risk of outflows," said Khoon Goh, head of Asia research at Australia & New Zealand Banking Group Ltd. in Singapore, who is reviewing year-end forecasts for the yuan. "Authorities could intervene to limit the extent of yuan weakness, as they have before and ensure current capital outflow measures are being enforced."

So there's much more to this including how China is trying to guide the yuan lower against the trade-weighted basket while simultaneously keeping things relatively steady versus the dollar and I'll tie that in later, but for now, here's what you should do: note the widening gap highlighted in red (in my chart) after Brexit, then consider the following two headlines from Monday along with one last graph:

- CNH -0.7% to 6.6843/USD in NY afternoon, lowest since Jan. 11

- China Weakens Yuan Fixing by 0.9%, Most Since August

0 comments:

Publicar un comentario