by: Hebba Investments

.

- The speculative trader net long position in gold continued to rise with the gold price.

- This week's report was based on Tuesday close and since gold is much higher we expect traders to be even more net long next week.

- Historically it took a few weeks after the COT speculative net long high was reached before the gold price started to drop.

- This may make a good reason for traders to ride gold even higher. As disciplined investors, we cannot jump into gold now with such a large net long position.

- This week's report was based on Tuesday close and since gold is much higher we expect traders to be even more net long next week.

- Historically it took a few weeks after the COT speculative net long high was reached before the gold price started to drop.

- This may make a good reason for traders to ride gold even higher. As disciplined investors, we cannot jump into gold now with such a large net long position.

In the latest Commitment of Traders report (COT), we saw the speculative positions in gold and silver rise with the surging precious metals prices. While we were not surprised in the rise in speculative gold positions after the Brexit vote (this is the first report after Brexit), we were surprised that we didn't see much of an increase in Commercial shorts - a good sign for the bulls.

We will also take this opportunity to take a look at some of the ETF flows, which have been driving gold demand over the past few months. We will get a little more into some of these details but before that let us give investors a quick overview into the COT report for those who are not familiar with it.

About the COT Report

The COT report is issued by the CFTC every Friday, to provide market participants a breakdown of each Tuesday's open interest for markets in which 20 or more traders hold positions equal to or above the reporting levels established by the CFTC. In plain English, this is a report that shows what positions major traders are taking in a number of financial and commodity markets.

Though there is never one report or tool that can give you certainty about where prices are headed in the future, the COT report does allow the small investors a way to see what larger traders are doing and to possibly position their positions accordingly. For example, if there is a large managed money short interest in gold, that is often an indicator that a rally may be coming because the market is overly pessimistic and saturated with shorts - so you may want to take a long position.

The big disadvantage to the COT report is that it is issued on Friday but only contains Tuesday's data - so there is a three day lag between the report and the actual positioning of traders. This is an eternity by short-term investing standards, and by the time the new report is issued it has already missed a large amount of trading activity.

There are many different ways to read the COT report, and there are many analysts that focus specifically on this report (we are not one of them) so we won't claim to be the exports on it.

What we focus on in this report is the "Managed Money" positions and total open interest as it gives us an idea of how much interest there is in the gold market and how the short-term players are positioned.

What we focus on in this report is the "Managed Money" positions and total open interest as it gives us an idea of how much interest there is in the gold market and how the short-term players are positioned.

This Week's Gold COT Report

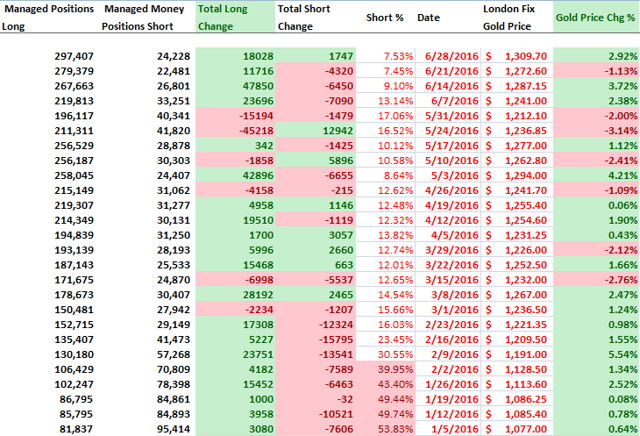

This week's report shows another huge increase in gold speculators while shorts also slightly increased.

As investors can see, for the fourth week in a row, speculative longs increased their positions by 18,028 contracts with the Brexit results and a rising gold price. While it is not surprising to see this increase, we were actually expecting a much larger increase in speculative longs as we saw a large increase in the gold price. This suggests much of the rising gold price may not be COT speculative positions - others are buying gold.

Also, the increase in shorts was a bit unusual as they also increased by a little over 1,700 contracts. The last time we saw short positions increase despite a greater than 2% move in the gold price during the week was in early March (3/8 report) - which marked a short-term high in the gold price.

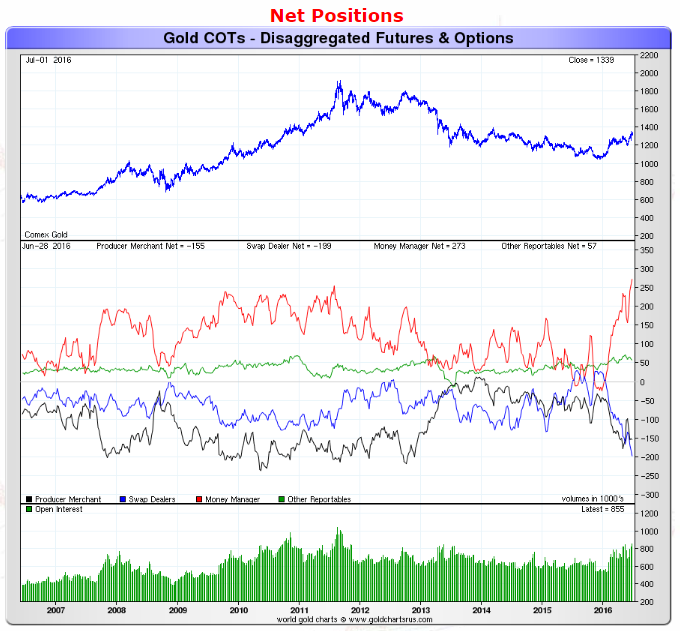

The net position of all gold traders can be seen below:

Source: Sharelynx Gold Charts

Source: Sharelynx Gold ChartsThe red-line represents the net speculative gold positions of money managers (the biggest category of speculative trader), and as investors can see, we are well above anything that we have seen previously in this report and well above the $1900 gold high from 2011. Speculative gold longs are now net long of gold by 273,000 contracts.

Additionally, this new record high was achieved with a gold price of $1309.70 per ounce and since the gold price is almost $40 higher, we're probably at an even higher speculative net long position.

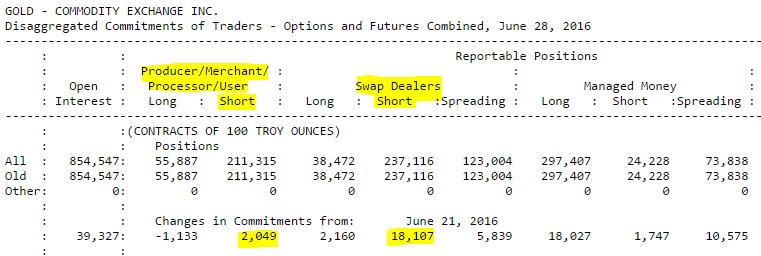

Before we move on to silver, another interesting tidbit from this report was that we didn't see what we expected to see in commercial traders. Instead of seeing a large increase in short positions to correspond to the rising gold price (commercial hedging), we actually saw a minimal move in their positions at just over 2,000 contracts.

Source: CFTC

Source: CFTC

The real action was in the Swap Dealers short positions as they surged by over 18,000 contracts to mirror the rise in speculative longs. What does this mean?

First let us understand whom the categories represent. The Producer/Merchant category is predominantly involved with the production, processing, or handling of the physical commodity - such as miners or jewelers. On the other end of the former commercial category, swap dealers are entities primarily involved with making a market with swaps or that engages in swaps during its normal course of business (you can read more here). Essentially, Producers/Merchants are dealing with physical gold while swap dealers are primarily playing the paper markets.

Since we feel the Producer/Merchant category is much more in tune with the actual physical gold market as they see it on a day-to-day basis, we give this category much more sway when analyzing position changes. Thus the fact that they didn't short en masse after the Brexit vote, is actually a bullish factor as they didn't feel the need to create major hedges for their physical positions.

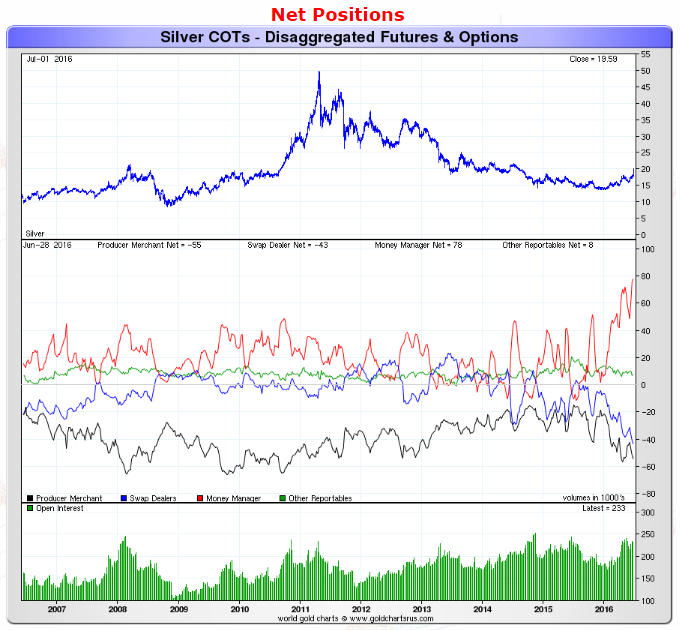

As for silver, the action week's action looked like the following:

Source: Sharelynx Gold Charts

Source: Sharelynx Gold Charts

The red line which represents the net speculative positions of money managers, increased by a little more than 1,000 contracts while shorts decreased by a little under 2,000 contracts. That was actually a bit unusual because in this report that's pretty small beans in terms of activity - the silver market was probably being moved by other players last week. But again, just like in gold, we are also at historic highs in silver.

Our Take and What This Means For Investors

Another rising week for gold and that led to another historical high in terms of the speculative net long gold position. As we stated in previous pieces, we really like that such a large amount of investors are bullish gold as it is a strong contrarian indicator - but we have been very wrong as the gold price has continued to rise despite this historical high in speculative gold bulls.

Investing is a finicky business as you can be dead right in terms of your logic and still watch a position lose money. Then again, you can think you're right and be dead wrong. The key is to re-evaluate and check that natural human hubris that seeps into our investment decisions.

Is it time to change our position on gold and go long gold rather than wait for a pullback?

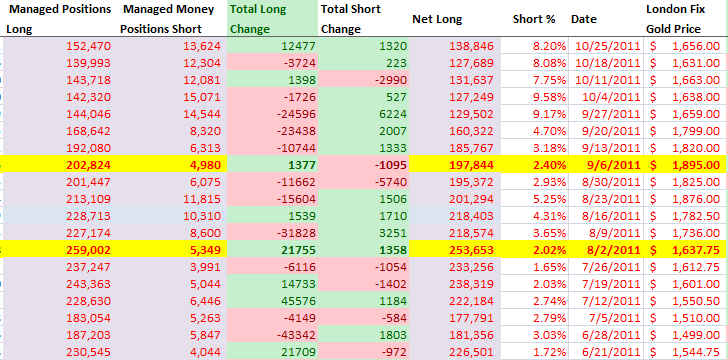

We decided to take a look back at the previous historical net long high in gold - back in 2011 when gold hit its all-time peak.

As investors can see, gold's previous cyclical speculative net long peak was hit on the week of 8/2/2011, when the net long position reached around 253,000 contracts and the gold price was $1637.75 per ounce. If you had used that data to wait for a pullback (or worse get short), you would have seen gold rise for another month to a high of $1895 per ounce - not a very fun position to be in.

The thing is that you would have actually been right if you had just waited longer as gold continued to drop to the end of the year as it ended under $1600 per ounce. But of course, you would have had to wait four long months to see that - very hard to do with gold scaling new all-time highs.

Obviously we only have a single cyclical data point here to compare, but if gold does the same thing this time we may see it climb to over $1500 per ounce before it drops back below $1300. If we were playing that strategy we'd jump back into gold and wait for it to go parabolic before getting out.

But with so much bullish sentiment in gold we just cannot feel we are being disciplined investors, especially considering that we don't see evidence of a surge in physical gold buying from the general population. We have been hearing reports of Indian gold trading at significant discounts, while Chinese buying doesn't seem to be so strong. Additionally, one of the biggest and most consistent buyers of gold, the Russian central bank, recently mentioned it doesn't see any possibility in increasing its gold and foreign exchange reserves. Pair that with the fact that for the first time since it started reporting gold reserves, the Chinese central bank didn't buy any gold in May, and we see some fundamental reasons why gold in the short-term could see a major pull-back.

While it is extremely hard to not be bullish with such a bullish run in gold and investors sentiment running so high, we cannot reverse our position on gold yet. We think despite these things investors should hold off on increasing their gold positions and should actually be decreasing gold positions in ETF's and miners such as the SPDR Gold Trust ETF (NYSEARCA:GLD), iShares Silver Trust (NYSEARCA:SLV), ETFS Physical Swiss Gold Trust ETF (NYSEARCA:SGOL), and miners such as Randgold (GOLD) and Barrick Gold (NYSE:ABX).

As we said last week, we think gold will rise much further in the coming years, but emotions and not fundamentals are ruling here and it is too crowded of a trade for us to be long with anything but our core gold position (which we maintain). We want to get back into gold but we want a much better entry point.

0 comments:

Publicar un comentario