Into The Shadows: China's $3.2 Trillion Ticking Time Bomb

by: The Heisenberg

Summary

- Take a look behind the curtain folks, and behold China's labyrinthine shadow banking complex.

- This is how Chinese banks channel trillions in credit to restricted sectors and companies.

- And this is why Kyle Bass is betting against the yuan.

- This is how Chinese banks channel trillions in credit to restricted sectors and companies.

- And this is why Kyle Bass is betting against the yuan.

Given that most shadow lending is short-term in nature, typically under three months, there's a risk that a small-scale panic could rapidly turn into a liquidity crisis that sweeps the industry.

That's from a Bloomberg View piece by Christopher Balding, an associate professor of business and economics at the HSBC Business School in Shenzhen.

It goes without saying that China's shadow banking complex isn't well understood. The labyrinthine system of intermediaries, back channels, and end-arounds banks use to funnel money to borrowers of various stripes is so complex, it's not even clear that the banks themselves could quantify their exposure if they tried.

But it's critical that someone, somewhere (preferably a regulator in China) attempt to untangle the mess because once you begin to understand just how self-referential this whole thing truly is, it becomes readily apparent that it literally is a ticking time bomb.

In fact, it's a small miracle it hasn't imploded yet. I've talked quite a bit about this lately (here and here for instance). Between high profile shorts by Kyle Bass and George Soros, the broader investment community is beginning to wake up to the possibility that there's more to the China story than "will they or won't they have a hard landing."

They've already landed. And it was indeed hard.

Needless to say, GDP growth is nowhere near the headline print. For one thing, China doesn't net out import prices when they calculate their deflator. I know that sounds like something really boring right out of freshman economics. And it is. But here it's important. Think about it. When commodity prices are plunging, you need to account for that when you're measuring domestic output (i.e., GDP). If you don't, you're not really measuring the value of goods and services produced in your country, you're just re-reporting PPI. This, arguably, causes some EMs to consistently overstate GDP when commodity prices are falling.

And that's just one technical reason to believe growth is overstated. There are other decidedly "non"-technical reasons to believe the numbers don't tell the whole story. Reasons like this one: the Politburo says growth is between 6.5% and 7%, so that's what growth is. And it's just that simple.

(Image credit: Institutional Investor)

But let's bring it back to the banks. And then to the yuan (NYSEARCA:CYB).

You have to look beyond the hard landing and ask what decelerating growth means for the institutions that finance the economy. What does it mean when you, as a lender, are compelled from on high to support an economy that's literally crashing but you are also compelled by the very same authority to rein in risk and avoid doing things that imperil the system?

It's an impossible task and clearly, banks feel as though it's more important to keep funneling money to borrowers than it is to recognize losses and/or tell Beijing that you simply have to cut off the spigots or else your balance sheet is going to rot from the inside out.

Of course, you can't just keep piling up traditional loans. Especially not to sectors that are suffering from overcapacity. While the official NPL data is certainly malleable, one has to wonder how much further the truth can be stretched. The idea that overall, NPLs in the sector are something like 1.75% is absurd. Fortunately, there are plenty of ways around booking loans as, well, as loans.

What's especially amusing is the kind of blurry line between "on balance sheet" and "off balance sheet." A few days ago I said the following about the CNY39 trillion in shadow banking credit that's proliferated in China: "You might as well just count that as off balance sheet."

Sure, some of it is carried on balance sheet, but who cares when it's all lumped under the line item "investments." They might as well just have a line item called "who knows?". No one knows what all is included under "investments held as receivables," and frankly, you probably don't want to know.

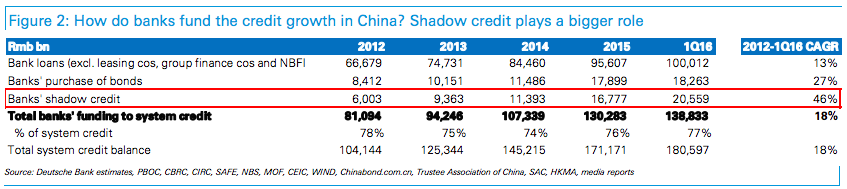

But that's too bad because I'm going to give you a peek under the hood, courtesy of a few selected excerpts from Deutsche Bank, whose work on this is really incredible. First off, note the extent to which shadow banking has dominated in terms of growth among credit channels:

(Table: Deutsche Bank)

(Table: Deutsche Bank)

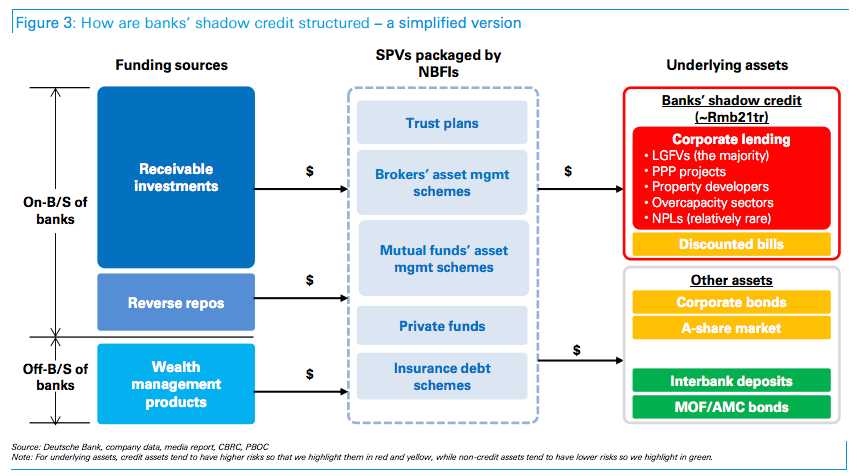

So what exactly do we mean by "shadow banking" when it comes to China? Deutsche provides the most succinct explanation I've seen to date:

Banks' shadow credit is essentially lending to corporates, but it is booked under either interbank assets or receivable investments on the balance sheet, or under wealth management products (WMPs) off the balance sheet, instead of being under a loan category.

There you go. Simple. For those interested in learning more about WMPs, please see the articles linked above. For now, we'll focus on exactly how banks channel money to corporates through the vast shadow banking complex. Here's a simplified diagram:

(Chart: Deutsche Bank)

(Chart: Deutsche Bank)

Okay, so that looks complicated, right? Really it's not. The important thing to understand is the on-balance sheet "receivables;" (these are the things which I previously contended might as well just be counted as off balance sheet because the average investor has no way in hell of knowing what they are). Of the total CNY21 trillion in assets accounted for by the three types of assets depicted above, CNY14.3 trillion is on-balance sheet receivables. So that's what you really need to grasp. Fortunately, it's not nearly as complex as it sounds either. Here are the summary bullets from Deutsche:

- Firstly, due to constraints of liquidity or capital or restricted sector, a bank is unable to make loans to one of its corporate borrowers.

- Secondly, the bank arranges with a non-bank financial institution (NBFI), e.g., a trust company, to package a trust product with a loan granted to the corporate borrower as the underlying asset.

- Thirdly, the bank uses its own fund to purchase the trust product and books it under receivable investments. At this point, the bank is effectively taking on the credit risk of the underlying corporate borrower.

See how that works? The bank is restricted from lending to a certain company or sector, so they simply use a middleman to do the dirty work. There's $2.2 trillion (that's 2.2 trillion dollars) of that on banks' books.

So why would banks want to do this, you ask? Well that's pretty simple too. Here are four more bullets from Deutsche:

- Save capital consumption, as risk weights for NSCAs in some cases are as low as 20%, as we illustrate above.

- Circumvent the loan quota imposed by the PBOC so that banks could free up loan quotas for other high-yield loans.

- Continue to support their corporate customers who are restricted from obtaining bank loans by current regulations, e.g., LGFVs and property developers.

- Hide NPLs or overdue loans. As mentioned, some small unlisted banks package corporate loans in overcapacity sector and even NPLs into these SPVs.

Nothing complicated about that. They wanted to hold has little in the way of reserves possible against their assets; they want to get around caps on loans; they want to make their customers happy; and they want to repackage and offload their NPLs only to essentially buy them back but carry them in such a way that they aren't booked as non-performing.

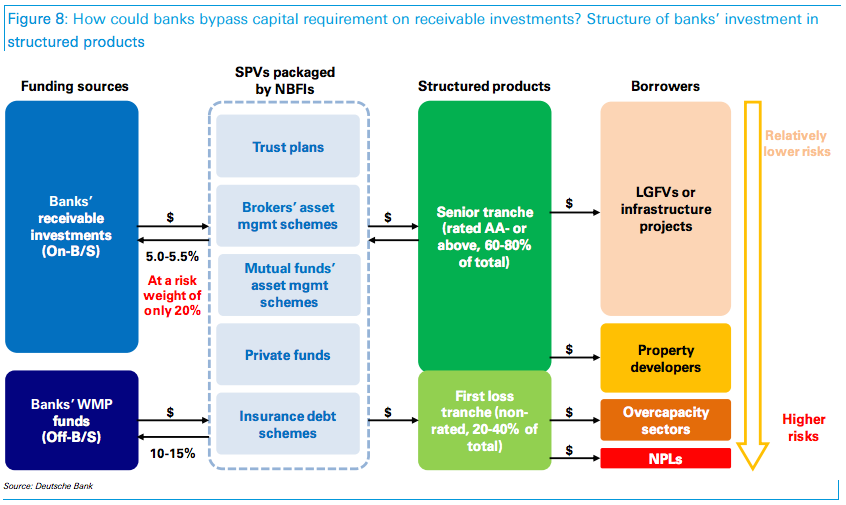

There's much, much more in the full note but out of respect for the research and out of respect for your sanity, I'll simply present one final diagram which shows how banks get around capital requirements on these "investments":

(Chart: Deutsche Bank)

(Chart: Deutsche Bank)

See what they're doing there at the top? They're channeling money to local government financing vehicles and getting away with an RWA of only 20% because they've invested in the senior tranches.

For this they get a 5-5.5% return.

Remember folks, this is only ~10% of total banking assets in China. This does not count the portion of China's traditional loan book that's going to eventually sour when the government finally capitulates and purges the excess capacity at SOEs and elsewhere in the industrial sector.

Once again, you can see why Kyle Bass is betting against the yuan. When they have to recapitalize this system, the cost will be astronomical.

I'll leave you with the following quote from Moody's:

...shadow banking assets accounted for nearly 80% of GDP in 2015. Increasing interconnectedness between banks and the shadow banking system could put additional pressures on banks' asset quality.

Investments in loans and receivables among the 26 listed banks in China jumped four-fold to RMB10.4 trillion from RMB2.5 trillion between 2012 and 2015.

Moody's stressed that these investments are an opaque source of asset risk.

0 comments:

Publicar un comentario