Gold Miners: Where Wealth Goes To Die

by: Gold Bug

My long term market outlook for gold is bearish, but investors who own physical are guaranteed to retain some value in their investment while mine investors are not.

Gold miners almost invariably under-perform the spot price of gold over the long term.

A combination of debt load, risk and costs that are rising faster than the rate of inflation make gold miners extremely dangerous investments in a bear market.

Gold miners almost invariably under-perform the spot price of gold over the long term.

A combination of debt load, risk and costs that are rising faster than the rate of inflation make gold miners extremely dangerous investments in a bear market.

Gold miners are not a good investment.

The Market Vectors Gold Miners ETF (NYSEARCA:GDX) is the most common security retail investors use to gain exposure to the gold mining industry. Other popular stocks include; Barrick Gold (NYSE:ABX), Gold Corp (NYSE:GG), Rangold (NASDAQ:GOLD) and Sandstorm (NYSEMKT:SAND).

Many precious metals investors see gold miners as a way to gain greater upside on gold rallies.

When gold prices become significantly higher than a mines cost of production the difference is pure profit - variable cost per ounce stays the same while the selling price increases drastically.

This can be taken to the extreme by investing in smaller cap junior miners via the (NYSEARCA:GDXJ) ETF or through leveraged products like (NYSEARCA:NUGT)

There is a problem: While large cap gold miners do well to not lose money, their smaller cap and leveraged counterparts may teeter on the edge of bankruptcy in a long term gold bear market because of the unique risks miners have when faced with a declining price. These risks will be explored in this article.

Gold miners under-perform physical gold:

Gold miners are under-diversified. Cash Costs and All-In Sustained Costs (AISC) are rising faster than the pace of inflation, and for many mining companies these costs are already very close to the spot price of gold.

Most gold mining stocks tend to under-perform in almost every scenario except day trading.

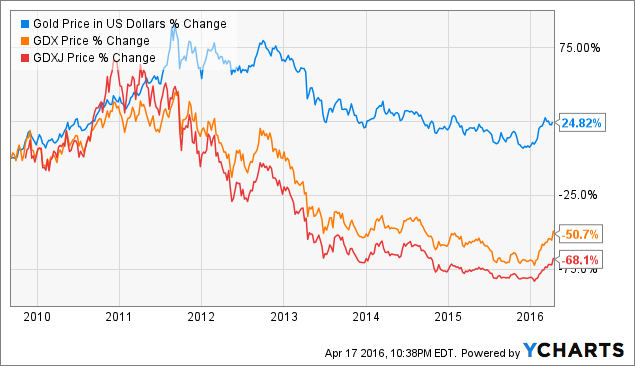

When gold plunged 25% in 2013 gold mining ETFs fell a staggering 50%. In fact, the majority of mining stocks underperform the metal in good times and bad. Investors who got into GDXJ at the peak of 2011, are currently sitting on losses over 80%.

2010 to 2016: failure in GDX and GDXJ:

Why are gold mining stocks so bad?

Unlike physical gold, gold miners have debt and other liabilities eating away at the value of the investment. Even if the price of gold is high, these companies may still only make minimal profits or even losses depending on the financial situation of the specific company or what occurs in the mine.

Gold miners are leveraged with debt and suffer from a greater level of risk and uncertainty compared to physical gold and the market prices this into their values, making the majority of mining stocks perform worse than gold over the long term.

The economics of gold mining.

I believe many of the smaller gold companies are the result of speculation on further gold price increases and were created with the assumption that gold prices would increase or stay stable after the bull market of 2011. When this did not occur, many gold producing locations essentially became worthless because they can only produce at a price higher than they can sell for.

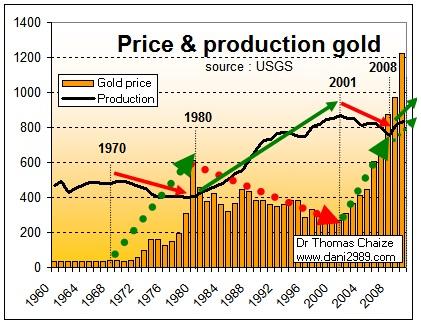

There is a lag between gold price increases and the completion of investments needed to increase production and exploit the price increase:

When the price of a commodity goes up, the free market uses this as a signal for producers to expand production and increase competition in the market.

However, it can take many years and significant difficulty for a mine to increase production, or for new mining companies to form. By the time the new mines are functional and expansions are ready, the price of the commodity may have already decreased - as a result many mines find themselves unable to turn a profit at the current prices.

This problem is compounded by the fact that these new mines may be in locations where operational costs where prohibitively high before prices increased for the commodity.

Gold can fall below cost of production:

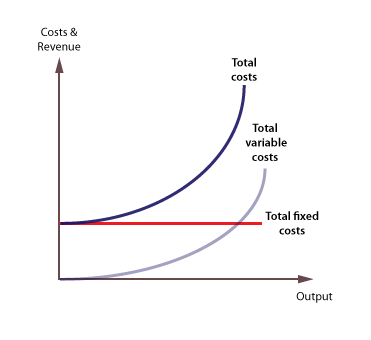

Many investors assume the average "All In Sustaining Costs" (AISC) for extracting gold represents a price floor below which gold prices cannot fall. This is not the case.

The truth is that most companies, mines included, will operate for years at a loss so long as their income exceeds fixed costs of operation - the costs they would have to pay with or without producing:

AISC does not represent fixed costs. It is made up primarily of variable costs that include exploration and expansion. These should not be seen as a price floor for gold prices.

I think mining cash costs are a more useful metric for determining the price floor of gold before it encounters significant supply side resistance. The average cash cost for GDX companies is less than $700. Granted, while cash costs are not fixed costs either, they typically represent the largest non-discretionary expense a mine will have to undertake to produce gold.

To determine the safety of individual mining companies; liabilities, interest expense, rent and royalty payments are more useful than AISC or cash costs.

Conclusion:

If you are bullish on gold the best bet is in either physical or GLD. I believe gold mining stocks are much too risky for what they offer. The majority of these stocks underperform the spot price of the metal in good times and bad. If gold goes to $900 per ounce, holders of physical still have $900 dollars worth of value. GDX and GDXJ holders, on the other hand, may have nothing but a portfolio full of soon to be bankrupt companies.

This is not to say that all gold miners are terrible, there are some good companies in the sector.

I like the companies with low debt numbers and massive cash positions such as Nevsun Resources (NYSEMKT:NSU) and Caledonia Mining Corp (OTCQX:CALVF). These miners also pay dividends and trade at a significant discount due to geographic risk.

The Market Vectors Gold Miners ETF (NYSEARCA:GDX) is the most common security retail investors use to gain exposure to the gold mining industry. Other popular stocks include; Barrick Gold (NYSE:ABX), Gold Corp (NYSE:GG), Rangold (NASDAQ:GOLD) and Sandstorm (NYSEMKT:SAND).

Many precious metals investors see gold miners as a way to gain greater upside on gold rallies.

When gold prices become significantly higher than a mines cost of production the difference is pure profit - variable cost per ounce stays the same while the selling price increases drastically.

This can be taken to the extreme by investing in smaller cap junior miners via the (NYSEARCA:GDXJ) ETF or through leveraged products like (NYSEARCA:NUGT)

There is a problem: While large cap gold miners do well to not lose money, their smaller cap and leveraged counterparts may teeter on the edge of bankruptcy in a long term gold bear market because of the unique risks miners have when faced with a declining price. These risks will be explored in this article.

Gold miners under-perform physical gold:

Gold miners are under-diversified. Cash Costs and All-In Sustained Costs (AISC) are rising faster than the pace of inflation, and for many mining companies these costs are already very close to the spot price of gold.

Most gold mining stocks tend to under-perform in almost every scenario except day trading.

When gold plunged 25% in 2013 gold mining ETFs fell a staggering 50%. In fact, the majority of mining stocks underperform the metal in good times and bad. Investors who got into GDXJ at the peak of 2011, are currently sitting on losses over 80%.

2010 to 2016: failure in GDX and GDXJ:

Why are gold mining stocks so bad?

Unlike physical gold, gold miners have debt and other liabilities eating away at the value of the investment. Even if the price of gold is high, these companies may still only make minimal profits or even losses depending on the financial situation of the specific company or what occurs in the mine.

Gold miners are leveraged with debt and suffer from a greater level of risk and uncertainty compared to physical gold and the market prices this into their values, making the majority of mining stocks perform worse than gold over the long term.

The economics of gold mining.

I believe many of the smaller gold companies are the result of speculation on further gold price increases and were created with the assumption that gold prices would increase or stay stable after the bull market of 2011. When this did not occur, many gold producing locations essentially became worthless because they can only produce at a price higher than they can sell for.

There is a lag between gold price increases and the completion of investments needed to increase production and exploit the price increase:

When the price of a commodity goes up, the free market uses this as a signal for producers to expand production and increase competition in the market.

However, it can take many years and significant difficulty for a mine to increase production, or for new mining companies to form. By the time the new mines are functional and expansions are ready, the price of the commodity may have already decreased - as a result many mines find themselves unable to turn a profit at the current prices.

This problem is compounded by the fact that these new mines may be in locations where operational costs where prohibitively high before prices increased for the commodity.

Gold can fall below cost of production:

Many investors assume the average "All In Sustaining Costs" (AISC) for extracting gold represents a price floor below which gold prices cannot fall. This is not the case.

The truth is that most companies, mines included, will operate for years at a loss so long as their income exceeds fixed costs of operation - the costs they would have to pay with or without producing:

AISC does not represent fixed costs. It is made up primarily of variable costs that include exploration and expansion. These should not be seen as a price floor for gold prices.

I think mining cash costs are a more useful metric for determining the price floor of gold before it encounters significant supply side resistance. The average cash cost for GDX companies is less than $700. Granted, while cash costs are not fixed costs either, they typically represent the largest non-discretionary expense a mine will have to undertake to produce gold.

To determine the safety of individual mining companies; liabilities, interest expense, rent and royalty payments are more useful than AISC or cash costs.

Conclusion:

If you are bullish on gold the best bet is in either physical or GLD. I believe gold mining stocks are much too risky for what they offer. The majority of these stocks underperform the spot price of the metal in good times and bad. If gold goes to $900 per ounce, holders of physical still have $900 dollars worth of value. GDX and GDXJ holders, on the other hand, may have nothing but a portfolio full of soon to be bankrupt companies.

This is not to say that all gold miners are terrible, there are some good companies in the sector.

I like the companies with low debt numbers and massive cash positions such as Nevsun Resources (NYSEMKT:NSU) and Caledonia Mining Corp (OTCQX:CALVF). These miners also pay dividends and trade at a significant discount due to geographic risk.

0 comments:

Publicar un comentario