When Economic Theory Fails: Globalization

- Economic theory supporting globalization suggests that regional or national specialization towards producing goods that best suit those economies will benefit everyone as we all produce goods we are best at.

- In reality, the current trend of globalization is leading to a global consumer demand crisis, in part because developed world consumers are earning less, while developing world consumers save more.

- Implication for investors is that we need to re-think the diversified portfolio, because the broader market will be stagnated. Sector picking at right time is the ideal new strategy.

For this article I want to cover globalization and how it fails to live up to its promise as indicated that it should, according to basic economic theory. In order to do that we should first establish what economic theory suggests should happen when global trade growth is facilitated.

The theoretical basis for supporting globalization and the liberalization of trade is the assumption that different countries have different possibilities to produce certain goods based on their labor force, labor costs, and the environment they live in. For instance, the classical example is watermelon growing in Mexico, versus Canada. Goes without saying that Mexico is better suited for it thanks to its climate as well as lower labor costs. Canada on the other hand is considered to have a much better educated labor force, therefore it is seen as being better at producing innovative products such as software and so on. It is therefore seen as beneficial for both countries to trade with each other, with Canadians benefiting from tastier watermelon which they can get year round thanks to trade with Southern states such as Mexico, while Canadian labor is much better utilized in producing things such as software which they can export to countries where labor profiles do not permit for the same quality to be produced. Thus everyone benefits from better quality at better prices and everyone can specialize on producing the things they are best at producing.

Theory works fine on paper and to some extent it may be true that the growth in global trade we have seen in past decades helped improve the lives of hundreds of millions of people initially.

By initially, I mean in the initial few decades. But the trend is now breaking down and the negative consequences are actually creating a drag, which threatens to reverse some of the initial gains. As it turns out, in real life the theory brings with it some consequences when put into practice.

As I pointed out to be the case with innovation, where I argued that certain innovations which lead to job loss, in fact lead to a lack of productivity gains because it kills consumer demand, therefore few new production facilities are being built or renovated, there is a paradox developing in the case of global trade as well. Globalization and the flow of trade that developed in past decades is now leading to a decline in global trade growth rates and is helping cause slower global economic growth.

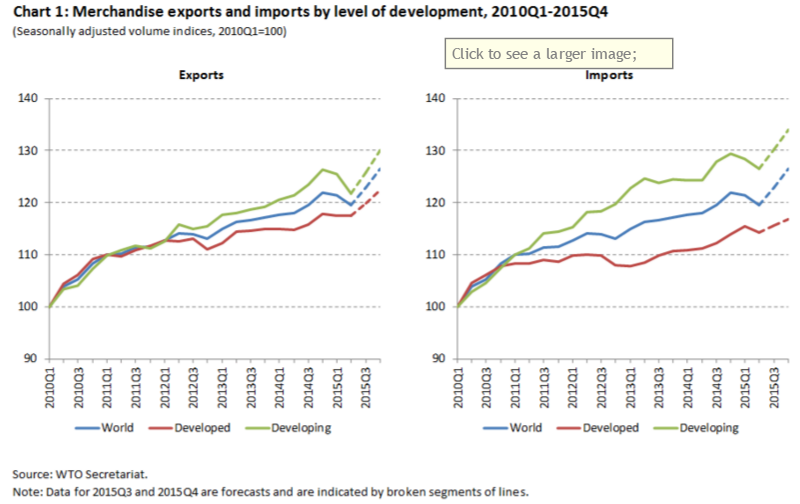

(click to enlarge)

(link)

(link)As we can see from the graph, global trade in fact entered its biggest decline in the past year or so since 2010, despite the fact that we are in what passes as an economic recovery these days.

The WTO is predicting a sharp rebound, but it is hard to see where and how that rebound will happen.

How it went wrong

The initial effect of increased global economic integration through trade was indeed what everyone would have expected. In the 1990's and up until 2007 global trade increased at twice the rate of global economic growth, while economic growth itself was also very healthy. Since then however, the WTO indicated that global trade growth has been more or less same as global economic growth, while growth as we know has been rather anemic, under 3% per year on average since 2008.

There is one main factor related to globalization, which is leading to a global economic slowdown and paradoxically to a slowdown in trade growth as well. That factor has to do with the resulting decline in real incomes in the Western World, where the strongest consumers are to be found.

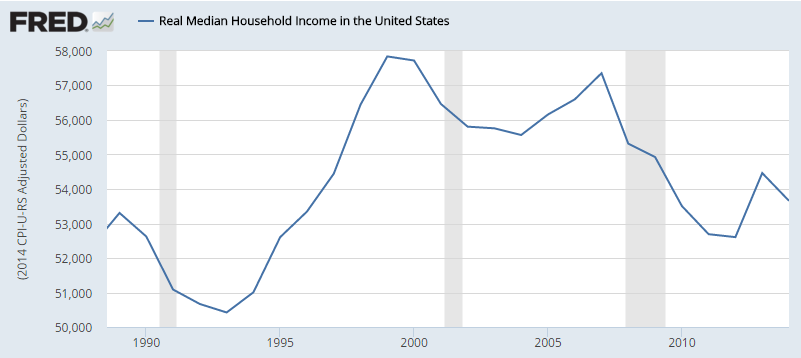

(click to enlarge)

Source: St. Louis Fed

As we can see, US household income has taken a decisively downward path since 1999 and it is not an insignificant trend given that real income is down almost 8% since then, as of the end of 2014.

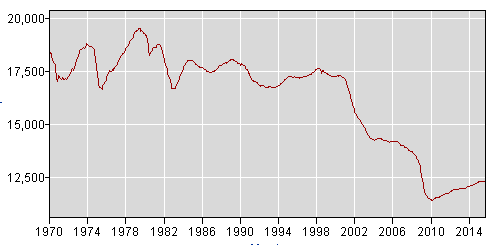

There are a few causes of the failure to improve US household incomes, one of which I indicated in my last article dedicated to economic theory failures. But one of the main trade-related causes has been the loss of manufacturing and increasingly higher-value jobs such as software development to the developing world. If we look at manufacturing alone since the WTO was established, the trend and correlation is unmistakable. The WTO was established in 1995 and just four years later manufacturing jobs started to disappear, and if we look at the graph above, it also coincides with the peak and subsequent decline in real household incomes.

Source: Bureau of Labor Statistics. Note: Data is in thousands.

As we can see, manufacturing jobs which generally tend to pay alright have been disappearing in the past eighteen years or so at a very fast rate. Five million jobs were lost so far. Back in the 1990's when globalization was starting to pick up steam, we were told not to worry because new jobs, better jobs and cleaner jobs will replace the ones we will lose. Economic theory in fact suggests that it should have been the case. That did not turn out to be true as the data on household incomes tells us.

As it turns out, higher levels of employment in fields such as the much-trumpeted R&D never happened, because the sector did not have the capacity to absorb and make up for the job losses suffered. There are currently 2.7 million jobs directly related to all R&D being performed in the US. This figure has been more or less constant, with no amount of variation which would be of great consequence to the overall US job market, given that there are over 120 million people with a full-time job in total. This was and still is a false narrative, which induces people into error when it comes to today's realities.

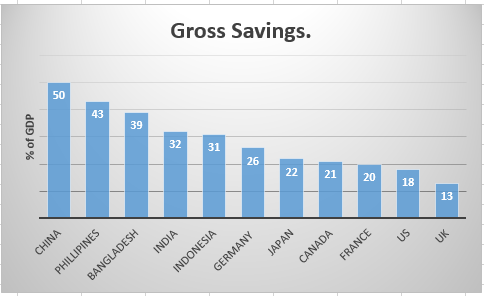

Going back to the effect this has had on the global economy, it turns out that developing world consumers such as the Chinese are not the best consumers, therefore not great drivers of demand. The wage earning power transfer from the developed world to them has resulted in money being stranded in Chinese consumer and government savings accounts. While the savings rate in most developed countries is somewhere between 10-25% of GDP, in the developing world it is in the 30-50% range.

Data source: World Bank.

Some of the negative consequences of this trend were masked for a while by lower interest rates and higher rates of indebtedness in the developed world, which allowed for consumer demand to continue to increase, but on both fronts, we are looking at the end of those one-time measures. Lower interest rates and higher levels of indebtedness were incidentally made possible thanks to the effects of globalization, which includes lower inflation. Interest rates have nowhere left to go but up, while Western consumers and governments cannot continue to expand their liabilities for much longer.

As was the case with the productivity assumptions, the assumption that globalization will provide for more prosperity for all in the longer run is looking to be less than a certainty to say the least. Looking ahead, the continued trend of globalization will continue to put downward pressure on global consumer demand, due in part to the higher savings rate. Ironically, this will lead to a slowdown in income growth in the developing world, which will make it harder for people living in those countries to satisfy their desires to save, because earning a decent income will become harder.

In the developed world, the slow but steady march towards the global average income will continue. At some point government debt crises may speed up the process as we have seen in places like Greece already. There is more and more evidence that while countries such as India and China are converging upwards towards the global average GDP/capita, countries with a high level of income are converging downwards towards that same average. Because of the lack of robust global economic growth, which as I pointed out is in part due to the negative effects of globalization, we are set to all be disappointed in regards to where that average we are all converging towards will be found.

Implications for investors

As I pointed out in my first article on the issue of failures in economic theory when put into practice, slow global economic growth and a likely continued consumer demand crisis means that the diversified portfolio strategy will likely be a long-term failure. There are opportunities to play trends, where certain sectors may be due to move up for a while. Those are the opportunities that need to be explored and exploited. For instance, I am currently building a position in commodities, mostly in oil & gas companies based on the conviction that current prices are well below the minimum level of sustainability needed for the long term. Any investment strategy based on diversification meant to just slightly outperform the broader market will most likely leave investors disappointed with their longer term results.

0 comments:

Publicar un comentario