Gold Is Rewriting The Textbooks; Likely Headed Lower, Will Test Critical $1,200 Level

by: Robert Wagner

Feb. 3, 2014 10:49 PM ET

One of my favorite investment themes is biodiesel. The EPA has implemented a relatively new program called the RFS2 which has all sorts of market distorting regulations that alter the prospects for the industry.

Congress then piles on with something called a "blender's tax credit," and there is simply too many variables for the market to accurately discount all the possible outcomes. When I read research reports from the Wall Street brokerages on this industry it becomes apparent that many on Wall Street haven't figured out the RFS2 yet. If Wall Street doesn't understand the RFS2, it is likely that they are making the wrong recommendations and errors in their earnings estimates. If they are making the wrong recommendations and earnings estimates, it creates an opportunity to profit from their errors because the market has discounted their errors.

Another favorite subject is Yahoo's (YHOO) holding of Alibaba. When I first wrote about that issue a year ago it was relatively unknown. Now it is very well known the stock is up over 100% from when I first wrote about it. The markets hadn't fully discounted the relatively unknown holdings of Alibaba, but I was pretty confident they would once the market started to pay attention to them.

My other favorite theme to write about is gold. I have written many bearish articles on gold, detailing the counter intuitive theory that gold is not an inflation hedge... at least not now. The fifth article I wrote for Seeking Alpha detailed how gold was behaving like a leveraged bond fund. The reason that is significant is because if gold was an inflation hedge, it would be performing like a leveraged inverse bond fund. If gold was an inflation hedge it would be directly correlated with interest rates and inversely correlated with bonds.

The fact that gold was correlating with bonds defies every economic and financial textbook ever written, or at least that I've ever studied. Gold is the classic inflation hedge. Ask anyone what is the most popular inflation hedge and the number one will be gold. Ironically, during a period of disinflation and near deflation, all the gold commercials still tout gold as an inflation hedge. The reason they do that is because they know the markets think of gold as an inflation hedge. Problem is the markets are wrong, and if the markets are wrong, money can be made from their error.

The theory goes that printing money causes inflation and inflation drives the price of gold higher. Almost everyone has been taught that. I was taught that; textbooks teach that to this day. Problem is they are wrong, or at least not right in all circumstances. What the markets failed to understand is the context in which that theory was developed. That theory is consistent with late business cycle inflation, or hyperinflation situations like the Waimar Republic where newly printed money was immediately used to take things off the shelves of a store.

Yes, printing money can cause inflation, but it doesn't always result in inflation. Printing money that simply goes and sits in a back as reserve requirements isn't inflationary. For money to be inflationary it has to be put into circulation buying things.

Banks are loaning, people aren't buying, there is no mechanism for the new money to cause inflation is it just sits in a bank. That is what the market doesn't, or at least didn't, get. The market reaction of gold even confused Janet Yellen and Ben Bernanke, who claim they don't understand its behavior, and don't believe anyone else does either:

That is understandable; gold has been performing in a counterintuitive manner contrary to what is taught in our finance and economic courses. It is not surprising then that many of my articles were just viciously attacked. The gold bugs are legendary for their vitriol, and my articles brought out the worst of them. It takes a whole lot for people to change their thinking, especially when it has been drummed into them year after year after year. Old habits die hard, and I knew the belief that gold wasn't an inflation hedge would take a long time for the markets to accept. Therefore, I knew there was going to be many many many opportunities to make money shorting gold. That belief resulted in many articles highlighting that the gold rallies were nothing but dead cat bounces and pointing out how gold uber bulls were certain to be wrong.

Fortunately, I do not stand alone with this counterintuitive theory. Thanks to a comment on my recent article, it was brought to my attention that Pimco is promoting the exact same theory that I have been outlining over the last year. They even produced a nice graph to demonstrate it.

Where is Gold Going?

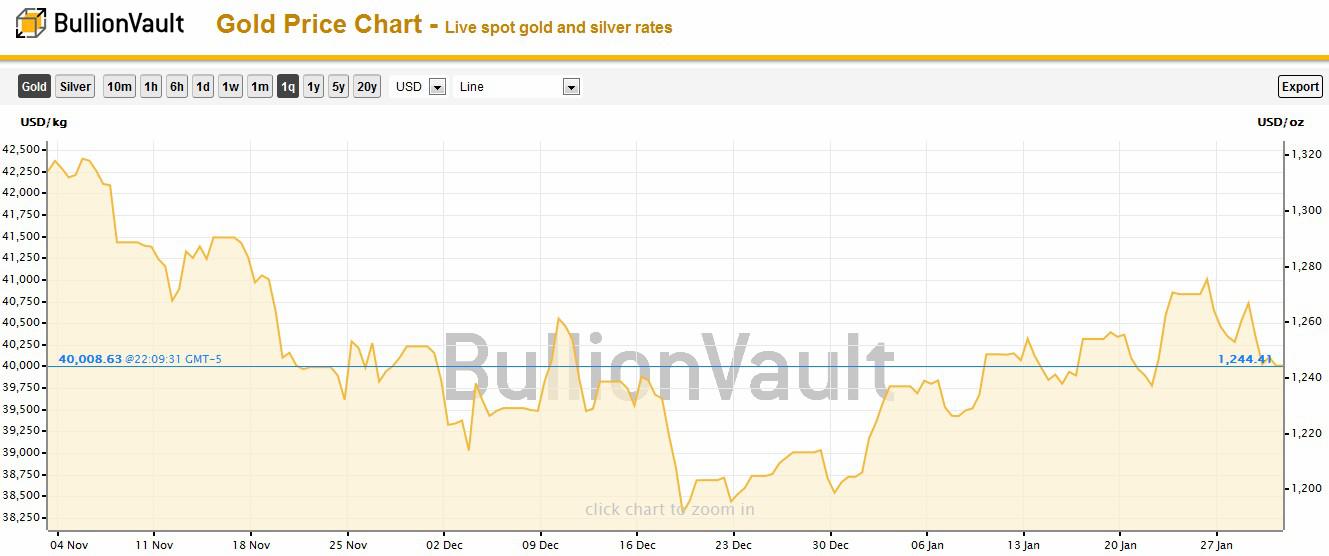

In mid-December 2013 gold tested key support of $1,200/oz, and the support held. After support held, gold rallied to reach a peak of $1,275 on January 26, 2014.

(click to enlarge)

Since that time a crisis in Turkey, a global stock market correction and falling interest rates after the Fed's "Taper" announcement has failed to provide support for gold. Those kinds of events usually provide support for gold, but this time, owners of gold have used the opportunity to exit their positions, not add to them. Gold appears to be losing its safe haven appeal.

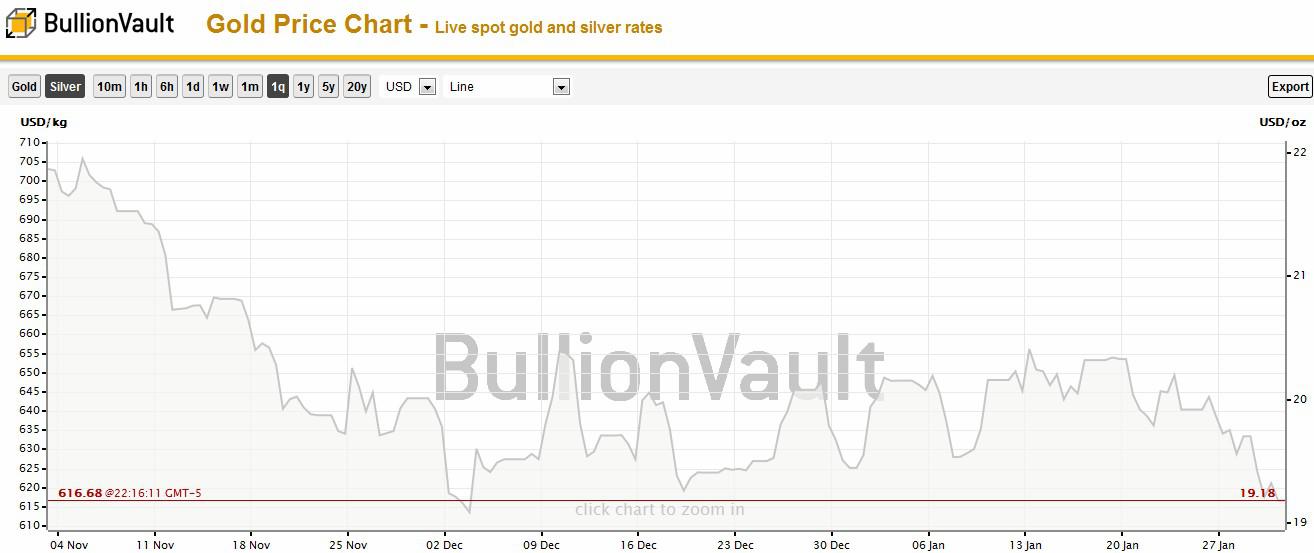

To make matters worse for gold, its close cousin silver has retraced more than 100% of its post December 19th advance.

(click to enlarge)

Running a comparative chart of the gold and silver ETFs highlights the divergence.

(click to enlarge)

While gold and silver don't always trend together, they do so more often that not. With the most recent events failing to drive gold higher, and silver giving up 100% of its most recent rally, I would expect the odds favor gold retesting $1,200/oz over reversing from here and exceeding its previous peak of $1,275. If gold significantly breaks the $1,200/oz support, I would expect gold to rally back up to $1,200/oz, which would then become a resistance level. If gold fails to retake the $1,200/oz level, then there is little to stop it from dropping to $1,100 and beyond.

(click to enlarge)

In conclusion, following the classic relationship of gold and inflation will not work in this current market environment. Gold is not acting as an inflation hedge, it is acting as a fear gauge - a fear of financial collapse.

As the economy strengthens, and inflation and interest rates return to normal, gold will sell off, not rally. Gold is likely to continue through an extended bear market until we get late into the business cycle when capacity constraints and a tight labor market generate the kind of inflation that will drive gold higher. That, however, is a long way away, and gold will go a lot lower before it finds a bottom from which it will rally due to eventual inflation.

I expect that gold is headed towards a critical support level. $1,200 has been tested multiple times over the last decade, and each time it has proven to be either a significant support or resistance level. Given that gold tested $1,200/oz just last month, and is already looking like it will be tested again soon, with silver already breaking its support level, I would place odds that gold will break $1,200 this time, and $1,100 will become the next likely price target.

Congress then piles on with something called a "blender's tax credit," and there is simply too many variables for the market to accurately discount all the possible outcomes. When I read research reports from the Wall Street brokerages on this industry it becomes apparent that many on Wall Street haven't figured out the RFS2 yet. If Wall Street doesn't understand the RFS2, it is likely that they are making the wrong recommendations and errors in their earnings estimates. If they are making the wrong recommendations and earnings estimates, it creates an opportunity to profit from their errors because the market has discounted their errors.

Another favorite subject is Yahoo's (YHOO) holding of Alibaba. When I first wrote about that issue a year ago it was relatively unknown. Now it is very well known the stock is up over 100% from when I first wrote about it. The markets hadn't fully discounted the relatively unknown holdings of Alibaba, but I was pretty confident they would once the market started to pay attention to them.

My other favorite theme to write about is gold. I have written many bearish articles on gold, detailing the counter intuitive theory that gold is not an inflation hedge... at least not now. The fifth article I wrote for Seeking Alpha detailed how gold was behaving like a leveraged bond fund. The reason that is significant is because if gold was an inflation hedge, it would be performing like a leveraged inverse bond fund. If gold was an inflation hedge it would be directly correlated with interest rates and inversely correlated with bonds.

The fact that gold was correlating with bonds defies every economic and financial textbook ever written, or at least that I've ever studied. Gold is the classic inflation hedge. Ask anyone what is the most popular inflation hedge and the number one will be gold. Ironically, during a period of disinflation and near deflation, all the gold commercials still tout gold as an inflation hedge. The reason they do that is because they know the markets think of gold as an inflation hedge. Problem is the markets are wrong, and if the markets are wrong, money can be made from their error.

The theory goes that printing money causes inflation and inflation drives the price of gold higher. Almost everyone has been taught that. I was taught that; textbooks teach that to this day. Problem is they are wrong, or at least not right in all circumstances. What the markets failed to understand is the context in which that theory was developed. That theory is consistent with late business cycle inflation, or hyperinflation situations like the Waimar Republic where newly printed money was immediately used to take things off the shelves of a store.

Yes, printing money can cause inflation, but it doesn't always result in inflation. Printing money that simply goes and sits in a back as reserve requirements isn't inflationary. For money to be inflationary it has to be put into circulation buying things.

Banks are loaning, people aren't buying, there is no mechanism for the new money to cause inflation is it just sits in a bank. That is what the market doesn't, or at least didn't, get. The market reaction of gold even confused Janet Yellen and Ben Bernanke, who claim they don't understand its behavior, and don't believe anyone else does either:

At her Senate confirmation hearing in November, Janet Yellen said, "I don't think anybody has a very good model of what makes gold prices go up or down." Ben Bernanke also said last year that "nobody really understands gold prices, and I don't pretend to understand them either."

That is understandable; gold has been performing in a counterintuitive manner contrary to what is taught in our finance and economic courses. It is not surprising then that many of my articles were just viciously attacked. The gold bugs are legendary for their vitriol, and my articles brought out the worst of them. It takes a whole lot for people to change their thinking, especially when it has been drummed into them year after year after year. Old habits die hard, and I knew the belief that gold wasn't an inflation hedge would take a long time for the markets to accept. Therefore, I knew there was going to be many many many opportunities to make money shorting gold. That belief resulted in many articles highlighting that the gold rallies were nothing but dead cat bounces and pointing out how gold uber bulls were certain to be wrong.

Fortunately, I do not stand alone with this counterintuitive theory. Thanks to a comment on my recent article, it was brought to my attention that Pimco is promoting the exact same theory that I have been outlining over the last year. They even produced a nice graph to demonstrate it.

Where is Gold Going?

In mid-December 2013 gold tested key support of $1,200/oz, and the support held. After support held, gold rallied to reach a peak of $1,275 on January 26, 2014.

(click to enlarge)

Since that time a crisis in Turkey, a global stock market correction and falling interest rates after the Fed's "Taper" announcement has failed to provide support for gold. Those kinds of events usually provide support for gold, but this time, owners of gold have used the opportunity to exit their positions, not add to them. Gold appears to be losing its safe haven appeal.

To make matters worse for gold, its close cousin silver has retraced more than 100% of its post December 19th advance.

(click to enlarge)

Running a comparative chart of the gold and silver ETFs highlights the divergence.

(click to enlarge)

While gold and silver don't always trend together, they do so more often that not. With the most recent events failing to drive gold higher, and silver giving up 100% of its most recent rally, I would expect the odds favor gold retesting $1,200/oz over reversing from here and exceeding its previous peak of $1,275. If gold significantly breaks the $1,200/oz support, I would expect gold to rally back up to $1,200/oz, which would then become a resistance level. If gold fails to retake the $1,200/oz level, then there is little to stop it from dropping to $1,100 and beyond.

(click to enlarge)

In conclusion, following the classic relationship of gold and inflation will not work in this current market environment. Gold is not acting as an inflation hedge, it is acting as a fear gauge - a fear of financial collapse.

As the economy strengthens, and inflation and interest rates return to normal, gold will sell off, not rally. Gold is likely to continue through an extended bear market until we get late into the business cycle when capacity constraints and a tight labor market generate the kind of inflation that will drive gold higher. That, however, is a long way away, and gold will go a lot lower before it finds a bottom from which it will rally due to eventual inflation.

I expect that gold is headed towards a critical support level. $1,200 has been tested multiple times over the last decade, and each time it has proven to be either a significant support or resistance level. Given that gold tested $1,200/oz just last month, and is already looking like it will be tested again soon, with silver already breaking its support level, I would place odds that gold will break $1,200 this time, and $1,100 will become the next likely price target.

0 comments:

Publicar un comentario