Gold is bullish but appears overbought

The COT figures indicate that gold has become overbought, which is hardly surprising given the run it has had. But as a guide to prospective price performance, it is too simplistic.

Alasdair Macleod

The Commitment of Traders numbers showed that as of last Tuesday, gold was moderately overbought at net long 177,915 contracts, as the chart below of the net Managed Money category indicates:

The dotted line is the average position long-term, which we can take to be neutral, i.e. neither overbought nor oversold.

But since last Tuesday, Open Interest has increased by over 20,000 contracts, suggesting that the Managed Money net position is getting close to net long 200,000.

In the last eighteen years, this level was first breached in the 2009—2011 bull market and three times since.

Should gold bulls be worried?

Clearly, something is driving Managed Money pairs traders (hedge funds) into selling dollars to buy gold.

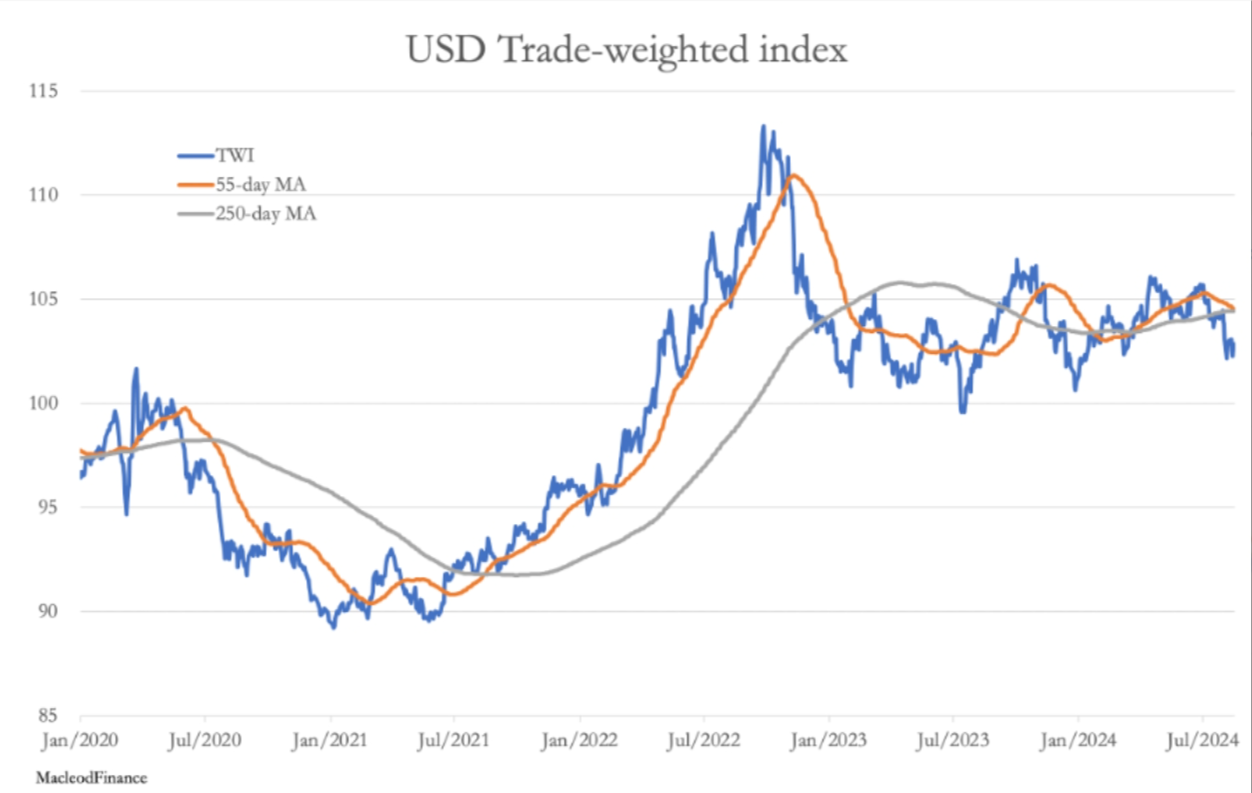

The answer is to be found in the dollar’s trade weighted index, which has turned sharply negative with the first death cross since the bullish golden cross in July 2020.

The occasions since then when price and moving averages have changed relationships have been indeterminate, but not this time.

The chart is below.

You may recall that gold ran up to all-time highs in early-August that year at $2070 intra-day, but Managed Money net longs had actually peaked at 238,000 before on 18 February when equities were crashing, and gold was only $1580.

Covid lockdowns began on 20 March, the Fed Funds Rate was cut to zero, and then gold soared to $2070 in early August.

Bizarrely, while gold soared Managed Money net longs fell.

But this was mainly due to short positions increasing from a record low of 1,556 contracts to nearly 58,000 — longs only fell by a modest 8,000 contracts.

It appears that rather than trading gold contracts, hedge funds were merely using gold futures to hedge swings in the dollar.

When you look at it this way, rather than being long gold futures in their collective minds they were short dollars as the dollar was beginning to turn higher.

They were then hedging a rising dollar by closing their short gold future positions, or just being stopped out.

Now hedge funds face a similar dilemma, but the other way round.

Instead of the dollar’s TWI moving into a bullish golden cross, it is in a bearish death cross. And it looks very bearish indeed.

So what can we expect from Managed Money?

They are likely to be stopped out of their gold future short positions, amounting to 25,929 contracts, and add to their longs.

Indeed, this already appears to be the case following Tuesday’s COT numbers.

By the way, all-time record longs were 300,070 contracts in September 2016.

And looking at the dollar, that sucker is going down.

0 comments:

Publicar un comentario