‘Range of uncertainties’ faces Federal Reserve at rate-setting meeting

Bond-yield surge and Israel-Hamas war cloud decision on whether to tighten monetary policy further

Colby Smith in Washington

Federal Reserve chair Jay Powell. The Federal Open Market Committee is poised to extend the pause in its monetary tightening campaign that has been in place since it last raised rates in July © JIM LO SCALZO/EPA-EFE/Shutterstock

Federal Reserve chair Jay Powell. The Federal Open Market Committee is poised to extend the pause in its monetary tightening campaign that has been in place since it last raised rates in July © JIM LO SCALZO/EPA-EFE/ShutterstockJust days before Federal Reserve officials hunkered down to prepare for this week’s policy meeting, chair Jay Powell conceded that the US central bank’s already difficult job had become even trickier.

“A range of uncertainties, both old and new, complicate our task of balancing the risk of tightening monetary policy too much against the risk of tightening too little,” the Fed chair told an event hosted by the Economic Club of New York.

Among the curveballs pitched at it are the deepening conflict in the Middle East that now looms over global oil markets, surging long-term interest rates, and stronger than expected economic data that has raised questions about how quickly inflation will moderate.

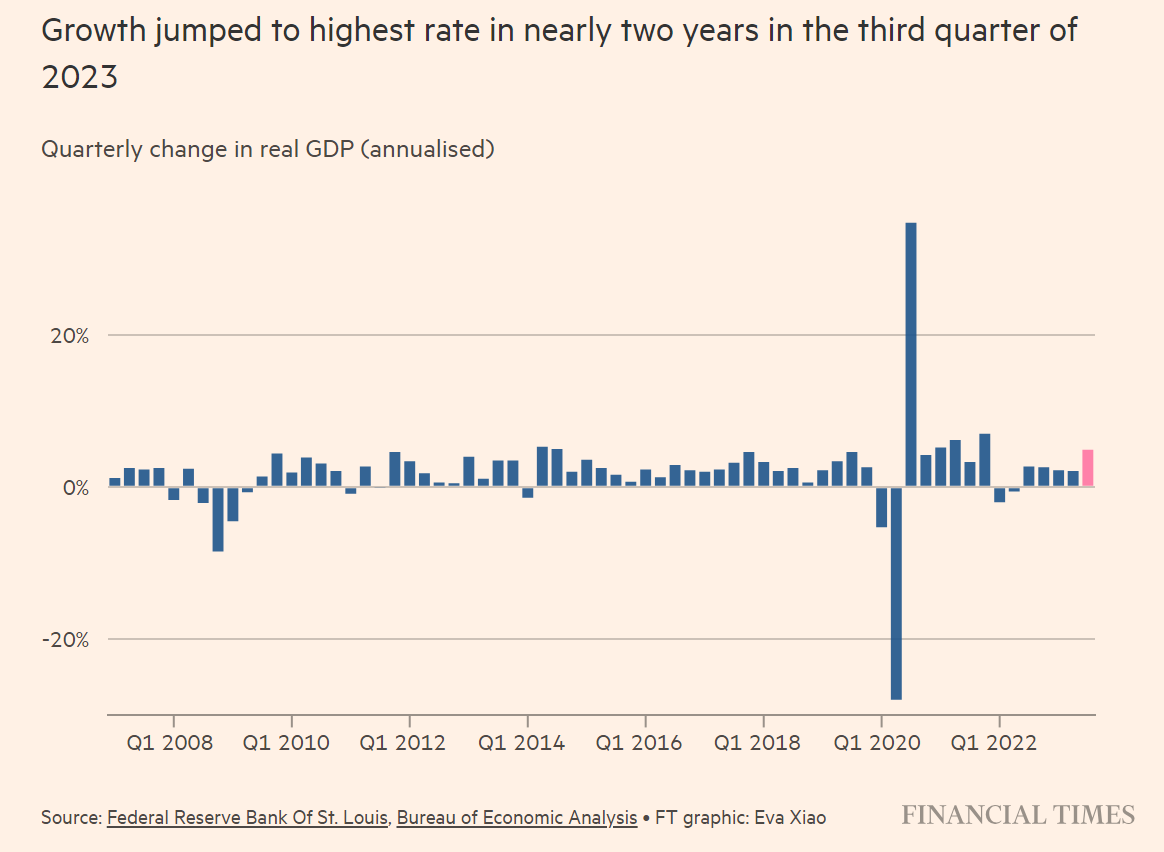

The Federal Open Market Committee is poised to keep its benchmark interest rate at a 22-year high of 5.25-5.5 per cent when its two-day meeting ends on Wednesday, extending the pause in its monetary tightening campaign that has been in place since it last raised rates in July.

That will give central bankers more time to assess not only the mixed signals about the US economy’s health, but also how the Fed’s past rate rises and a recent tightening of credit conditions are influencing consumer and business demand.

Market participants broadly wager that these cross-currents mean the Fed is done with the rate-raising phase of its fight against inflation — and will now shift the debate to how long rates should be kept at their current restrictive levels.

Officials themselves suggested this month that with price pressures still percolating it remained too early to rule out additional tightening, even as they insisted they would proceed carefully with policy decisions.

Powell and influential governors such as Christopher Waller have seemingly erected a high bar for additional tightening — suggesting recently that it would need fresh evidence that economic growth was not meaningfully slowing and that the disinflation process had either stalled or reversed.

But many economists argue that further tightening should not be ruled out altogether.

“Having recently faced high inflation, I think the Fed wants to err on the side of hawkish communication about the future until it has greater confidence that it has been addressed,” said Kris Dawsey, head of economic research at DE Shaw.

From continued signs of resilient consumer spending to the possibility of “spicier” inflation readings for the rest of the year, the data “could serve to reduce one’s conviction that the economy is actually going to continue cooling and inflation is going to be moving back towards 2 per cent”, he said.

Not only is a December rate rise a “very plausible outcome” without a more substantive let-up in inflation, Dawsey added, but if economic conditions warrant further tightening, it could well mean more increases beyond that.

As recently as September, officials projected that one more quarter-point notch higher in the fed funds rate would be necessary to deem the Fed’s policy settings “sufficiently restrictive”.

They also forecasted fewer cuts next year.

This embrace of a higher-for-longer policy approach helped to ignite a sharp sell-off in bonds that is seen both at the Fed and by others as doing some of the work for the central bank, by raising borrowing costs.

According to economists at Nomura, the surge in long-term yields is roughly equivalent to one or two quarter-point rate rises, which they said made it a “reasonable substitute” for the final increase officials had pencilled in at their September meeting.

Julia Coronado, a former Fed economist who now runs MacroPolicy Perspectives, cautioned that such a substantive move higher in borrowing costs would soon bite.

“We are not in a world awash in stimulus and liquidity.

We are in a world of extremely expensive money,” she said.

Any remaining froth is going to get “killed by higher rates” and if officials “go too hard, then they might end up having to reverse course too fast”, Coronado added.

Former Fed governor Laurence Meyer — who expects the central bank to skip a December rate rise but is “reluctant” to say the Fed has finished tightening — said next year’s debate would be tricky, focusing more on the “duration” of higher rates than their level.

The task will be for Fed officials to calibrate the fed funds rate such that as the pace of consumer price growth moderates, the real, inflation-adjusted policy rate does not become prohibitively restrictive for the economy.

Jonathan Pingle, who used to work at the Fed and is now chief economist at UBS, said he expected the central bank to slash its main interest rate in March 2024 — earlier than traders in futures markets are betting — and by the middle of next year to have reduced it by 0.75 percentage points as the economy tips into a recession.

“At the end of the day, it’s really the data that’s going to drive this,” Pingle said.

“They would like a slower economy, and if they get [that], then they are going to have to start thinking about how restrictive they really want to let policy get as inflation falls.”

0 comments:

Publicar un comentario