Why is the US economy so resilient?

High interest rates have not stopped businesses from hiring or consumers from spending — yet

Colby Smith in Washington

If 18 months of rising interest rates from the Federal Reserve were supposed to put a chill on the world’s biggest economy, US consumers had another idea.

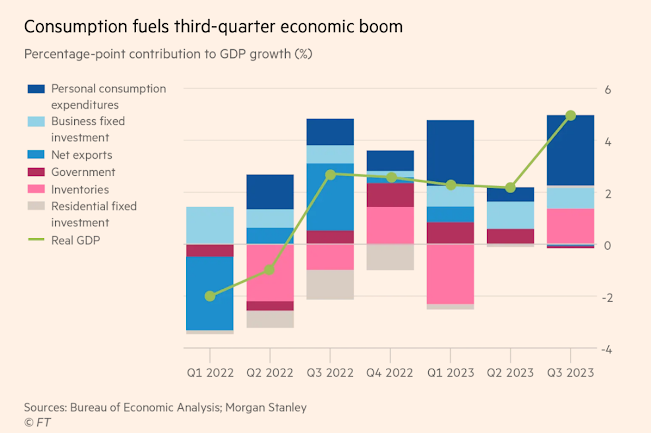

New federal data on Thursday showed the US economy expanded by an annualised rate of 4.9 per cent in the third quarter — a blistering pace that, not for the first time, defied gloomier predictions from economists.

“It has been an exercise in humility,” said Kathy Bostjancic, chief economist at Nationwide, referring to forecasters’ dim record since the pandemic.

What made Thursday’s explosive gross domestic product number — the strongest since 2021 — so surprising was what preceded it: the most aggressive campaign by the Fed to tighten monetary policy in decades.

The central bank has raised interest rates 11 times since March last year, to a 22-year high of 5.25 per cent to 5.5 per cent — all in an attempt to cool the economy and quell inflation.

Inflation has fallen.

But the economy remained far from subdued this summer.

Still, as off the mark as they have been over recent months, economists warn US GDP is unlikely to keep defying gravity for much longer.

The stunning resilience in the US economy to date has stemmed from one primary force: consumer spending, which was by far the biggest contributor to the economy’s boom in the third quarter, accounting for more than half of the annualised increase.

Buoyed by a healthy labour market, continuing demand for workers gave people confidence to keep buying.

“It has been incredible job growth really propelling consumer spending,” Bostjancic said.

Moreover, what had “turbocharged” this dynamic was a feeling among consumers that they were flush with cash.

“Balance sheets look in really good shape, stocks have generally performed really well, housing prices are very high, and even if you don’t have assets, you have this pool of pandemic-related savings,” she added.

But, like other economists and policymakers, Bostjancic expects this momentum to fade, especially as the Fed’s past interest rate increases bite, and companies and households struggle under the weight of the surging borrowing costs after government bond yields hit multiyear highs.

Signs that consumer strength is waning are visible.

Of more than $2tn in excess savings stockpiled since the pandemic, for example, economists estimate that the bulk has been drawn down.

Moreover, reckons Nancy Vanden Houten at Oxford Economics, what remains is concentrated among wealthier households.

Businesses are also turning more cautious.

Gregory Daco, chief economist at EY-Parthenon, said he thinks the US economic engine that performed so strongly in the third quarter is about to sputter.

He said: “All of the positive drivers of consumer spending were revving quite strongly over the course of the summer, but we’ve seen some of these drivers moderate quite significantly and expect [others to moderate] over the course of the coming months.”

Daco added: “If businesses start to feel the pressure of having higher debt servicing costs and low utilisation on the labour front, and if they start to feel the need to cut costs because they won’t necessarily be able to attain the revenues that they targeted, then that starts to create more of a snowball effect.”

Hints of “cost fatigue” were evident in the latest GDP data, Daco said, with non-residential fixed investment — which tracks businesses’ spending on machinery and other equipment — falling 0.1 per cent on a quarter-over-quarter basis.

That was the third decline in this category in the last four quarters — a sign, said economists at Morgan Stanley, that “higher rates are weighing on business activity”.

According to forecasts compiled by Bloomberg, most economists now expect US GDP growth to fall to 0.8 per cent next quarter — more than 4 percentage points below the third-quarter number — before bottoming out at 0.2 per cent in the first three months of 2024.

Ian Shepherdson at Pantheon Economics reckons growth could even drop to zero next quarter, although he acknowledged there is a wide margin of error.

Whether the US economy eventually tips into a recession, however, is a far more contested issue.

Janet Yellen, the Treasury secretary, on Thursday said the data does not suggest “any sign of recession”, even as she acknowledged that last quarter’s pace of growth is unlikely to be repeated.

Fed chair Jay Powell has also maintained there is still a path for a soft landing.

Daco sees the odds of a recession next year as even. But he was cautious about the forecasts.

“We’ve learned to be very humble in our ability to predict,” he said.

Additional reporting by Eva Xiao and Oliver Roeder

0 comments:

Publicar un comentario