This Time Really Is Different for the Economy. Just Look at the Job Market’s Confounding Strength.

Unemployment remains near historic lows even after the Fed's aggressive rate hikes. What's behind the job market's resilience---and why it could last.

By Megan Cassella

At the heart of the Federal Reserve’s 18-month fight to lower inflation has been a presumed trade-off between stable prices and a weakening labor market.

Mainstream economic thinking and decades of economic history both suggest that to wrestle price growth back to target, the central bank will have to slow the economy enough to drive up the unemployment rate, thereby putting millions of Americans out of work.

Otherwise, the theory goes, inflation persists, along with the hardships it causes.

At the heart of the Federal Reserve’s 18-month fight to lower inflation has been a presumed trade-off between stable prices and a weakening labor market.

Mainstream economic thinking and decades of economic history both suggest that to wrestle price growth back to target, the central bank will have to slow the economy enough to drive up the unemployment rate, thereby putting millions of Americans out of work.

Otherwise, the theory goes, inflation persists, along with the hardships it causes.

Since early last year, Fed officials have warned of the labor-market fallout that their attempt to cool prices probably would cause.

Fed Chair Jerome Powell called the anticipated pain an “unintended consequence” of the task at hand.

As recently as six months ago, the central bank’s own projections showed the jobless rate climbing more than a full percentage point, to 4.6%, by the end of 2024.

Believing in a more optimistic outcome would require an almost naive adherence to one of the most fraught phrases in economics: It’s different this time.

Except that, so far, it has been.

The Fed has lifted interest rates nearly a dozen times since March 2022, to a range of 5.25% to 5.5%.

Headline inflation has fallen by two-thirds, from a peak of 9.1% to 3% on a year-over-year basis, and despite a recent uptick is poised to slow further as rent prices cool.

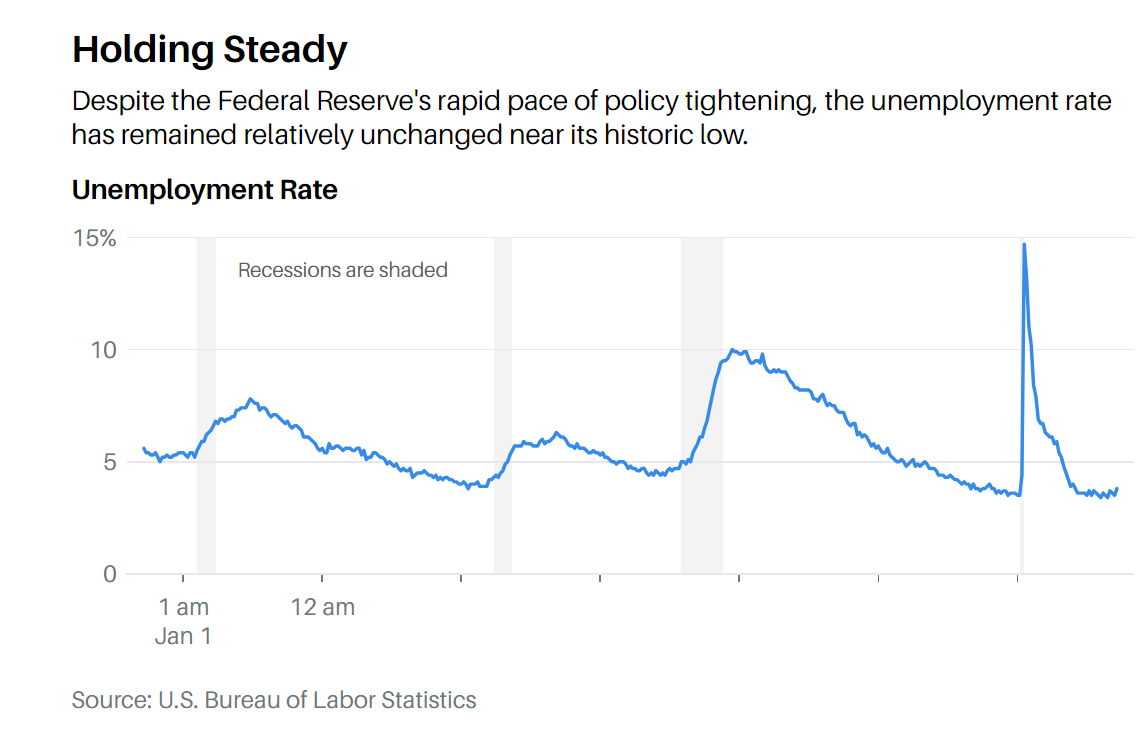

Yet, the U.S. unemployment rate sits at 3.8%, a historically low level only slightly above the 3.6% that prevailed when the Fed first began raising rates.

And there is little to suggest that unemployment will head much higher soon.

“Really, what we’ve been seeing is progress without higher unemployment,” Powell said at his most recent news conference, on Sept. 20.

The labor market’s persistent strength has surprised economists at the Fed, who have adjusted their unemployment forecasts down by half a percentage point, and those on Wall Street, where once-rampant recession predictions have been postponed or withdrawn.

It has also forced a rethinking of the ingrained assumption that labor-market weakness is a necessary step to restore price stability.

If it isn’t, as now seems possible, the central bank might finally achieve the elusive soft landing about which Fed officials—and so many others—have dreamed.

Understanding why the labor market has remained so strong could yield clues to how long it could last.

If the same factors that have kept unemployment so low can persist, then the central bank arguably can keep rates in restrictive territory and bring inflation down without having to force the economy through a painful transition.

If not, a downturn might come later than expected, but it will come eventually.

There is no single satisfactory explanation for what has gone right so far.

Instead, a delicate combination of factors appears to have bolstered the labor market, including generous fiscal stimulus, unexpectedly strong labor-force participation, a rebound in immigration, a boom in small-business creation, and continued growth in in-person services sectors, especially healthcare, following the Covid-19 pandemic.

Consumer spending has held up even as pandemic savings have run dry, helping the labor market grow. RICHARD B. LEVINE/ALAMY

Consumer spending has held up even as pandemic savings have run dry, helping the labor market grow. RICHARD B. LEVINE/ALAMYEach of these developments has helped either to boost labor supply or keep labor demand strong enough to withstand the impact of rate hikes.

Together, they have contributed to a period of such resounding economic strength that even as the labor market now slackens somewhat, the downshift looks much more like a return to normalcy than the start of a recession.

The job market was growing at “breakneck speed” in the past two years, says Nick Bunker, research director at Indeed Hiring Lab, part of the job-search site Indeed.

“So, a reduction in hiring intentions, or hiring itself, hasn’t led to a big spike in unemployment.”

To be sure, signs of cooling are more abundant than just a few months ago.

Employment growth has slowed to a three-month average pace of roughly 150,000 jobs added each month, down from about 240,000 added monthly over the previous three-month period.

Job openings are down 21% since the start of the year.

The temporary-help services sector—considered a leading indicator for the broader job market, given that employers tend to shed temporary help before moving on to broader layoffs—has now shrunk in size every month this year.

Viewing these trends in context, however, tells a less worrisome story.

Monthly job gains are far outpacing the level needed to keep pace with population growth.

Job openings are still 26% above prepandemic levels, and moving sideways rather than falling, according to Indeed data.

The temporary-help sector is shrinking only because the nature of the pandemic rebound and related labor shortages forced an unusual reliance on temporary help among companies that now have been able to recover and make permanent hires.

The path forward is murkier, but the prognosis, for now, is good.

“We don’t know what is going to happen over the next year,” says Mike Konczal, director of macroeconomic analysis with the Roosevelt Institute.

“But the story we have so far is an optimistic one.”

The healthier the economy is, the better-equipped it will be to withstand the drag from higher interest rates aimed at slowing consumer demand.

By the time the Fed first raised rates last year, the U.S. economy was resoundingly healthy—probably even stronger than many economists believed at the time.

Generous fiscal stimulus doled out to counter the economic impact of the Covid pandemic had been particularly helpful for low- and medium-income Americans, enabling them to pay down debts, improve their credit scores, and lock in low interest rates on fixed-rate mortgages and loans.

Those workers also saw some of the largest real wage gains among all workers, the Atlanta Fed’s wage tracker shows.

As a result, wealth among the bottom half of U.S. families increased by nearly 75% from the first quarter of 2020, when Covid hit, to the first quarter of 2023, according to recent Fed data.

And it is holding strong.

That helps to explain why consumer spending has held up even as pandemic-era excess savings run dry.

While lower-income households spend less overall than their higher-income counterparts, they spend a greater share of their income and can have a significant impact on the rate of change in consumer spending when they begin to pull back.

Continued healthy spending has helped the labor market grow—which, in turn, fuels even more spending.

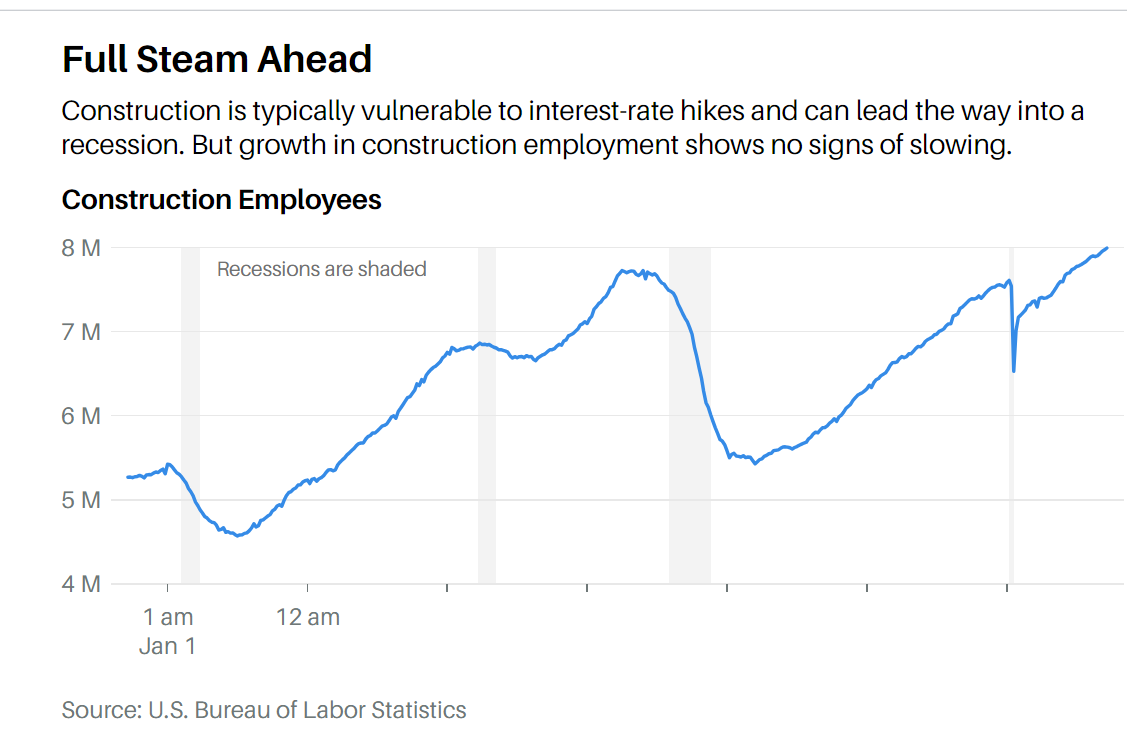

Fiscal spending has also been critical for the construction industry, which traditionally has been vulnerable to rate hikes that increase the cost of homes, cars, and manufacturing projects.

The hundreds of billions of dollars the federal government approved in the early years of President Joe Biden’s term to boost domestic chip manufacturing and rebuild the nation’s infrastructure all but ensured that demand for manufacturing projects wouldn’t fade, even as borrowing costs surged.

The spending was structured to incentivize private investment in the sector alongside public funding, further fueling building activity and stoking demand for more labor.

Employment in the construction sector continues to grow. Above, new-home construction in Buckeye, Ariz. MARIO TAMA/GETTY IMAGES

Employment in the construction sector continues to grow. Above, new-home construction in Buckeye, Ariz. MARIO TAMA/GETTY IMAGESResidential construction has also boomed after years of depressed building activity following the 2007-08 housing crisis left the country with a lack of supply of single-family homes.

That dearth coincided with a spike in demand as millennials reached peak homebuying years and remote-work policies allowed for migration out of urban centers.

Plus, as interest rates climbed, fewer homeowners who had locked in the prior years’ ultralow mortgage rates listed their homes for sale, exacerbating supply constraints.

Demand shifted to new homes, which began to contribute a larger share of total home sales.

Construction spending soared as a result, increasing more than 31% since February 2020, with no sign of a peak in sight.

Employment in the sector is up 5% in the same span, and continues to rise.

“The usual sort of crash in construction employment that happens when the Fed raises rates just didn’t take place,” says Julia Pollak, chief economist with ZipRecruiter.

Another source of surprising strength: the small-business sector.

Small firms are responsible for nearly two-thirds of all new job postings, so their health is vital to keeping labor demand strong.

Higher interest rates were expected to hurt small-business formation by making start-up costs, including loans, more expensive.

The collapse of several U.S. banks in the spring also was forecast to have a negative impact by making it harder for upstart firms to secure necessary financing.

But the slowdown never materialized.

Monthly business applications hit record highs when the economy reopened in 2020, and the trend has remained strong.

After leveling off in 2022, new-business applications are up again since the start of this year, and are 55% above February 2020 levels, census data show.

Even more important, the data show that these new firms are highly likely to hire.

So-called “high propensity” business applications—for entities likely to turn into operating companies with payrolls—are up by more than a third since just before the pandemic hit.

The strong economy, fiscal stimulus, and a booming small-business environment all helped keep demand for labor from collapsing as the Fed worked to slow the economy.

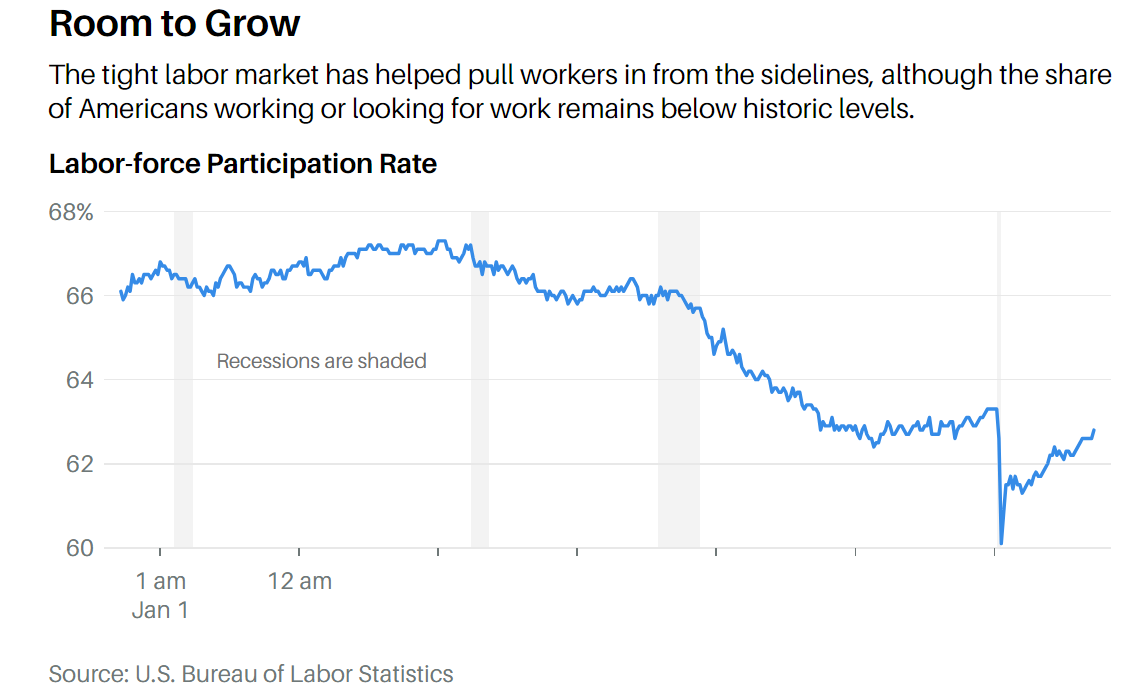

The other crucial development was a rise in labor-force participation, which boosted supply.

Overall labor-force participation—or the share of Americans either working or looking for work—took a severe hit after the Covid pandemic started, and at a current 62.8%, has yet to fully recover.

But an uptick in immigration and a record-high share of prime-age working women have both helped to boost participation rates above expectations.

Before Covid hit, the government had projected that the overall participation rate would fall to below 62% by the end of next year, largely due to more retirements as the U.S. population ages.

Crucially, participation could be poised to keep rising.

Department of Labor data show that the share of people moving into employment after being disconnected from the labor force—meaning they found a job without spending time searching for work—is at elevated levels, notes Elise Gould, a senior economist with the Economic Policy Institute.

That, she says, means “the reserve of workers is much larger than the unemployment level would suggest.”

“It means there is still room to grow,” Gould adds.

There is reason to think that most if not all of these trends can last.

Continued growth in the labor supply, as Gould suggests, would be one critical step toward a soft landing because it would help to rebalance the job market and reduce upward pressure on wages without destroying employer demand.

If that trend can hold, so can the strong labor market.

Increasing worker productivity also could help.

Diane Swonk, chief economist with KPMG, calls productivity enhancement “the No. 1 way we can actually sustain wages without having to have an increase in unemployment.”

Productivity is difficult to measure and has been sluggish for most of the past decade.

But Swonk and other economists think that could be starting to change, in part because the remarkable labor-market churn of the past few years has allowed workers to shift into better-fitting jobs where they can do better work.

As the quits rate slows and workers settle into their new jobs, output should increase, as well.

At the same time, the growing use of artificial-intelligence technology should soon start to boost productivity in a major way—and could be doing so already.

Chad Syverson, a University of Chicago economist whose research is focused on this area, has done work that suggests productivity is undermeasured when a new technology is just taking hold, as AI is now, because its output is intangible.

“It is worth keeping in mind that maybe we will be understating true productivity growth for a while,” Syverson says.

It is impossible to know where the economy is headed.

A resurgence of inflation that would demand sharply higher interest rates than expected would make it much more difficult for the labor market and the broad economy to maintain their current strength.

For now, though, it is clear that the recent moderation in job growth has yet to dent the labor market, which remains remarkably resilient even in the face of high inflation and rising interest rates.

The Fed’s ultimate goal is to rebalance supply and demand in the labor market.

Its tools work to tamp down demand, and the decline in job openings shows that its efforts are working.

But healthy consumer spending, heightened fiscal stimulus, and rampant small-business creation have all helped to ensure elevated demand, while rising participation levels are easing supply problems and new technologies are poised to help workers produce more with less.

There is notable progress, in other words, on both sides of the rebalancing equation, even as unemployment remains low.

Following through on this progress and successfully reaching equilibrium without forcing a surge in layoffs would be unprecedented in modern times, especially given how high inflation surged and how rapidly the Fed raised rates once it started.

Then again, much of what the labor market—and the broad economy—has experienced in the past three years hasn’t been seen before, either.

“I do think this time is different,” Pollak says.

“Because we’re coming from a completely different place.”

0 comments:

Publicar un comentario