Does China’s Property Bust Make a Financial Crisis Inevitable?

Perhaps not—if Beijing plays its cards right. But serious damage to the nation’s prospects is still likely. A look at the problem in five charts.

By Nathaniel Taplin

When property markets go bust, banks often follow—most famously in the U.S. in 2008.

Now China is in the midst of its own property blowup, with major developers teetering and housing sales—in floor space terms, year-to-date—at levels last seen in 2015. Does that mean a financial crisis is in the making?

Not necessarily, thanks to some surprising quirks of China’s housing market and Beijing’s heavy hand in the financial system.

But the cost will likely be serious damage to bank balance sheets, impairing their ability to support growth for years.

Moreover, widespread financial turbulence can’t be ruled out—especially if housing and land prices fall too fast—or if Beijing doesn’t do more to support cash-strapped local governments and small lenders.

Property is the heart of China’s economy, driving around a quarter of total economic activity.

But both banks and China’s “shadow banks” like trust firms have rapidly shed property exposure in recent years.

Total loans to property developers and home buyers peaked at nearly 30% of commercial banks’ loan books in 2019, according to central bank data.

That had fallen to just 23% by mid-2023.

Moreover, the biggest chunk—individual home mortgages—is probably relatively safe due to the way they are structured in China.

Down payments are large and loans tend to be recourse, meaning banks can go after other assets besides the house if homeowners walk away.

Indirect exposure

Unfortunately, banks’ seemingly manageable direct exposure to property is deceptive because of the housing market’s deep links to two other key borrowers: Heavy industry and local governments.

Heavy industries such as steel feed directly off construction, while local governments, especially in smaller cities, finance themselves with land sales to developers.

The good news is that, with the exception of steel itself, the heavy industries at the heart of China’s last big debt and housing crisis in 2015—metals, coal, cement and chemicals—are in better shape than they were last time around.

Total profits from metal smelting, building materials, coal and chemicals were about six times as large as their interest payments in mid-2023.

In 2015 and early 2016, that ratio dipped below two—one key reason for the big spikes in NPLs and bond defaults in those years.

Going local

The bad news is that another heavily indebted sector that ran into trouble in 2015—local governments—may actually be worse off this time.

Local governments in China, especially poorer inland ones without big corporate tax bases, have long relied on land sales and transfers from Beijing to plug their budget gaps.

But over the past decade, debt and land have become increasingly critical funding sources.

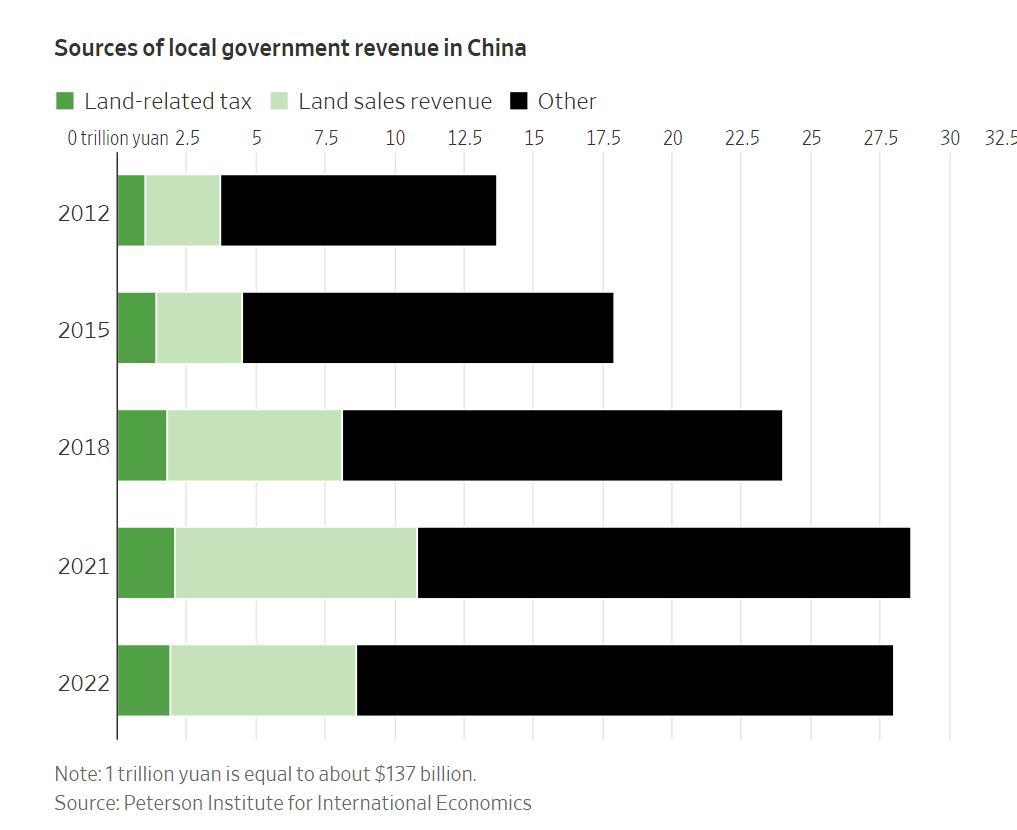

For local governments as a whole, land sales and land-related taxes were 25% of revenue in 2015, according to Tianlei Huang at the Peterson Institute for International Economics.

By 2021, that had risen to 38%.

Local governments have also racked up an enormous collective debt pile—much of it held by local banks.

Property developer debt was only 5.7% of banks’ loan books in mid-2023.

But local government borrowings through corporate financing vehicles comprised at least 11% of bank loans, according to consulting firm Gavekal Dragonomics.

And the total figure is likely significantly higher since that estimate was calculated using publicly available bond prospectuses, which also list the issuers’ other borrowings, including bank loans.

Many such municipal financing vehicles, especially in smaller cities, are probably unable to access bond markets and depend on banks instead.

Rolling over

The real problem for banks, therefore, probably isn’t mortgage exposure.

Rather, it is that the continuing property buyer’s strike among households is starving developers and local governments, two of the economy’s biggest debtors.

Moreover, local-government-owned corporate financing vehicles have also issued substantial bond debt.

And rather than risk market turbulence from bond defaults, authorities could lean heavily on banks to relieve pressure on local government balance sheets by quietly restructuring or rolling over bad loans while keeping bonds current.

That will heap further pressure on bank balance sheets.

Total local government debt was equal to about three-quarters of gross domestic product in 2022, according to estimates from the International Monetary Fund.

And much of this is likely backed by low or negative-return infrastructure projects.

China’s biggest banks are still in good shape.

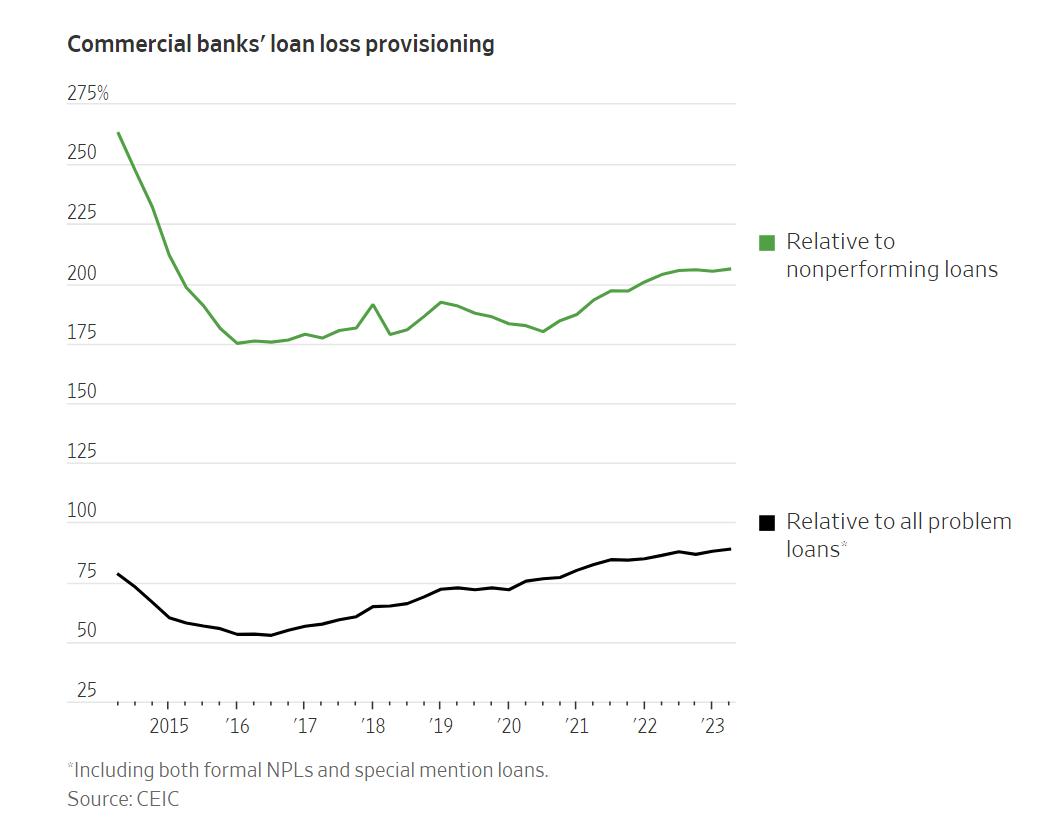

In the banking system as a whole, funds set aside to cover potential loan losses were equal to 89% of all loans currently marked as of concern—including formal NPLs and also so-called special mention loans.

In 2015, loan loss provisions were only 56% of problem loans.

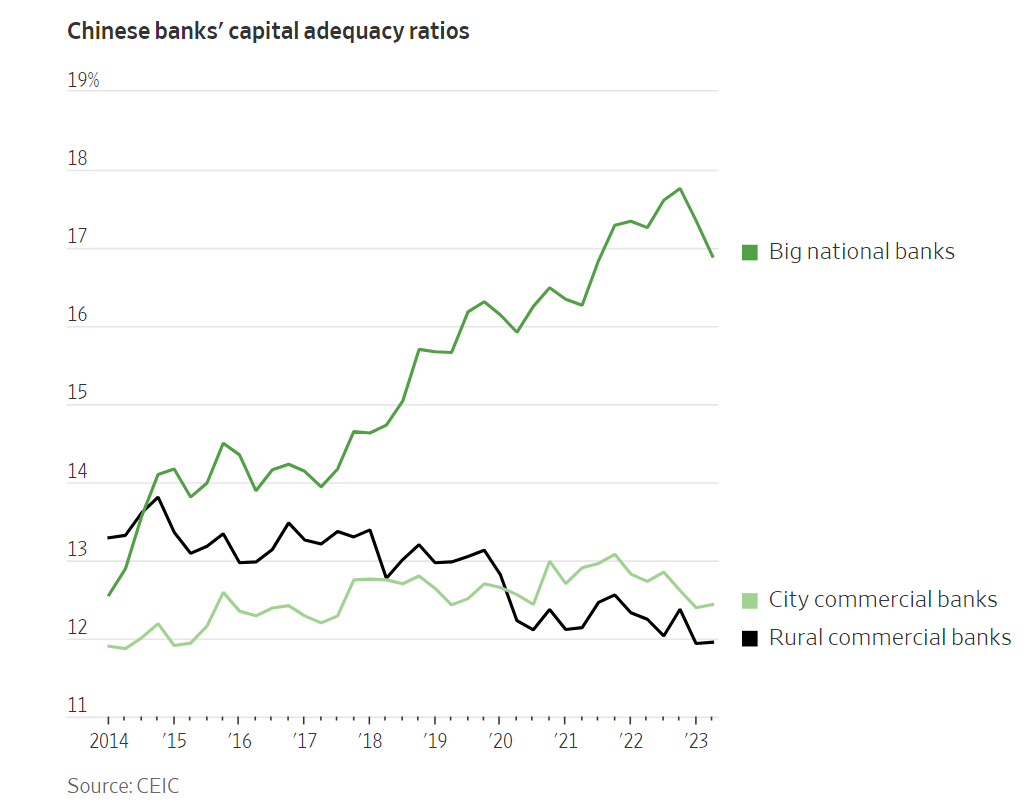

But the picture looks less rosy at smaller and particularly rural banks.

Big banks’ capital adequacy ratios have marched much higher since 2017.

But that has been mirrored by deteriorating capital buffers at many smaller banks—in part because of tougher restrictions on shadow banking activities, which used to be a key profit driver.

Gavekal reckons that a 1.5 percentage point rise in NPL ratios would push rural banks’ capital adequacy ratios below the regulatory minimum of 10%.

In the last big property downturn from mid-2014 to mid-2016, rural banks’ NPL ratio rose about 1 percentage point.

Relief measures

Authorities are well aware of the risk to rural banks and local government finances.

They have been aggressively recapitalizing small banks since 2020.

And on Wednesday, the northern province of Inner Mongolia said it was issuing 66 billion yuan—or about $9.1 billion—of “special refinancing bonds” to help repay higher interest debt issued before 2018.

A similar program launched in 2015 ultimately helped refinance trillions of yuan in off-balance sheet municipal debt.

That swap, along with a state-financed slum redevelopment program, probably helped China stave off a much worse municipal, property and industrial debt crisis in 2015 and 2016.

Still, the sheer size of property and land related financial flows—total land sales revenue was 6.7 trillion yuan in 2022 according to Huang at the PIIE—means that bailing out small banks and city governments without bailing out the property market may ultimately prove difficult.

There is some good news on that front.

Since late August, Beijing and local governments have both begun rolling out much more aggressive steps to support the property market.

And rural banks, which are in the worst shape, usually aren’t heavy borrowers from other financial institutions, which could limit direct spillovers from any bank failures.

As a whole, rural financial institutions are a significant, if not a large part of the financial system: about 13% of banking assets.

China may well avoid a systemic financial crackup in 2023 and early 2024.

But it is unlikely to avoid serious damage to banks’ balance sheets—even at healthier lenders.

That will have its own costs: less cash available to support small businesses and grandiose industrial policy, and ultimately, probably slower growth.

0 comments:

Publicar un comentario