Should we worry about corporate debt levels?

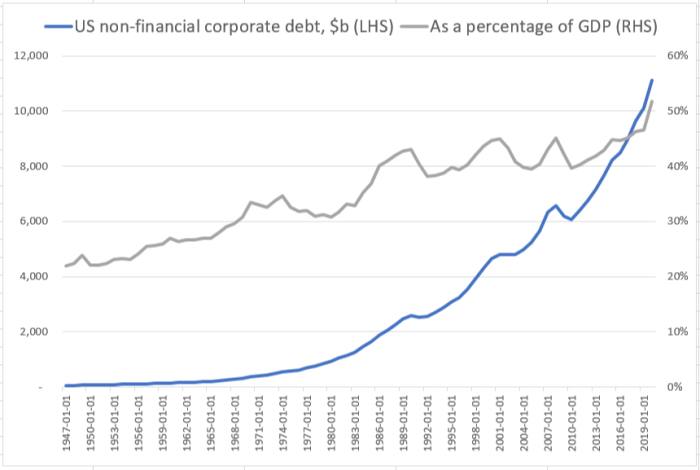

Here’s a chart you might worry about, if you were in a worrying mood. From the national accounts:

Corporate debt has never been higher, neither in absolute terms nor relative to GDP.

From 2010 to 2020, corporate debt grew at over 6 per cent a year, almost twice the rate of the economy.

This seems a little spooky.

At finance school, they teach you that as companies depend more on debt for financing, their returns and earnings per share rise, but they become less stable in the face of financial stress, because debt costs are rigid, and debt has to be paid back.

So in theory we should be worried that all this debt will make the next recession or financial crisis worse.

And recently people mention this risk quite often.

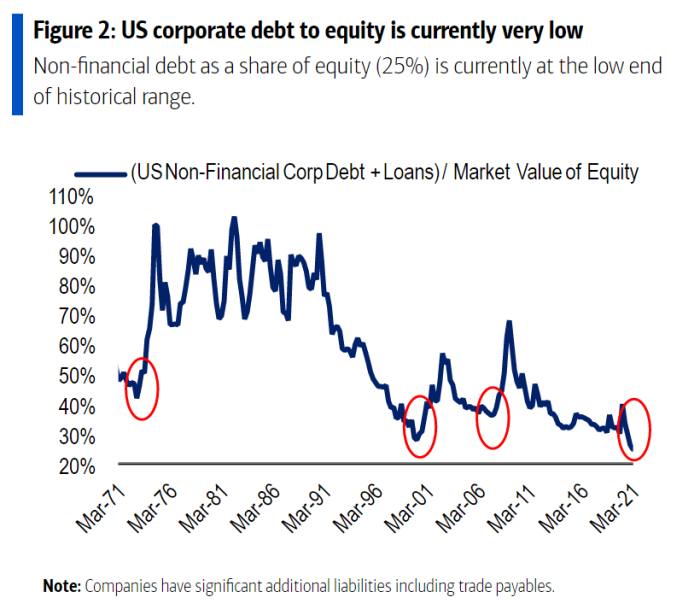

But Hans Mikkelsen, credit strategist with Bank of America, thinks that we can relax a little, because of this chart:

Stock prices have risen even faster than levels of debt.

Mikkelsen writes that “claims of US corporate bond and loan investors have never been backed by more equity value”.

That doesn’t strike me as at all reassuring.

If a company, or companies in general, get into a nasty situation where servicing or rolling over their debt is a worry, that equity value is going to disappear fast.

It is an umbrella companies can only use when the sun is shining.

Mikkelsen goes on:

Providing an offset to that benefit, the bar is set really high for companies to justify equity valuations organically without leveraging up.

That means large BBBs [companies rated at the bottom rung of investment grade] and financials, for which maintaining ratings is important, are the sweet spots in investment grade credit.

Finally note that both equities and credit struggled following prior lows in this leverage ratio (end of 4Q-72, 1Q-00 and 2Q-07).

Mikkelsen likes the debt of companies that are constrained from adding even more debt, suggesting he isn’t all that reassured by equity value, either.

And his reference to the fact that stocks and debt struggled after what he calls the “leverage ratio” hit lows shows exactly why.

The ratio gets low when stocks are really expensive, that changes when bad things happen (1972, 2000, 2007, where the little red circles on his chart are), and when bad things happen is when defaults becomes a problem.

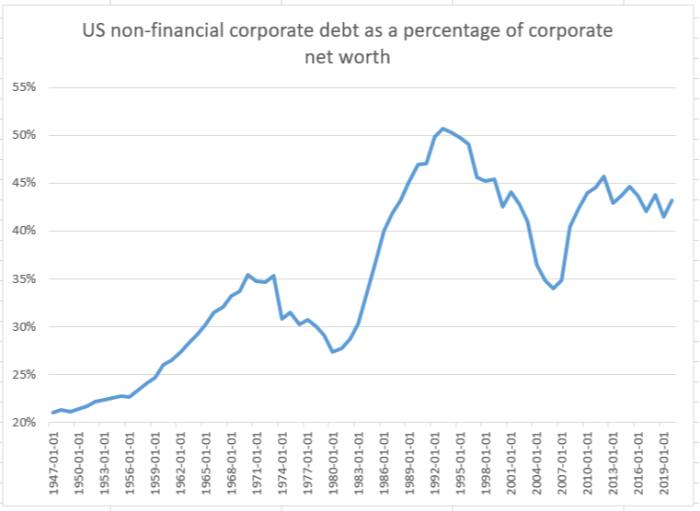

But there is another way to look at this.

Here is total corporate debt as a percentage of corporate net worth, that is, equity value in the balance sheet rather than the stock market sense:

Leverage in this sense is higher than in Mikkelsen’s sense, but it is right at its 30-year average.

And isn’t this the kind of leverage we should be worried about?

The problems start when your debt is almost as much as, or more than, your assets.

Looking at that last chart, it doesn’t look like US companies have that problem right now.

So I’m not terribly inclined to put corporate debt on my list of pressing worries.

Am I missing something?

Median and mean valuations

Among the investment cognoscenti/Twitterati, reading Barron’s is not considered cool.

It’s your dad’s investment magazine, basically, and talking about something you read there risks people thinking that you wear suspenders, believe the Dow is a good index to follow, and still think in eighths.

Well, I like Barron’s, whatever kids today think, the little punks.

Reading it this weekend, I was struck by this interview with Doug Ramsey, who manages the Leuthold Core Investment Fund.

He said:

I was of the view that the late-1990s stock mania was a once-in-my-lifetime event, and here we are just 21 years later and I would argue that this market is, broadly speaking, more expensive than what we saw in the tech bubble. Back then, the high valuations were concentrated in the top 40 to 50 stocks. Today, the median stock valuation across the market is the highest it has ever been. At the end of July, the S&P 500 median normalised price/earnings ratio was 34.2. In February of 2000, the month-end peak of the tech bubble, it was 22.2.

The idea that the market now is expensive everywhere, rather than being top-heavy, is interesting for a couple of reasons.

One, it’s not what I would have expected, given how high-valuation tech companies have led the market upwards in this cycle.

Two, for people like me who received their basic financial training as value investors, it’s bad news.

We cling to the (possibly irrational) hope that if we search out reasonably priced stocks this will protect us when the market finally falls.

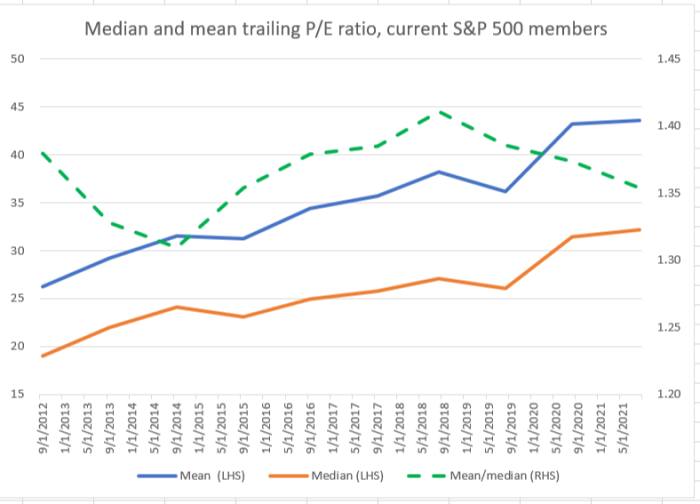

So I decided to give the data a look myself.

I took the valuations of the companies in the S&P every year over the last ten years and calculated the mean and the median, on the theory that if the mean is rising further and further above the median, we have an increasingly top-heavy market, which could be vulnerable to changes in fortunes of a relatively small number of stocks, but where value still might be found.

Alternatively, if the median is rising toward the mean over time, overvaluation is reaching every corner of the market.

What I found, instead, was hardly any change at all in the relationship of the mean and median (data from S&P Capital IQ):

The ratio of mean to median moves a bit, but only within a tight range, from 1.3 to 1.4.

It doesn’t look like we are getting more top-heavy in the last decade.

But I have to admit an embarrassing shortcoming of my data.

It measures the valuation, over the last ten years, of the companies that are in the S&P now (I can’t figure out to make Capital IQ adjust for historical changes in the index constituents; if you know how to do this, email me).

So it is possible that adjusting for changes in the index over the years would give a different result.

That said, I find the stability of the ratio interesting.

0 comments:

Publicar un comentario