AT&T Is Cutting Its Dividend and Spinning Off WarnerMedia. Here’s How Much Its Stock Might Be Worth.

By Nicholas Jasinski

AT&T said it would “reset” its dividend as part of the transaction, to a payout ratio of about 40% of free cash flow. Gabby Jones/Bloomberg

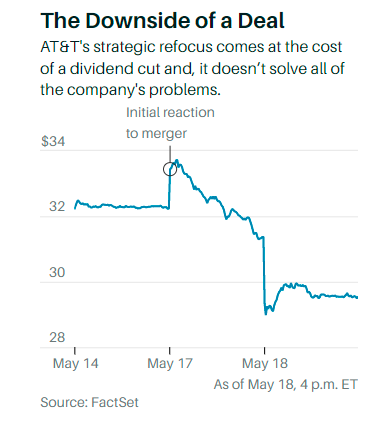

AT&T stock was the biggest loser in the S&P 500 on Tuesday, a day after announcing a megadeal to shed its media assets and focus on its 5G and fiber-internet telecom core.

That strategic refocus was seen as a positive by investors and analysts, but it comes at the cost of a dividend cut after the proposed spinoff closes.

Worse still, it doesn’t solve all of the company’s problems.

AT&T stock (ticker: T) lost 5.8% on Tuesday, to close at $29.55, after losing 2.7% on Monday.

Shares of Discovery (DISCA), which will combine with WarnerMedia, fell 1.6%, to $33.31, extending Monday’s 5.1% decline.

The deal will provide AT&T with $43 billion in cash and other assets to pay down debt. AT&T shareholders will own 71% of the combined WarnerMedia/Discovery, with Discovery shareholders owning the rest. Discovery CEO David Zaslav will lead the company, and the merger is expected to close in the middle of 2022.

AT&T said it would “reset” its dividend as part of the transaction, to a payout ratio of about 40% of free cash flow, which management estimates at least $20 billion in 2023.

That means roughly $8 billion in annual payout, or some $1.11 per share (AT&T has about 7.19 billion shares outstanding, per its latest filing).

Should the post-spinoff equity trade for the same annual dividend yield as Verizon Communications ’ (VZ) current 4.3%—given a similar leverage and business profile—it would be worth $186 billion, or about $25.88 per share.

Several Wall Street analysts did a version of that math this week, and came up with similar values for AT&T’s telecom businesses after spinning off WarnerMedia.

Valuing the newly created media company is a tougher task, and depends on investors’ views of its future streaming prowess.

Management said Monday that they expect WarnerMedia/Discovery to generate about $13 billion in adjusted Ebitda—short for earnings before interest, taxes, depreciation, and amortization—in 2023, and to be levered at 5 times net debt to adjusted Ebitda at closing. That implies about $65 billion of net debt on the new entity.

The market ascribes vastly different multiples to streaming winners and legacy media players. Walt Disney (DIS), which has a runaway streaming success in Disney+, trades for 17.3 times its enterprise value to 2023 Ebitda estimate, while streaming pure-play Netflix (NFLX) goes for 22.3 times.

Relatively subscale media companies ViacomCBS (VIAC) and premerger Discovery each trade for about 8.5 times their 2023 EV/Ebitda ratio.

WarnerMedia/Discovery will bring HBO Max and Discovery+ under one roof, plus a deep library of content from their multiple brands and a combined annual production budget of about $20 billion, per management.

But the business today is more of a collection of cable networks and a Hollywood movie studio, with the streaming services not expected to turn a profit for several years.

Every weekday evening we highlight the consequential market news of the day and explain what's likely to matter tomorrow.

At a Disney-like multiple of 17 times 2023 Ebitda, WarnerMedia/Discovery would have an enterprise value of $221 billion and its equity would be worth $156 billion after subtracting net debt.

AT&T shareholders’ 71% stake would be worth $110.8 billion, or about $15.40 per current AT&T share, if the stock gets the same credit from the market as Disney’s.

At an 8.5 times EV/2023 Ebitda ratio in line with ViacomCBS’ and Discovery’s today, the same math yields a value of about $4.49 per share.

Add the $25.88 value of AT&T’s telecom businesses, and AT&T stock today could be worth between $30.37 and $41.28—depending on whether investors believe WarnerMedia/Discovery will look more like ViacomCBS or Disney in the future.

The reality is likely to be somewhere in between. But after a nearly 10% selloff in the past two days, AT&T stock is trading below both of those values.

Another way to play the transaction is via Discovery stock, which will morph into a 29% stake in the combined media company.

With a fully diluted market value of $22.5 billion at Tuesday’s close and net debt of about $13 billion, Discovery’s $35.5 billion enterprise value implies a $122.4 billion enterprise value for WarnerMedia/Discovery.

AT&T shareholders’ stake in the media company would be worth $40.8 billion after debt, or $5.67 per share.

For now, the market seems to be valuing WarnerMedia/Discovery much more like ViacomCBS than Walt Disney.

0 comments:

Publicar un comentario