Spain Becomes Europe’s Weak Link

The Spanish economy is suffering from a particularly bad resurgence in Covid-19 cases as well as its outsized exposure to tourism

By Jon Sindreu

Once a rising star of the European economy, Spain is on a path to becoming its problem child—and the latest example of why global investors should tread carefully around Southern European stocks.

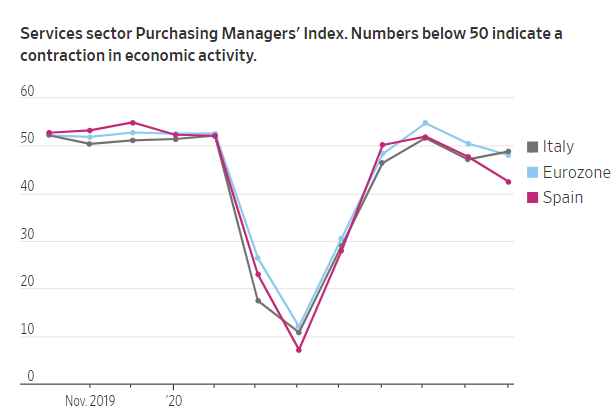

This week, the latest readings of the purchasing managers index published by IHS Markit confirmed two trends. The first is that global manufacturing activity is recovering at a much faster pace than services. The second is that, among big developed countries, Spain seems to be in particular trouble.

The pandemic has made these polls of companies more difficult to interpret than usual. Still, they show Spain performing worse than its European peers, including Italy, which was the economic laggard coming into the crisis and was worse hit by the first wave of Covid-19 cases.

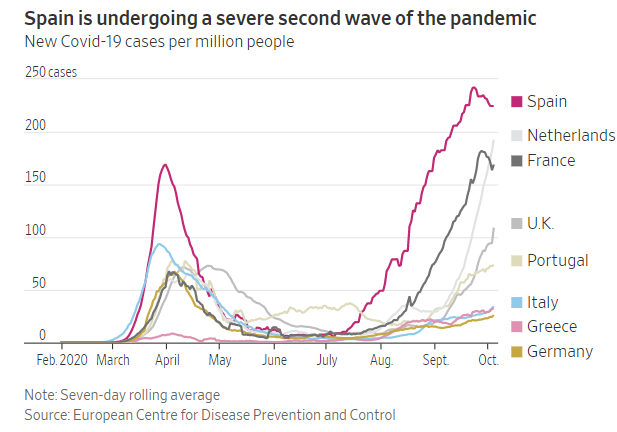

Spain has been unable to contain the spread of the virus.

In the spring, officials took too long to act, only to later establish the strictest of lockdowns.

Unlike Italy, the country then tried to return to normal too fast—its leader of health emergencies went abroad on vacation just weeks after advising against travel between provinces.

Infection rates rebounded sharply in the summer, such that Spain accounted for one-third of Europe’s daily Covid-19 cases. Now, Madrid is one of the region’s hardest-hit cities, and new measures that directly impact the services sector have been enacted.

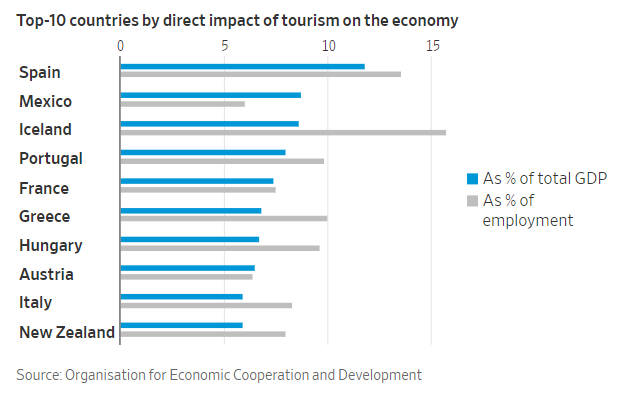

The structure of Spain’s economy, which enjoyed a growth spurt between 2015 and 2019, explains why it is at risk now.

Official figures suggest that half of the one million jobs lost during the depths of the outbreak have already been recovered. But there are an additional 735,000 being propped up by subsidized furlough programs.

Many are tourism-related roles that will probably disappear as soon as support ceases.

The real unemployment rate is likely well above 20%, rather than the official 15%.

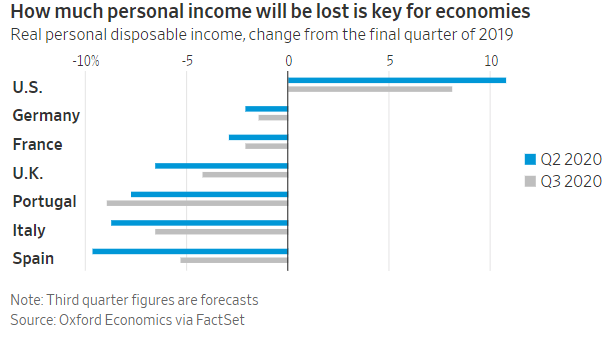

In the medium term, what is even more important for all economies is how much money consumers have once the pandemic is over. Reduced earnings could depress demand for years and even cause a double-dip recession.

In the U.S., an expansion of unemployment subsidies and stimulus checks led personal income to increase more than 10% in the second quarter even as people lost their jobs. In Southern Europe and Spain in particular, by contrast, income losses have been very steep, Oxford Economics analyst Ángel Talavera has pointed out.

The reason is that these governments have been less willing or able to widen their budget deficits by opening their purses, despite support from the European Central Bank. While Oxford Economics forecasts a rebound in Spanish personal income in the third quarter, the economic gap with richer nations is likely to widen from here.

European reconstruction funds will probably arrive too late—over the past week, governance questions have put the timing further at risk—and won’t fix Spain’s overreliance on relatively unproductive industries like tourism.

A big question for investors over the past few months has been whether to tilt their portfolios from the U.S. to Europe. The pain in Spain is a warning of the dangers involved.

0 comments:

Publicar un comentario