Region’s weak economies appear ill-equipped to cope with a rapid rise in borrowing

Michael Stott in London and Andres Schipani in São Paulo

Women health workers pictured in Buenos Aires. Latin America struggled with multiple issues before the pandemic, from weak health systems to high levels of borrowing © Ronaldo Schemidt/AFP/Getty

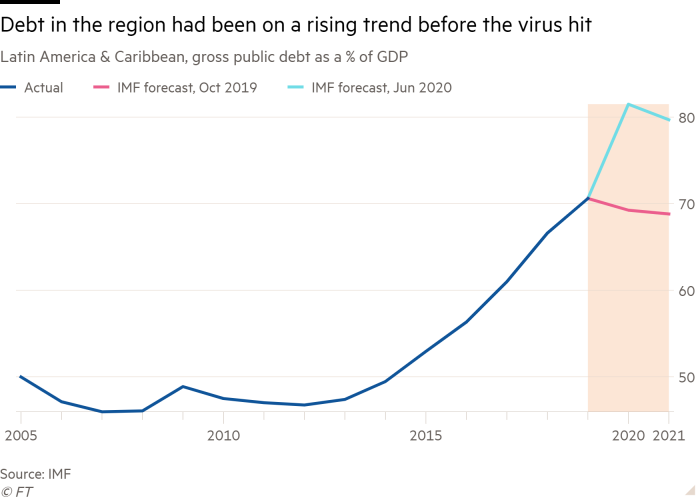

Latin America is at the centre of the coronavirus pandemic, suffering some of the worst infection rates and highest death tolls in the world. Now economists warn that the region faces more bad news: its sickly economies risk falling into a new debt crisis even worse than the last big bust of the 1980s.

The continent was struggling with multiple “pre-existing conditions” before the virus took hold: anaemic growth, weak health systems, low tax revenues, high levels of borrowing and an over-reliance on commodity exports.

Now some of the longest lockdowns in the world, together with the accompanying costly rescue programmes, have wreaked havoc on public finances. Chile, Brazil and Mexico were among the five emerging markets globally with the biggest increase in debt to GDP this year, according to the Washington-based Institute for International Finance. Chile's total debt rose 30 per cent year-on-year in the first quarter.

Latin America “already had a lot of debt before the crisis,” José Ángel Gurría, secretary-general of the OECD, told the Financial Times, adding that after the “brutal reality” left by the virus the region would need much “greater resources and/or relief on its debt”.

Government borrowing in the region is spiralling, alarming investors. “It’s definitely the elephant in the room,” said Claudio Irigoyen, head of Latin American research at Bank of America, of the debt problem.

“The trade-offs in Latin America are much worse than in other regions. There’s a very under-developed health and sanitation system, which dictates strict lockdowns, but there’s also a very high degree of labour informality which means you can’t extend the lockdowns in time or you risk social chaos.”

Residents of Heliópolis, São Paulo, line up for a food donation © Alexandre Schneider/Getty

Advanced economies can tap vast resources from central banks because they have strong currencies and investors willing to continue buying their debt. Latin American countries have no such safety net and labour under the weight of a history of debt crises stretching back more than a century.

Argentina and Ecuador are already in default on their foreign debt and are negotiating restructurings. Argentina has adopted a more confrontational stance, while Ecuador has won praise for a more consensual approach. Neither has yet agreed a deal with all bondholders.

Brazil, the region’s largest economy, has seen its debt rocket as its precarious public finances feel the impact of a deep recession and sharply increased government spending. William Jackson at Capital Economics forecast that Brazil’s debt-to-GDP ratio could jump to close to 100 per cent this year from 76 per cent last year. “It’s a ticking time bomb,” he said.

Alberto Ramos, chief economist for Latin America at Goldman Sachs, said Brazil needed to convince investors that it could get its public finances back on track. “If you start with a very fragile fiscal position, you will come out with an even uglier fiscal position which requires . . . the right signalling from policymakers that this was just a one-off expansion . . . and that after that you will embrace a fiscal adjustment,” he said. “The biggest fear in the market is when exactly the authorities will embrace such an adjustment.”

President Jair Bolsonaro’s government insists that pro-market reforms are still alive and will resume later this year. But Brazil faces elections in 2022, making it highly unlikely that ministers will adopt painful austerity measures ahead of the vote.

Mexico, the region’s second-largest economy, started the pandemic with relatively sound public finances and low levels of debt. However, President Andrés Manuel López Obrador’s decision to press on with an austerity programme, instead of spending to save the economy, is likely to deepen the country’s recession and stymie its recovery.

The IMF forecasts that Mexico’s GDP will plummet 10.5 per cent this year, which would make it the hardest-hit major emerging market in the world. Lower oil revenues and the virus impact mean the country’s sovereign debt is likely to lose its coveted investment grade credit rating in 2022 unless policy changes, according to Morgan Stanley. Colombia, the region’s fourth-biggest economy, has sounder government policies but risks a downgrade in the first half of next year because of weak public finances, the bank says.

José Ángel Gurría, secretary-general of the OECD, says Latin America will need greater relief on its debt © Stefan Wermuth/Bloomberg

The OECD’s Mr Gurría, who is a former Mexican finance minister, said investors had little tolerance for rising debt in emerging markets. “Once a country passes 50 per cent [debt to GDP] they put it on warning, once it passes 60 per cent they put flashing lights on it and once they pass 70 or 75 per cent . . . at that moment all the alarms go off”, he said.

Colombian president Iván Duque has argued that rating agencies should suspend their normal evaluation criteria for sovereign ratings because of the pandemic but his calls are unlikely to be heeded. Instead, investors are likely to favour nations which had built rainy day surpluses before the virus and are better placed to ride out the storm.

Peru and Chile are the best examples. “Peru’s financing strategy before Covid was practically a zero-debt policy,” Maria Antonieta Alva, Peru’s finance minister, told the FT. The country’s debt-to-GDP ratio was 26 per cent late last year and even after a generous stimulus plan, was still only forecast to rise to about 30 per cent, she added.

Eric Parrado, chief economist at the Inter-American Development Bank, forecasts that average debt levels across the region will rise from 57 per cent before the pandemic to 71-76 per cent by 2022. He said the rapidity of the debt build-up was particularly worrying.

“It’s not so much the absolute level of indebtedness which matters, as the speed at which it rises,” he said. “It’s rather like a bullet: if you throw it, it has no impact, but from a gun it’s the speed that kills you.”

0 comments:

Publicar un comentario