Equities imply that economic activity will swiftly return to previous peaks

Gavyn Davies

China’s manufacturing rebounded in April, but exports are down as the rest of the world struggles to overcome the pandemic © AFP via Getty Images

The strong recovery in global financial confidence caused the S&P 500 index to rebound 13 per cent in April, leaving US share prices only 9 per cent below their levels at the end of last year.

This may seem puzzling, given the slim prospect that a vaccine against the virus, or effective treatments, will become available soon.

The surge appears to rest on the pattern shown in gross domestic product forecasts from the big investment banks (see box), which is mainly driven by the expected path for supply shutdowns.

Based on indices of lockdown policies published by the Blavatnik School of Government, and on population movements shown on Google Maps, it is likely that supply curtailments in the advanced economies reached their peak in April.

From May onwards, a combination of gradual policy relaxations and normalisation of consumer behaviour should allow the global economy to bounce back.

China has already seen industrial activity rebound as shutdowns have been relaxed since late February, although exports are now weakening markedly amid global recession.

Growth expectations have also been supported by the sheer scale of the monetary and fiscal policy easing introduced around the world in just a few weeks.

Thomas Huray at Fulcrum estimates that the direct fiscal measures introduced in the advanced economies so far is equivalent to 6 per cent of 2019 nominal gross domestic product, roughly double the equivalent stimulus from 2008 in the financial crisis.

Furthermore, JPMorgan estimates that the expansion in central bank balance sheets may exceed 18 per cent of GDP by 2021, about three times the scale in the financial shock.

The relatively optimistic forecasts for the advanced economies seem to treat the 2020 downturn in a similar fashion to a recession caused by a natural disaster, which has a catastrophic immediate effect but then disappears extremely rapidly.

If that pattern is repeated this year, the implication is that share price valuations may be only minimally affected by discounted future profits.

According to a very interesting analysis by Zach Pandl of Goldman Sachs, the equity markets are assuming that the storm will blow over very quickly, with GDP growth rates being higher not lower than normal in 2021. On that basis, equities do not look particularly overvalued.

However, Mr Pandl adds that this outcome would be unique among recent recessions in the country.

In a normal cyclical downturn, predictions for GDP growth are reduced in successive years once a recession becomes inevitable.

This is particularly true in the second year after the recession starts, suggesting no early bounceback to previous peak activity.

The decline in output becomes persistent, not a springboard for recovery.

This more normal pattern underpinned the strong concerns expressed by Federal Reserve chairman Jay Powell last week about the medium-term risks to the productive capacity of the US economy following a very deep recession.

Mr Powell also said that the course of coronavirus itself is a new form of economic uncertainty.

He is clearly right about this.

Although the key infection rate — the reproduction rate — has almost certainly dropped below one in most countries during the lockdowns, there have already been indications from Germany and Singapore that improvements can be partially reversed as restrictions are relaxed.

The grim arithmetic of epidemics strongly suggests that any increase in the R rate significantly above one may lead, sooner or later, to a large second wave in infections that will need to be suppressed.

In his press conference on Thursday, the UK prime minister Boris Johnson promised that the country was now approaching “sunlight and pasture” after passing through the “huge tunnel” of Covid-19.

But his chief medical officer, Chris Whitty, suggested it would still be a “long slog” for all countries from here.

Unfortunately, the scientist has probably got it right.

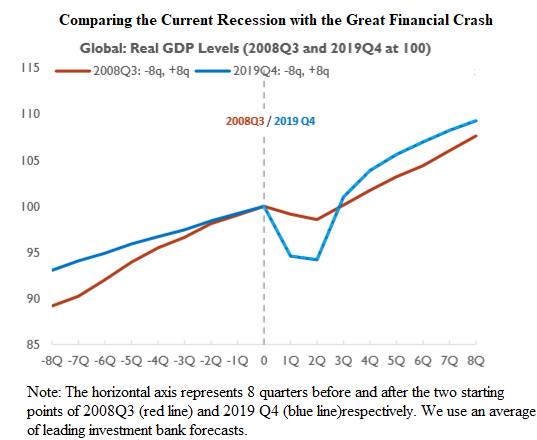

Market economic forecasts depict a short, sharp recession

Fulcrum has collected an indicative selection of economic forecasts from leading investment bank economists.

The average of these suggests that the level of GDP in the global economy will fall by 6 per cent in the first half of 2020, but then rebound to exceed pre-crisis levels of output by the beginning of 2021.

China is out of synchronisation with the advanced economies, and has already started to recover. This results in some smoothing in the cycle for the world as a whole.

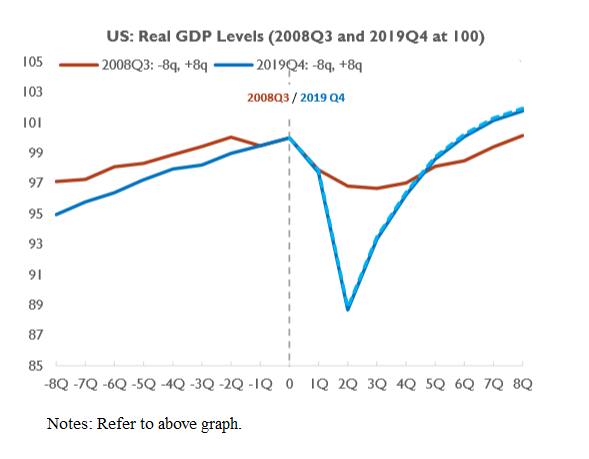

The US economy is expected to show a similar broad pattern, although both the recession and the recovery are expected to be much sharper than for the global economy as a whole.

The level of US GDP is expected to fall by 12 per cent in the first half of this year, returning to pre-crisis levels only in mid 2021.

0 comments:

Publicar un comentario