Berkshire Hathaway’s financing of Occidental Petroleum’s Anadarko deal could see it own a large chunk of the company if it gets paid in shares

By Spencer Jakab

Warren Buffett last year threw Occidental Petroleum a costly lifeline to support its purchase of Anadarko Petroleum. Photo: johannes eisele/Agence France-Presse/Getty Images .

The Oracle of Omaha wouldn’t stoop to a borderline-legal financing technique associated with penny-stock financiers.

Yet, while it was never his intention, Berkshire Hathaway BRK.B 3.72%▲ might wind up with a chunk of discounted shares in Occidental Petroleum OXY 3.31%▲ in a pattern similar to so-called death-spiral financing. The technique involves a company that is unable to raise public equity directly and instead issues debt privately to an outside source; the debt becomes convertible into stock for a fixed dollar amount rather than a fixed number of shares. The share price declines in anticipation of dilution, giving the financier much of the company.

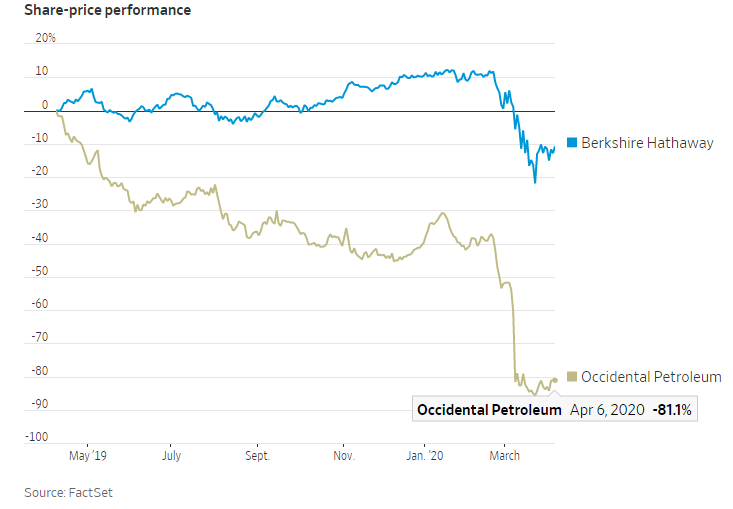

Last year, Occidental found itself in a bidding war with much-larger Chevron for Anadarko Petroleum. To win and to avoid having its own shareholders vote to approve it, Occidental paid for much of the $37 billion purchase with $10 billion in preferred stock bearing an 8% coupon issued to Berkshire.

While perpetual and not convertible, dividends can be paid in common stock at a 10% discount.

A year ago, when Occidental’s bidding war was heating up, its market value was $50 billion.

Now its value is $11.4 billion, it has slashed its dividend and capital expenditures and its debt prices signal distress.

A logical but painful way of staying afloat is to pay Mr. Buffett in shares at next week’s dividend declaration. Occidental can do so at 90% of the volume-weighted average price of Occidental’s shares for 10 days after the declaration.

At today’s price, paying the next four quarterly dividends in discounted stock would give Berkshire 7.3% of the company. Occidental also could ax its remaining common dividend and defer quarterly payments on the preferred shares, but then it would owe Berkshire dividends on the unpaid amount that compound ad infinitum.

Even Mr. Buffett wasn’t oracular enough to see this year’s coronavirus-induced oil-price collapse, and if there were a market price for his preferred stock then it would trade below par value. But he was smart enough to throw Occidental a costly lifeline.

The ideal outcome for Berkshire would be for Occidental to avoid a true death spiral but remain on the ropes long enough to give the conglomerate a chunk of a once-great oil company at a bargain Price.

0 comments:

Publicar un comentario